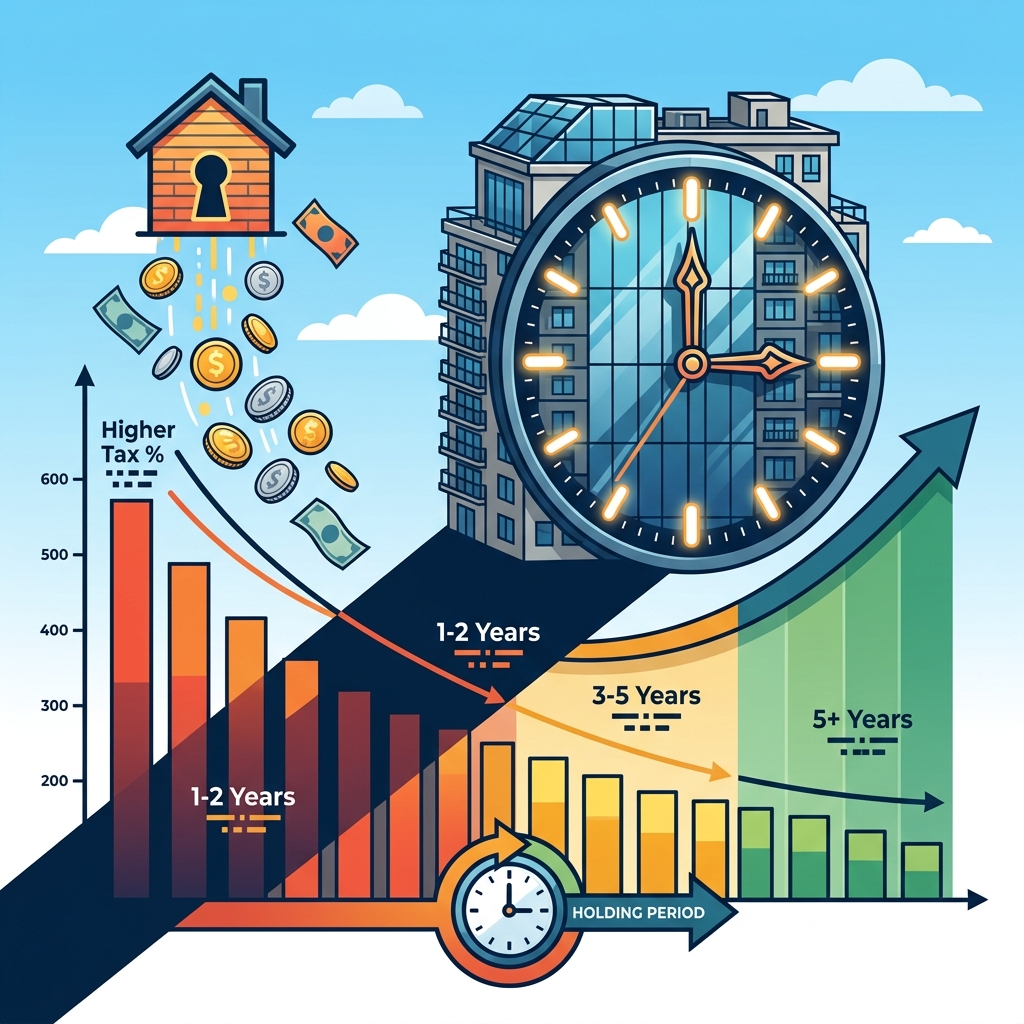

If you bought a private residential property in Singapore on or after 4 July 2025 and need to sell within the first year, the Seller’s Stamp Duty (SSD) — the government tax applied on the higher of the selling price or market value at exit — now sits at 16%. That is not a rounding error. That is a structural cost that rewires every holding-period assumption built around short-to-medium-term private property investment in this country.

Many investors still treat cooling measures as temporary friction — something the market absorbs over a cycle or two before reverting to form. The July 2025 SSD changes, which extended the holding period from three years to four and recalibrated the rate schedule, do not feel temporary. They feel deliberate, and they deserve a serious rethink of how exit strategies are constructed from day one.

This matters especially in the current market environment. URA Realis data shows overall private residential prices rose 0.9% quarter-on-quarter in Q1 2026, but total transaction volume fell 25.5% year-on-year — a market where prices hold but liquidity is thinning. This article walks through exactly how to reconstruct your exit-cost model under the new SSD framework before committing to any purchase.

Key Takeaways

– For private residential properties purchased on or after 4 July 2025, the SSD holding period extends to four years, with rates of 16%, 12%, 8%, and 4% across Years 1–4 respectively (Source: IRAS, effective 4 July 2025).

– On a S$2 million property, a Year 1 exit triggers S$320,000 in SSD alone — before agent fees, legal costs, or any foregone capital gain.

– Total private residential sales volume reached 5,413 units in Q1 2026, down 25.5% year-on-year, indicating thinning secondary market liquidity (Source: URA Realis via 99.co, April 2026).

– RCR non-landed prices rose 0.8% quarter-on-quarter in Q1 2026, outpacing CCR at 0.6% in momentum terms, though CCR commands a substantially higher absolute base (Source: URA price index via Cushman & Wakefield, April 2026).

– Every acquisition modelled on a sub-four-year hold requires price appreciation materially above the applicable SSD rate just to break even, based on the IRAS schedule effective 4 July 2025.

Understanding the 2025 Seller’s Stamp Duty Framework

The 2025 SSD framework applies a four-tier rate schedule to any private residential property purchased on or after 4 July 2025 — extending the previous three-year holding window by a full additional year and raising the peak rate to 16%.

According to IRAS and MAS, the current schedule is applied to the higher of the actual selling price or market value at the point of disposal:

- Within 1 year of purchase: 16%

- Within 2 years: 12%

- Within 3 years: 8%

- Within 4 years: 4%

- Beyond 4 years: No SSD payable

Properties purchased before 4 July 2025 retain the old schedule — a three-year window with rates of 12%, 8%, and 4% respectively. This distinction is not academic. Two otherwise identical properties transacting on either side of that date carry materially different exit cost structures for the buyer.

On a S$2 million property sold within the first year under the new framework, SSD alone amounts to S$320,000. That figure excludes the Additional Buyer’s Stamp Duty (ABSD) already paid at entry, legal fees, agent commissions, and any capital gains foregone by an early exit. The cost of a premature sale has compounded significantly.

The policy rationale, as stated by MAS, is to curb speculative short-term trading in residential property. The four-year threshold aligns more closely with a typical property cycle and is consistent with the broader macro-prudential posture Singapore has maintained since the 2021–2022 cooling measure sequence.

Sub-sale transactions — a proxy for short-term flipping — accounted for approximately 175 units in Q1 2026, representing roughly 3.2% of total private residential sales volume of 5,413 units (Source: URA Realis via 99.co, April 2026). The new SSD structure is a likely structural contributor to that suppression.

Practical takeaway: Any holding-period model built for a property purchased on or after 4 July 2025 must account for a minimum four-year SSD window. Exit strategies planned before year four require explicit SSD provisioning at the applicable rate, calculated on whichever is higher — contracted sale price or independent market valuation.

How Holding Period Directly Determines Net Capital Gains

How long you hold a private residential property purchased on or after 4 July 2025 directly determines what percentage of your gross profit is surrendered before a single dollar of net gain is realised.

The stamp duty is calculated on the higher of the actual transacted price or market value at disposal. For a property sold at S$2 million, the tax burden across each holding tier is material:

| Holding Period | SSD Rate (Post-July 2025) | Estimated Tax on S$2M Property | Net Gain Margin Impact |

|---|---|---|---|

| Within 1 Year | 16% | S$320,000 | Full gross gain reduced by S$320,000 before other costs |

| Within 2 Years | 12% | S$240,000 | S$80,000 less tax vs. Year 1 exit |

| Within 3 Years | 8% | S$160,000 | S$160,000 less tax vs. Year 1 exit |

| Within 4 Years | 4% | S$80,000 | S$240,000 less tax vs. Year 1 exit |

Note: Table assumes S$2M as the higher of selling price or market value. SSD liability based on IRAS schedule effective 4 July 2025. Agent commissions, legal fees, and BSD excluded.

To contextualise why the holding period calculus matters in the current cycle: overall private residential prices rose 0.9% quarter-on-quarter in Q1 2026, with OCR non-landed leading at +2.2% q-o-q (Source: URA price index via Cushman & Wakefield, April 2026). On a S$2 million asset, a 2.2% quarterly price appreciation generates approximately S$44,000 in gross gain — a figure entirely consumed by a 16% SSD charge of S$320,000 on a Year 1 exit.

The SSD structure does not merely reduce profitability at the margin. For properties held fewer than four years, it can convert a nominally positive price movement into a net capital loss once stamp duty, agent fees (estimated at 1–2% of transaction value based on standard CEA guidelines), and legal costs are factored in.

Practical takeaway: For any private residential property acquired on or after 4 July 2025, model your exit scenario at the four-year minimum before committing to a purchase price — a sub-four-year hold requires price appreciation materially above the SSD rate for that tier just to break even, based on the IRAS schedule effective 4 July 2025.

CCR vs RCR: Where Price Momentum Sits in 2026

The Core Central Region (CCR — broadly covering Districts 9, 10, 11, the Downtown Core, and Sentosa) and the Rest of Central Region (RCR — the city fringe belt covering districts such as 3, 4, 8, 12, 13, and 14) are moving at meaningfully different speeds in 2026.

According to URA price index data compiled by Cushman & Wakefield (April 2026), RCR non-landed private residential prices rose 0.8% quarter-on-quarter in Q1 2026, while CCR recorded a more modest 0.6% gain over the same period. The Outside Central Region (OCR) outpaced both at +2.2% quarter-on-quarter.

In absolute quantum, new launches transacted at a median of S$2,660 per square foot versus S$1,766 per square foot for resale units in Q1 2026 — a 50.6% premium for new stock (Source: Business Times, April 2026). This gap is relevant when comparing CCR projects — where new launches are concentrated at higher absolute quantum — against RCR resale units that may offer more accessible price points for upgraders.

Total private residential sales reached 5,413 units in Q1 2026, down 25.5% year-on-year, with resale transactions accounting for 59.6% of that total (Source: URA Realis via 99.co, April 2026). Secondary market liquidity remains the dominant activity channel even as new launch pipelines persist.

Practical takeaway: If your budget sits in the S$1.8 million to S$2.5 million range, RCR resale non-landed stock currently offers relatively stronger quarter-on-quarter price momentum at a lower per-square-foot entry point than comparable CCR new launches — though all projections remain subject to market conditions and individual project fundamentals.

Building a Financially Sound Holding Strategy for 2026

Strategic financial planning for a post-July 2025 purchase begins with aligning entry price, financing structure, and intended holding period before signing any Option to Purchase — because the interaction between SSD liability and market price movements determines whether a transaction generates real wealth or simply returns capital.

Non-landed properties led price recovery in Q1 2026, with OCR recording the strongest gain at +2.2% quarter-on-quarter, ahead of RCR at +0.8% and CCR at +0.6%. Landed properties contracted 0.4% over the same period (Source: URA price index via Cushman & Wakefield, April 2026).

These figures carry a direct implication for financial modelling. A 2.2% quarterly price gain on a S$1.5 million OCR non-landed unit represents estimated appreciation of approximately S$33,000 — a figure that is substantially eroded by an 8% SSD liability of S$120,000 if the property is disposed of within three years of a post-4 July 2025 purchase. Exit timing, not entry price alone, drives net return.

For investors with properties purchased before 4 July 2025, the older three-year SSD schedule with rates of 12%, 8%, and 4% continues to apply — a relative timing advantage over newer acquisitions held to comparable durations.

Transaction volume data reinforces the case for a medium-to-long holding horizon. With total Q1 2026 sales down 25.5% year-on-year and resale activity accounting for 59.6% of that reduced total, longer marketing periods in softer quarters are a realistic scenario to plan for (Source: URA Realis via 99.co, April 2026).

Practical takeaway: Model your net capital position across all four SSD holding tiers before signing any OTP on a post-July 2025 purchase — the difference between a Year 3 and Year 4 exit on a S$2 million property is S$80,000 in stamp duty savings alone, based on current IRAS rates.

Frequently Asked Questions

What is the difference between CCR and RCR property prices in Singapore in 2026?

According to URA price index data compiled by Cushman & Wakefield (April 2026), RCR non-landed prices rose 0.8% quarter-on-quarter versus 0.6% for CCR in Q1 2026 — the city fringe is currently outpacing the prime district in momentum terms. In absolute quantum, new launches transacted at a median of S$2,660 per square foot versus S$1,766 per square foot for resale units, a 50.6% premium that disproportionately reflects CCR new stock (Source: Business Times, April 2026). Buyers in the S$1.8 million to S$2.5 million range will generally find more accessible per-square-foot entry points in the RCR resale segment.

How does the new Seller’s Stamp Duty affect property investment in Singapore?

Effective 4 July 2025, IRAS extended the SSD holding period for private residential properties from three years to four, with rates of 16%, 12%, 8%, and 4% applying across Years 1 through 4 respectively (Source: IRAS, effective 4 July 2025). On a S$2 million property, a Year 2 exit triggers an SSD liability of S$240,000 — a cost that would eliminate most or all capital gains in a market where quarterly price gains are running below 2.5%. Investors should model the full four-year SSD schedule before signing any Option to Purchase on properties acquired from 4 July 2025 onwards.

What percentage of Singapore property transactions are resale versus new launch in 2026?

According to URA Realis data compiled by 99.co (April 2026), resale transactions accounted for 59.6% of total private residential sales in Q1 2026 — approximately 3,225 units out of 5,413 total. New sales contributed around 2,013 units and sub-sales accounted for approximately 175 units over the same period. The dominance of resale volume is relevant for investors modelling realistic secondary market exit windows.

How much stamp duty is saved by holding for 4 years instead of 3?

Under the IRAS SSD schedule effective 4 July 2025, a property sold in Year 3 attracts an 8% SSD rate, while a Year 4 exit reduces that liability to 4% — a difference of S$80,000 on a S$2 million transaction. Holding beyond four years eliminates SSD liability entirely, making the Year 4-to-Year 5 transition the most financially significant holding decision for most investors.

Does the new SSD apply to properties purchased before 4 July 2025?

No. Properties purchased before 4 July 2025 retain the old three-year SSD schedule with rates of 12%, 8%, and 4% for Years 1, 2, and 3 respectively (Source: IRAS). The extended four-year schedule at 16%, 12%, 8%, and 4% applies only to private residential properties purchased on or after 4 July 2025.

One Conversation, Full Clarity

If you are working through a purchase decision and want to stress-test the numbers against your specific holding horizon, Whatsapp Joe directly, no pitch, no obligations.

Data Sources: All figures sourced from URA, IRAS, and MAS publications, supplemented by Cushman & Wakefield, Business Times, and 99.co reporting. Data current as of April 2026.

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This article is for general reference only and does not constitute financial, legal, or investment advice. Verify all details with relevant authorities before making decisions.