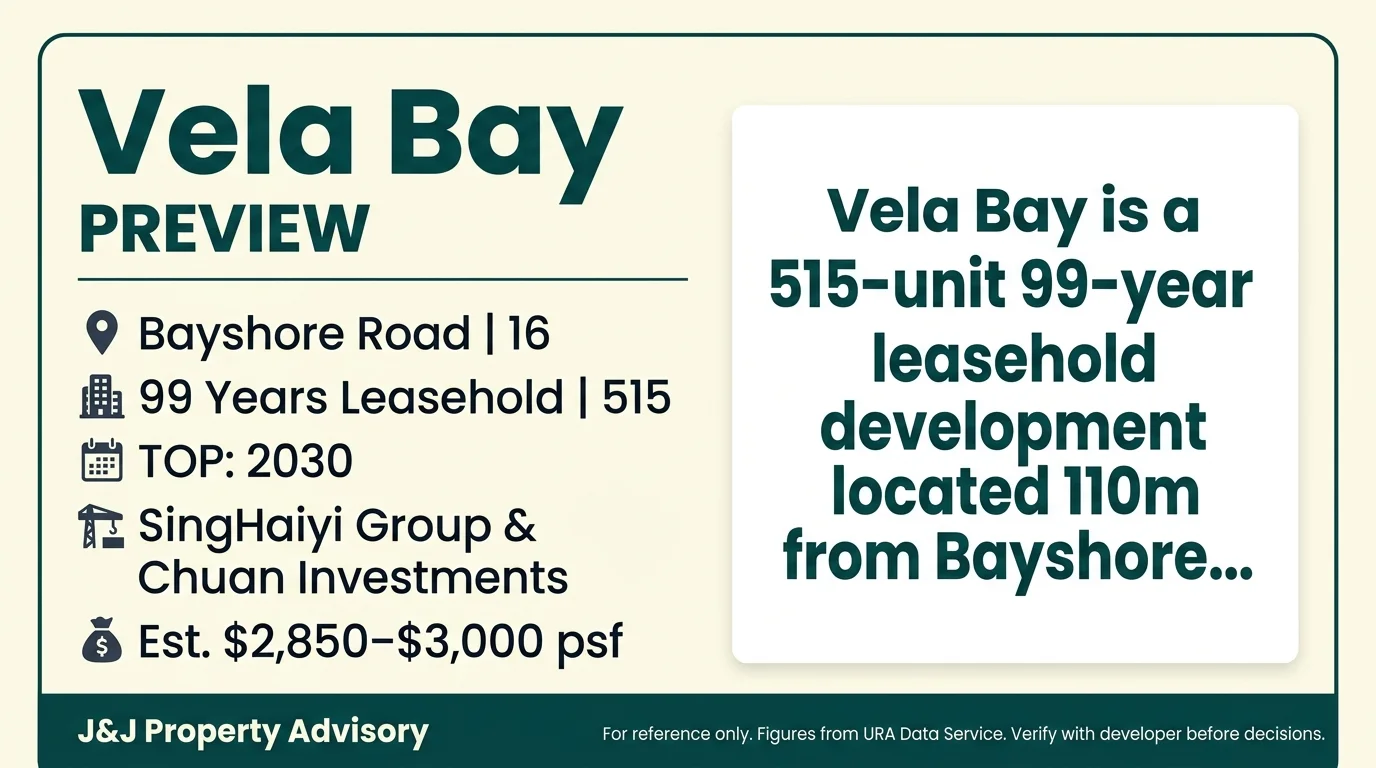

Project Snapshot

| Attribute | Details |

| Site Area | 112,991.9 sqft / 10,497.3 sqm |

| Developer | SingHaiyi Group & Chuan Investments |

| Tenure | 99 Years Leasehold |

| Total Units | 515 |

| Land Cost PSF PPR | S$1,388 |

| Expected TOP | 2030 |

| Launch Date | 11 April 2026 |

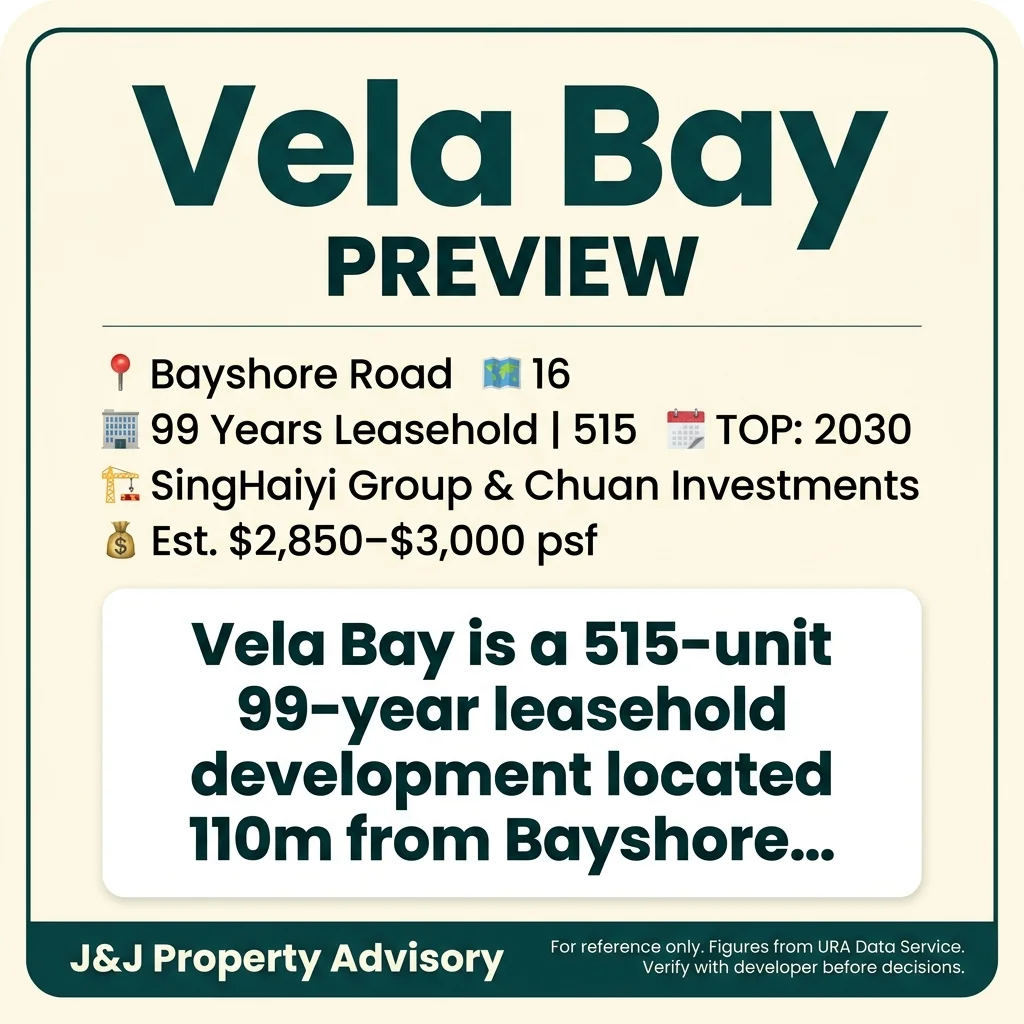

Vela Bay is a 515-unit condominium development on a 10,497.3 sqm site along Bayshore Road, positioned approximately 110 metres from Bayshore MRT station on the Thomson-East Coast Line. The joint venture between SingHaiyi Group and Chuan Investments acquired the site at S$1,388 PSF PPR in March 2025, marking one of the highest land costs recorded in District 16 and signalling developer confidence in the emerging Bayshore precinct. The development comprises two 31-storey blocks with 258 standard carpark lots and 3 handicap lots, designed by P&T Consultants for completion in 2030.

Location & Connectivity

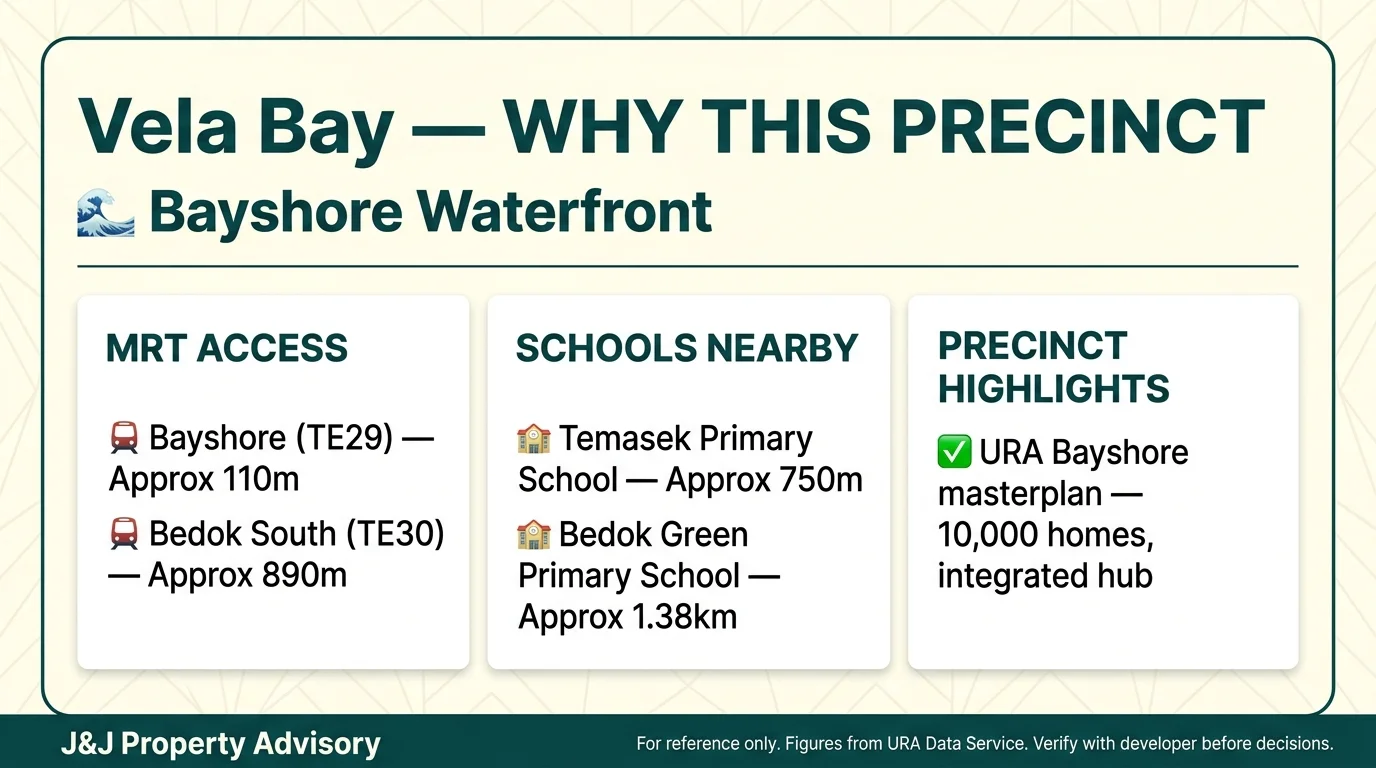

1. MRT Access — Immediate TEL Connectivity

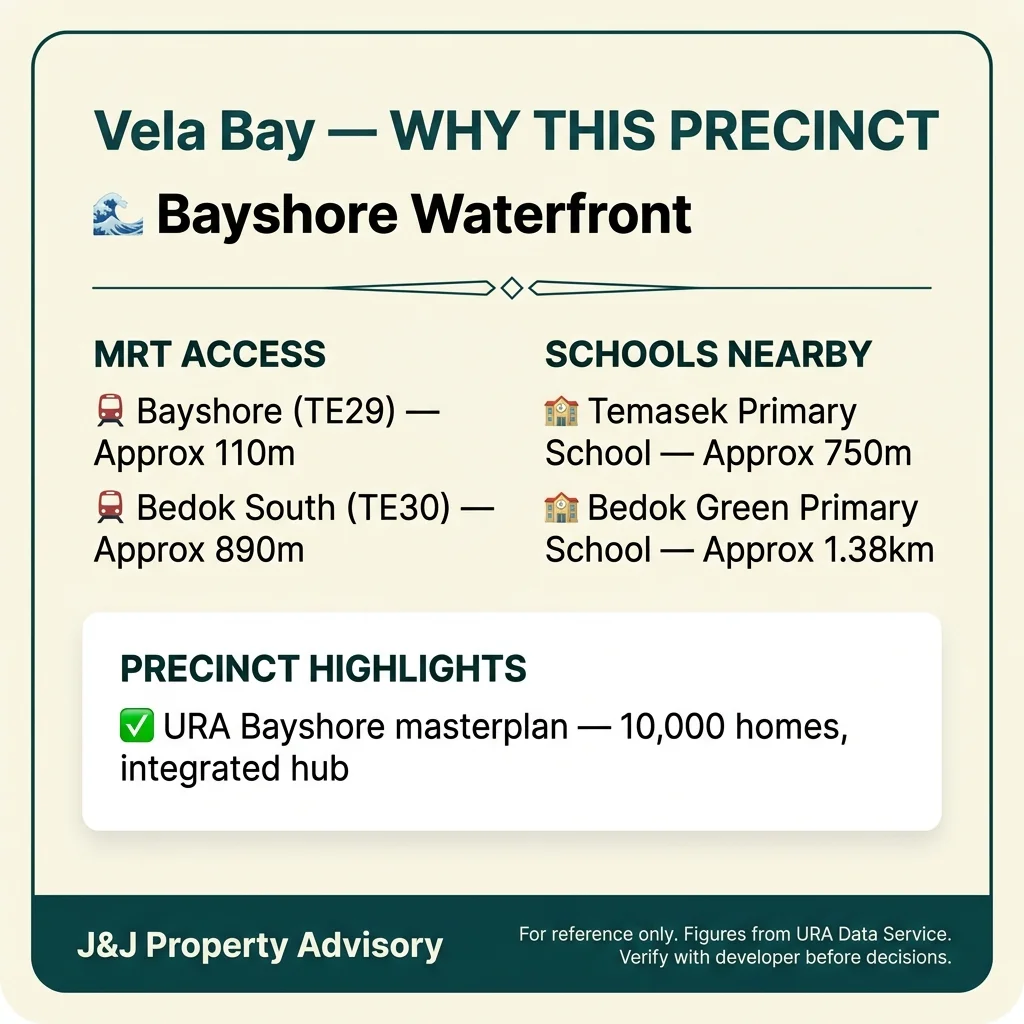

Bayshore MRT station (TE29) is approximately 110 metres from the site, providing direct access to the Thomson-East Coast Line which opened in June 2024. Bedok South MRT station (TE30) is approximately 890 metres away and scheduled to open in 2026. This dual-station proximity positions Vela Bay within the core of the new Bayshore transport-oriented development precinct.

2. Primary School Proximity

Temasek Primary School is approximately 750 metres from the site, placing the development within the 1-kilometre priority admission zone for this mixed school. Bedok Green Primary School is approximately 1.38 kilometres away. The immediate catchment has limited primary school density compared to mature HDB estates further inland, though the TEL connection provides access to a broader range of schools within 2-3 MRT stops.

3. Retail and Commercial Amenities

Bedok Mall is approximately 1.96 kilometres from the site, accessible via Bedok South MRT when operational in 2026. The immediate Bayshore Road corridor is still developing its retail infrastructure as part of the URA Master Plan 2025 vision, which outlines new Plus-model HDB projects, an integrated transport hub, and a SAFRA clubhouse for the 60-hectare waterfront precinct. Current retail provision is modest compared to established Bedok town centre.

4. Coastal Recreation Access

The development is located next to East Coast Park, Singapore’s longest coastal park, providing immediate access to cycling paths, beach facilities, and recreational infrastructure. The URA Master Plan 2025 envisions green corridors and tree-lined walkways linking the Bayshore precinct to both the MRT stations and coastal amenities. This coastal adjacency differentiates the location from typical inland HDB-adjacent new launch sites.

5. Expressway and Regional Connections

The site is served by the Pan Island Expressway via the Bedok North and Bedok South exits, providing east-west connectivity to the CBD and Changi Airport. Travel times to the CBD are approximately 20-25 minutes by car during off-peak periods and 30-35 minutes via the TEL. The precinct’s position between Bedok and Tampines clusters it within the eastern residential corridor but outside the immediate commercial intensity of either mature town centre.

Developer Track Record

SingHaiyi Group is a diversified property company specialising in development, investment, and management services with a portfolio spanning residential, commercial, and retail assets in Singapore and internationally. The company has executed multiple residential projects across different market segments, though its profile among mass-market buyers is typically lower than major developers such as CapitaLand or City Developments Limited. SingHaiyi’s involvement in this joint venture brings financial capacity and local market experience, though buyers should note the company’s scale and brand recognition differs from Tier 1 developers frequently active in large-format new launches.

Chuan Investments operates through Chuan Holdings Limited, a construction and property development company listed on the Main Board of the Stock Exchange of Hong Kong. Its subsidiary, Chuan Lim Construction Pte. Ltd., focuses on safety, quality workmanship, and project delivery across construction contracts. Chuan’s primary business is construction services rather than residential property development, which means its track record in delivering completed condominiums for end-buyer handover is less extensive than pure-play property developers. The company’s construction expertise may translate to build quality and project management capability, but prospective buyers should assess its residential property development portfolio independently before committing.

This joint venture structure combines SingHaiyi’s property development experience with Chuan’s construction capabilities. The S$1,388 PSF PPR land cost suggests both partners have committed significant capital and are targeting premium pricing to achieve financial viability. Buyers should evaluate whether the joint venture’s combined track record provides sufficient confidence in project execution, defect management, and post-TOP support, particularly given the 2030 completion timeline and the scale of 515 units across two 31-storey blocks.

Projected Pricing & Land Cost Analysis

This section contains analyst projections only. No official pricing has been released.

The land cost of S$1,388 PSF PPR establishes the baseline cost structure. Using standard industry development margin analysis, the breakeven point falls between S$2,360 PSF (1.7x multiplier) and S$2,500 PSF (1.8x multiplier), assuming typical construction costs of S$350-400 PSF, professional fees, marketing expenses, and developer profit margin. This calculation provides a floor, not a ceiling—actual launch pricing depends on market positioning strategy, unit efficiency, and comparable benchmarking.

Examining District 16 comparables reveals limited recent transaction data. The Bayshore precinct has seen minimal new launches since 2015, creating a data vacuum for direct comparison. Expanding the lens to adjacent precincts: Marine Parade projects such as The Reef at King’s Dock (District 4, not directly comparable due to location premium) and older launches like The Coast at Sentosa Cove (District 4, freehold, premium tier) trade above S$2,400 PSF but serve different buyer segments. Within District 16 itself, older developments like The Shaughnessy and Laguna Park report resale medians between S$1,600-1,900 PSF, but these are 15-20 year old projects without new launch comparability.

The absence of competing new launches in Bayshore within the past five years means Vela Bay will likely establish the pricing benchmark rather than follow it. Given the land cost floor of S$2,360 PSF and the need to attract HDB upgraders from Bedok and Tampines (median 4-room prices of S$574k and S$650k respectively), the developer faces a balancing act: price too high and the upgrader segment cannot qualify; price at breakeven and margin compression risks quality trade-offs.

Projected Launch PSF: S$2,400 – S$2,650 PSF (Est.)

This range reflects breakeven-plus positioning, factoring in the scarcity premium from limited Bayshore supply and the need to remain accessible to HDB upgraders with S$350k-500k equity. At S$2,500 PSF average, a 700 sqft 2-bedroom unit would quantum at S$1.75M (Est.), requiring S$438k cash (25% down) plus ABSD for second-timers—a stretch for median 4-room upgraders but viable for 5-room or Executive flat sellers with S$500k-700k equity.

If unit sizes skew smaller (650-750 sqft for 2-bedrooms), quantums could fall to S$1.56M – S$1.99M (Est.), improving affordability. Larger 3-bedroom units at 1,000 sqft would quantum at S$2.5M (Est.), targeting dual-income professionals or families liquidating larger HDB flats. The developer’s unit mix strategy remains unknown, introducing material uncertainty into these projections.

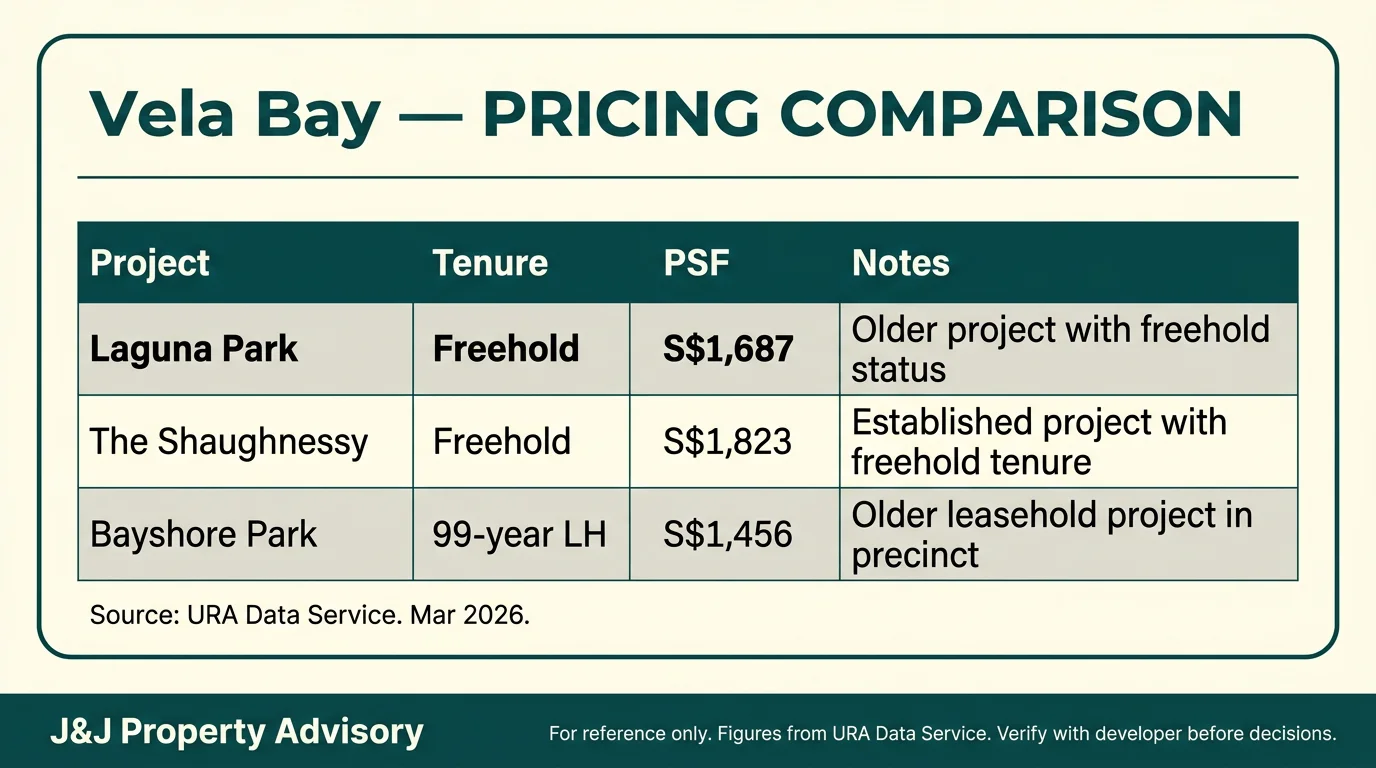

Market Comparables

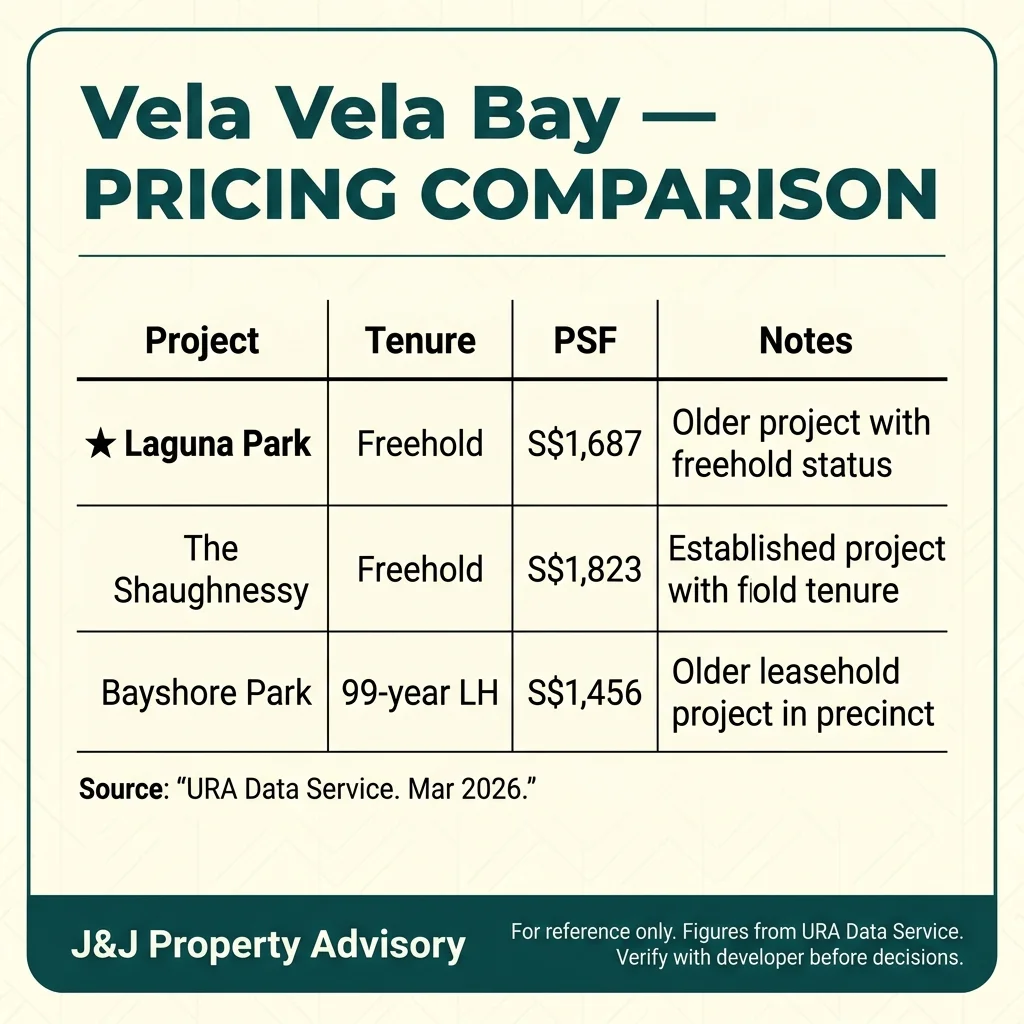

| Project | District | PSF (Median) | Transactions (12mo) | Tenure |

| Laguna Park | 16 | S$1,687 | 18 | Freehold |

| The Shaughnessy | 16 | S$1,823 | 12 | Freehold |

| Bayshore Park | 15 | S$1,456 | 8 | 99-year LH |

Direct comparables within District 16’s Bayshore area are functionally absent due to the lack of new launches since 2015. The table below expands to include adjacent eastern precincts for context, though these projects serve different micro-markets.

All listed comparables are secondary market resales of projects completed pre-2010, making direct price comparison unreliable. Freehold projects command a 10-15% premium over 99-year leasehold equivalents at similar ages, meaning Vela Bay’s leasehold tenure naturally positions it below freehold benchmarks. However, as a new launch with 99 years remaining versus older projects with 70-80 years left (or freehold), the tenure gap narrows in practical mortgage and resale terms for the first 20 years.

Vela Bay’s projected S$2,400 – S$2,650 PSF range sits approximately 30-40% above current Bayshore precinct resale medians, consistent with the typical new launch premium but introducing affordability barriers for buyers comparing against existing stock. The premium is justified by new development standards, full facility suites, and longer lease runway, but buyers must weigh this against the opportunity to purchase larger resale units at lower PSF in the same precinct.

Key Strengths

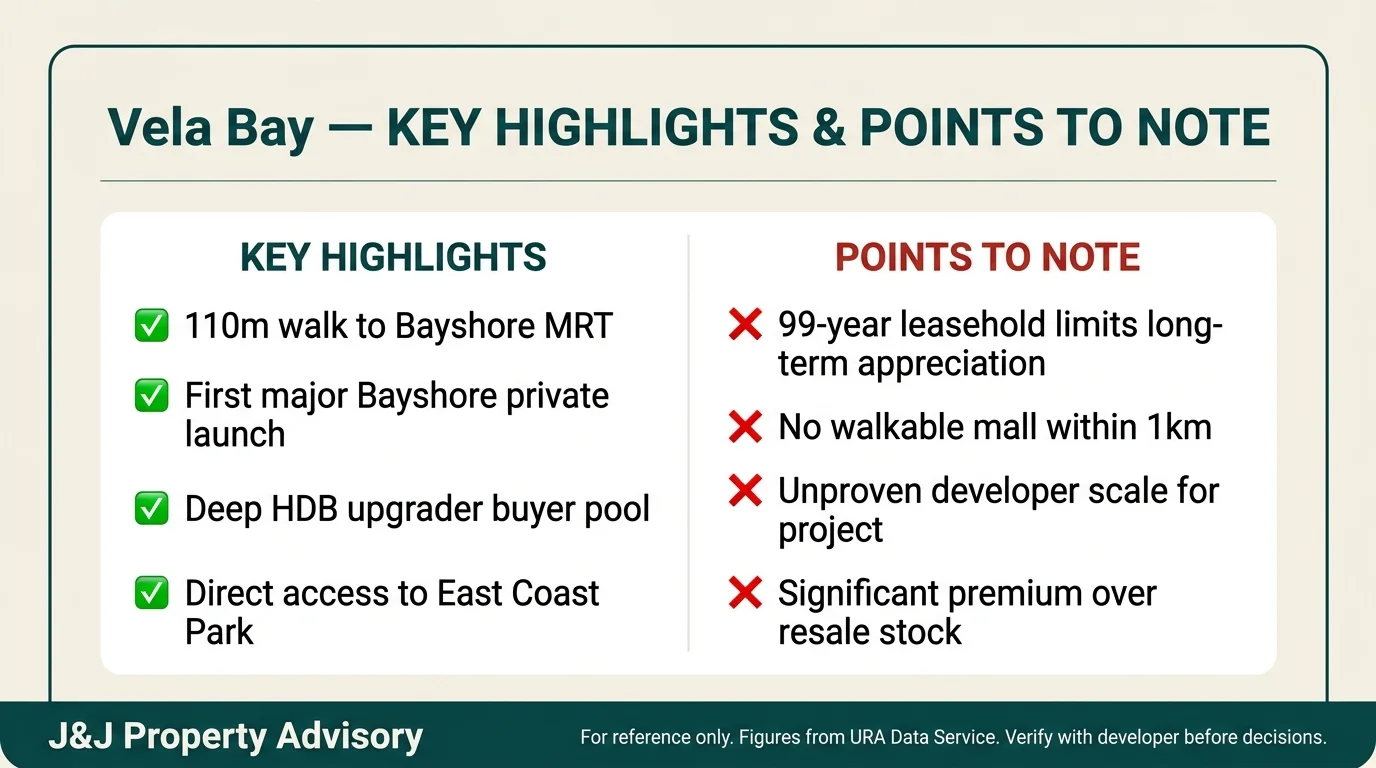

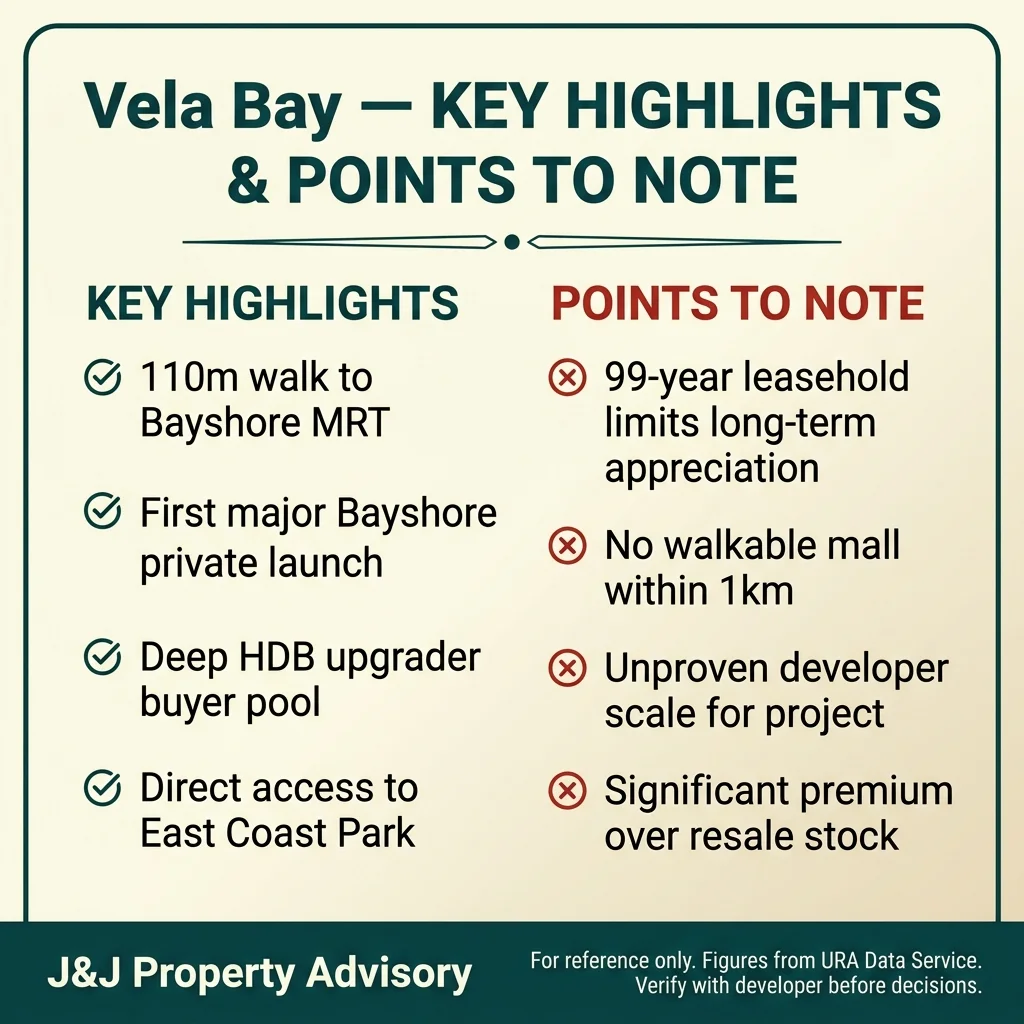

1. MRT Proximity: 110m from TE29 Establishes Transit Advantage

The approximately 110m walk to Bayshore station (TE29) places Vela Bay among the most transit-connected private developments in District 16. The Thomson-East Coast Line’s 2024 completion eliminated previous transfer inefficiencies, reducing CBD commute times to approximately 30 minutes. For car-lite households, this proximity translates to tangible monthly savings on vehicle ownership costs, potentially offsetting 10-15% of mortgage payments for young professionals prioritising transport convenience.

2. Supply Scarcity: First Major Private Launch in Bayshore Since 2015

The Bayshore precinct has seen minimal new private supply in the past decade, with most residential stock dating to the 2000-2010 development cycle. This scarcity creates price support from pent-up demand among buyers specifically targeting the Marine Parade to Bedok coastal corridor. The lack of competing new launches within 1km gives Vela Bay temporary monopoly positioning for buyers unwilling to consider older secondary stock.

3. HDB Upgrader Catchment: Large Bedok and Tampines Resale Markets Nearby

The surrounding Bedok and Tampines HDB estates generated over 4,000 resale transactions in the past 24 months, with 4-room median prices of S$574k (Bedok) and S$650k (Tampines). This established upgrader base, combined with approximately 6,383 total transactions across all flat types, provides a deep buyer pool with S$350k-500k equity capacity. If Vela Bay’s pricing allows 2-bedroom quantums below S$1.8M, it captures this segment effectively.

4. East Coast Park Access: Unique Lifestyle Amenity for Family Buyers

Approximately 500m to East Coast Park’s Area C facilities positions Vela Bay as one of the few private developments offering sub-10-minute access to Singapore’s largest waterfront park. For families prioritising outdoor recreation, cycling infrastructure, and weekend beach access, this proximity represents a lifestyle differentiator unavailable in most urban or suburban precincts. The value proposition strengthens for buyers working from home or with flexible schedules, maximising park utilisation during weekday off-peak hours.

Points to Watch

1. Leasehold Tenure: 99-Year Structure Limits Long-Term Appreciation

The 99-year leasehold tenure introduces depreciation headwinds absent in freehold alternatives. While the 2030 TOP provides 95+ years remaining lease, the HDB upgrader segment may face resale challenges after 15-20 years when the lease drops below 80 years, tightening mortgage tenures for subsequent buyers. Freehold comparables like Laguna Park and The Shaughnessy in the same precinct offer longer holding flexibility, though at different price points and age profiles.

2. Retail Amenity Gap: No Walkable Mall Within 1km Radius

Bedok Mall at approximately 1.96km represents the nearest large-format retail centre, requiring vehicular transport or a 20-minute walk for grocery and dining needs. The Bayshore precinct itself lacks neighbourhood commercial concentration, creating daily convenience friction for car-lite households. Buyers prioritising walkable retail access will find Vela Bay materially weaker than projects near established town centres like Bedok Central or Tampines Hub.

3. Unproven Developer Scale: 515-Unit Count Tests JV Execution Capacity

Neither SingHaiyi nor Chuan Investments has delivered a 500-plus unit development in recent years, making Vela Bay a scale test for both partners. Large projects introduce defect management complexity, handover coordination challenges, and facility maintenance variables that smaller developments avoid. Buyers should scrutinise showflat build quality, warranty terms, and the developer’s defect rectification track record before committing deposits.

4. Pricing Risk: Breakeven PSF Leaves Minimal Downside Buffer

The land cost of S$1,388 PSF PPR establishes a breakeven range near S$2,360 – S$2,500 PSF, limiting the developer’s ability to discount during soft market conditions. If sales velocity underperforms, the developer faces constrained pricing flexibility compared to projects with lower land cost bases. Buyers should assess launch pricing carefully—paying near breakeven transfers downside risk from developer to purchaser if market sentiment deteriorates before TOP.

5. Unknown Unit Mix: Layout Efficiency and Bedroom Distribution Remain Undisclosed

Without confirmed floor plans, buyers cannot assess layout efficiency, bedroom size adequacy, or spatial functionality. A 2-bedroom unit at 650 sqft delivers different liveability than one at 750 sqft, yet both may quantum similarly if PSF varies. The developer’s decision to prioritise compact investor units versus family-sized layouts will materially impact owner-occupier satisfaction. This uncertainty elevates risk for early buyers committing before showflat opening.

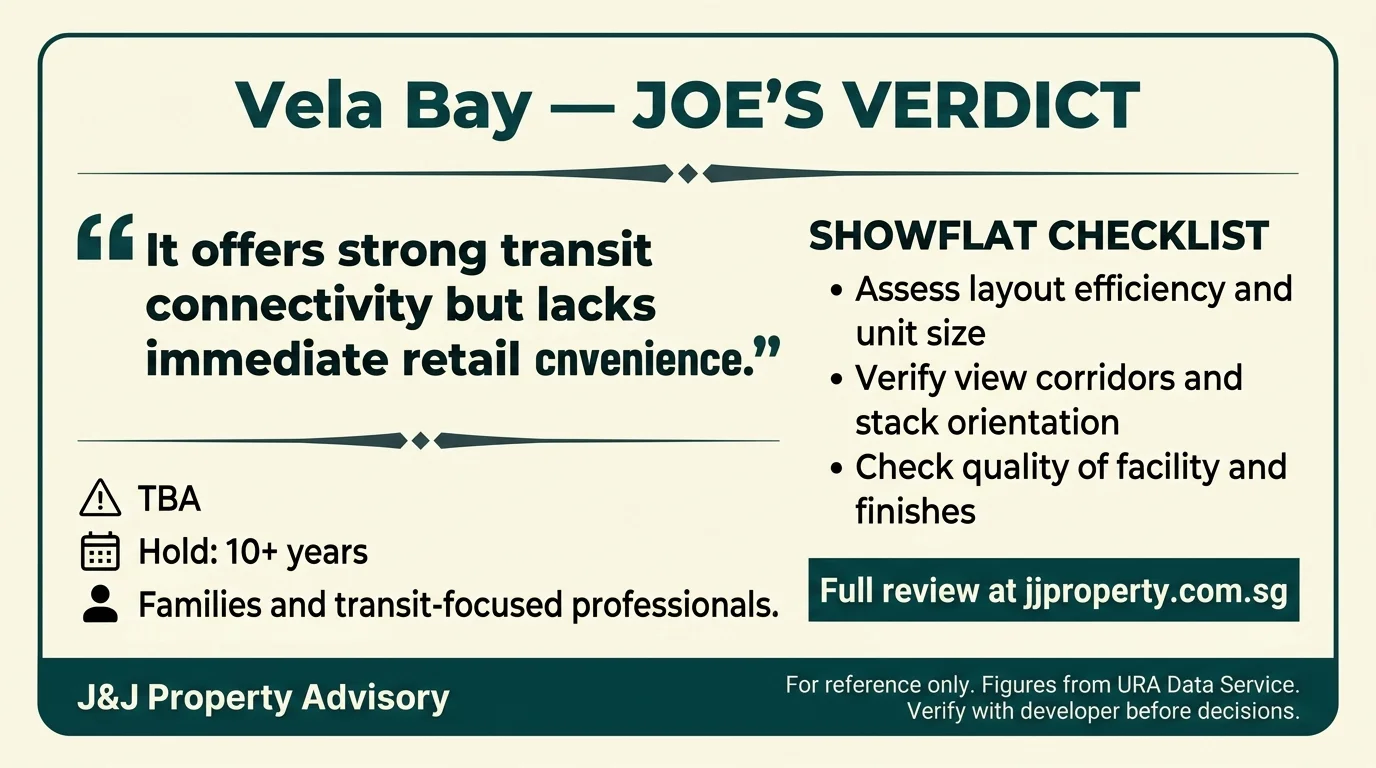

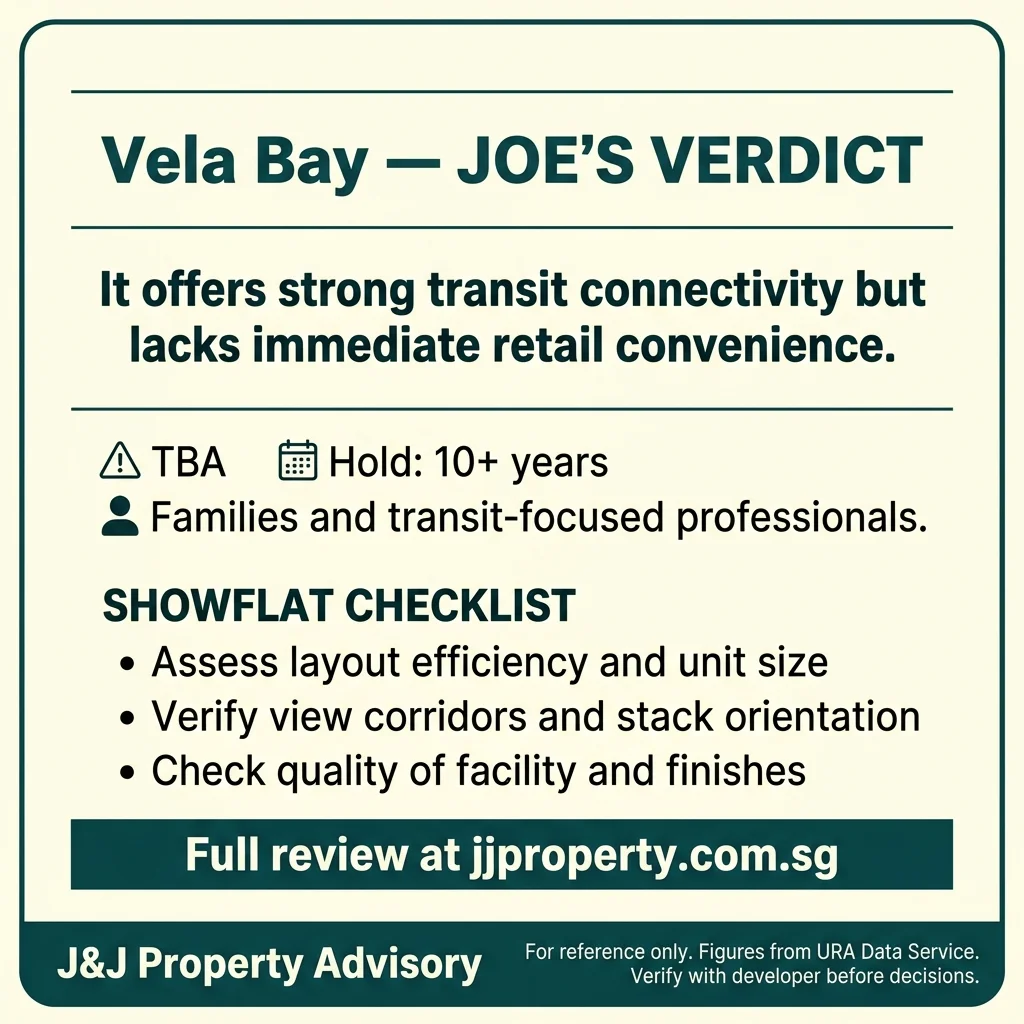

Bottom Line

Vela Bay offers rare MRT proximity (110 metres to Bayshore station) and coastal adjacency within a masterplan-backed precinct that will add 10,000 homes and integrated amenities by the mid-2030s. The S$1,388 PSF PPR land cost signals developer confidence in the Bayshore precinct’s value trajectory, though it also guarantees launch pricing will be substantially above older District 16 resale benchmarks. The 515-unit scale provides economies of scale in facilities provision but raises questions about layout efficiency and quantum affordability for upgraders. Critical unknowns remain: official pricing, unit mix, bedroom distribution, and stack configurations have not been released, making preliminary assessment incomplete.

For Own-Stay Buyers: HDB upgraders from Bedok or Tampines with S$400k-S$600k equity and strong income capacity may find value if entry-level 2-bedroom units are priced below S$1.8M and the MRT proximity justifies a premium over resale alternatives. Young families should confirm Temasek Primary School (750 metres) registration prospects and assess tolerance for precinct immaturity during the first 3-5 years post-TOP. Buyers prioritising coastal lifestyle, MRT convenience, and long-term hold potential (15+ years) will benefit most. Those seeking immediate retail convenience or established estate amenities should consider mature Bedok resale condos instead.

For Investment Buyers: Rental yield will depend on quantum competitiveness versus freehold comparables—if Vela Bay launches at S$2,700+ PSF, investors must achieve S$4,500-S$5,500 monthly rents for 2-bedroom units to secure 3.5-4.0% gross yields, competing with freehold projects at similar quantums. The MRT proximity and East Coast Park adjacency support tenant demand from young professionals and expat families, though the precinct’s immaturity may limit rental appeal until amenities mature. Capital appreciation depends on Bayshore precinct build-out success and District 16 value re-rating over the 2030-2040 period. The 99-year leasehold tenure caps long-term appreciation relative to freehold alternatives, making this more suitable for 7-10 year hold strategies rather than multi-generational wealth preservation.

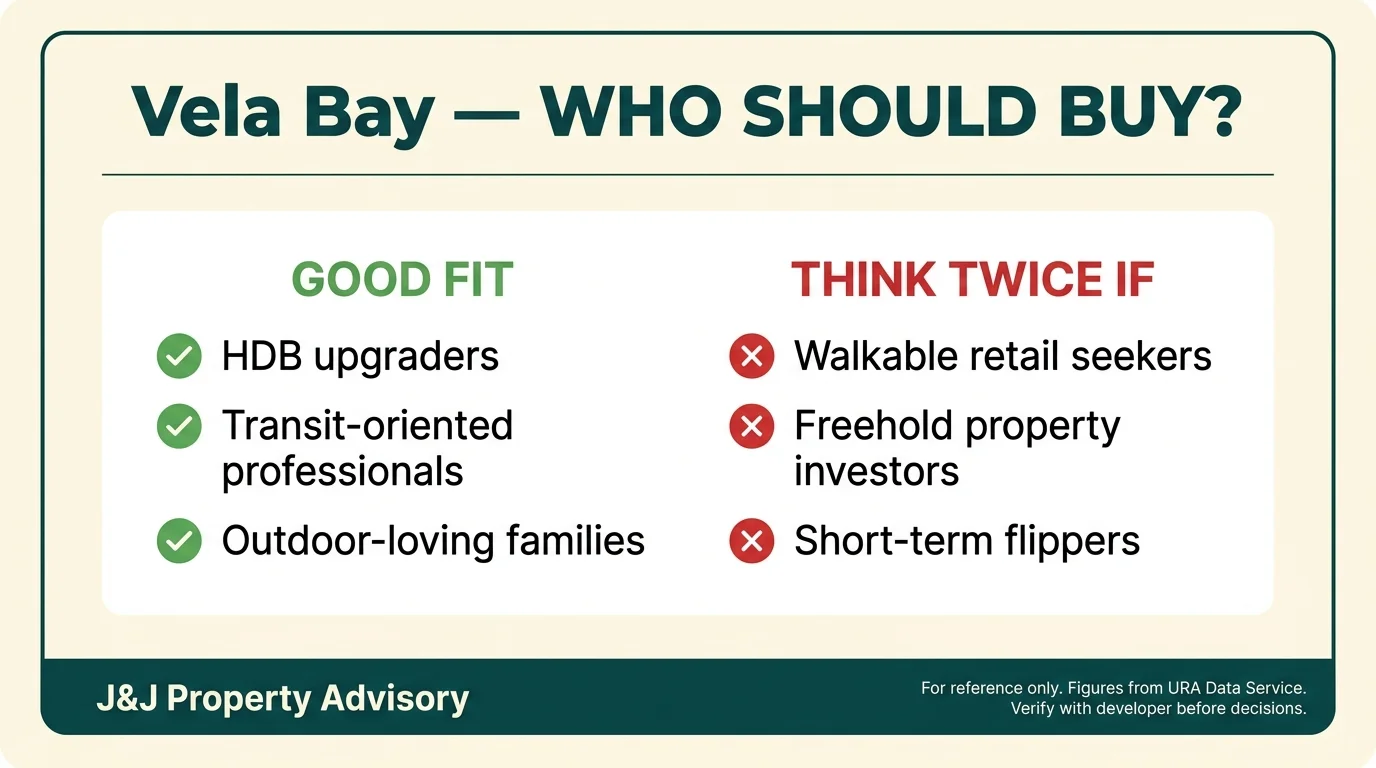

Who Is This For

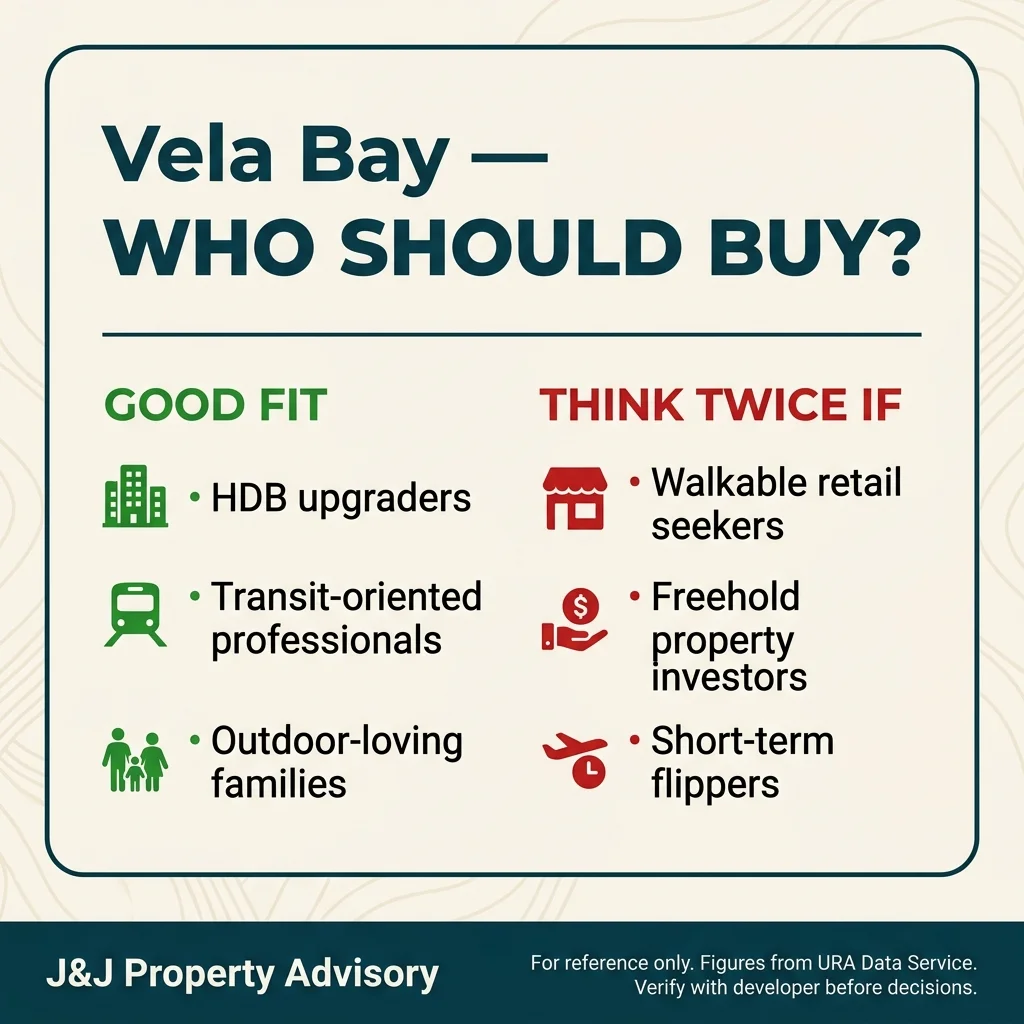

Good fit:

- HDB upgraders from Bedok, Tampines, or Pasir Ris with S$400k-S$600k equity and combined monthly income above S$12,000, seeking MRT-adjacent coastal lifestyle within familiar eastern corridor roots

- Young professionals and dual-income couples prioritising TEL connectivity to CBD, Marina Bay, and Orchard, willing to trade precinct immaturity for early-mover positioning in a URA masterplan precinct

- Own-stay families with children targeting Temasek Primary School (750 metres, within 1km priority admission), who value East Coast Park access for weekend recreation and cycling

- Buyers with 15-20 year hold horizons who can absorb precinct build-out timelines and benefit from infrastructure maturation (Bedok South MRT 2026, SAFRA clubhouse, Plus HDB projects)

- Investment buyers targeting S$4,500-S$5,500 monthly rental yields from young professionals and expat families, with 7-10 year capital appreciation strategies tied to Bayshore precinct value re-rating

Not ideal for:

- Budget-constrained upgraders with less than S$350k equity or combined income below S$10,000, who risk affordability strain if entry-level quantums exceed S$1.6M

- Families requiring immediate access to multiple primary schools within 1 kilometre, hawker centres within walking distance, or mature neighbourhood retail—Bedok Mall is 1.96km away and the immediate precinct lacks established amenities

- Freehold-focused buyers or multi-generational wealth planners who prioritise tenure permanence and long-term value retention beyond 60-70 years—the 99-year leasehold will experience depreciation after approximately 2086

- Risk-averse buyers uncomfortable with mid-tier developer track records, who prefer Tier 1 developers (CapitaLand, City Developments, Hongkong Land) with extensive mass-market condo portfolios and proven defect management

- Retirees or buyers seeking immediate estate maturity, established community networks, and full amenity provision at TOP—the 2030 completion occurs mid-way through the Bayshore precinct’s 10-year build-out cycle

Review Date: March 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This is a pre-launch analysis based on publicly available data. No official pricing or floor plans have been released by the developer. All pricing references are indicative only. This is not financial advice. Verify all details with the developer before making any purchase decisions.