Imagine choosing between a 1,200 sq ft unit in a mature estate requiring a $150,000 overhaul or a brand-new 800 sq ft unit with modern facilities and immediate move-in readiness. This scenario represents the core dilemma for many Singaporean families and investors in the current market. The decision often hinges on whether the lower entry price of an older resale property, combined with a significant renovation budget, can yield a better long-term return than the efficiency and convenience of a new launch. While the older unit offers the luxury of space, the new launch provides a contemporary lifestyle with potentially lower initial friction. I often observe that buyers underestimate the complexity of a total overhaul, viewing it merely as an aesthetic exercise rather than a structural restoration.

- Target resale condos where total cost (purchase + renovation) is at least 20% below comparable new launches, and only consider the deal if the new launch vs resale price gap exceeds 35% in your area

- Budget $120,000-$180,000 for gut renovation of a 1,200 sqft older unit, plus 15% contingency for hidden defects, with most costs requiring cash since renovation loans max out at $30,000

- Older condo maintenance fees run 20-30% higher than newer developments, and you need at least 70 years remaining lease to avoid CPF withdrawal restrictions and financing complications

The financial bridge between these two options has widened. As of Q4 2025, the price gap between new sale and resale properties in the Core Central Region (CCR) remains substantial. According to data reported by the Global Property Guide for Q3 2025, new sale average prices in the CCR reached SGD 3,208 psf, while resale average prices hovered around SGD 2,261 psf. This difference of nearly SGD 947 psf suggests that even with a heavy renovation budget, an older resale unit may offer a lower total quantum. However, the decision framework must account for more than just the purchase price. Factors such as lease decay, maintenance fund health, and the opportunity cost of renovation time play critical roles in determining the final ROI.

Price Trends: New Launch vs Resale Condos 2021–2026

The trajectory of Singapore’s private residential market has shown resilience despite various cooling measures. Based on URA flash estimates reported by The Straits Times on 2 January 2026, overall private residential prices rose by 3.4% across the full year of 2025. This growth followed a moderate Q4 2025 price increase of 0.7%. Within this upward trend, the premium for new launches has been driven by high land acquisition costs and rising construction expenditures. Historically, new launches have commanded a premium of 20% to 40% over resale counterparts in the same district, a trend that persisted through the 2021–2025 period.

For buyers, the price trend analysis reveals a distinct behavior in the resale market. While new launch prices are often set by developers based on land tender prices from one to two years prior, resale prices are more sensitive to immediate market sentiment and interest rate fluctuations. In 2025, the resale market saw steady volume as buyers sought larger floor plates that are increasingly rare in new developments. However, the capital appreciation of older resale units has historically trailed behind new launches during the first five to seven years of a project’s life cycle. Data from URA Realis for Q4 2025 indicates that projects approaching their Temporary Occupation Permit (TOP) often see a secondary price surge, which older developments rarely replicate unless they become collective sale candidates.

The price gap is particularly evident when comparing specific regions. In the Rest of Central Region (RCR), the price index for new sales has outpaced resale units by an estimated 12% over the last three years, based on historical URA price index trends. This makes the older resale unit an attractive proposition for those prioritizing a lower mortgage quantum or a larger living space for multi-generational needs. Buyers must weigh this lower entry cost against the reality that resale properties usually require a higher cash outlay for the downpayment and renovation, as the latter cannot be financed through a standard home loan.

Practical takeaway: Analyze the price gap between new launch and resale units within a 1 km radius over the same property type and comparable district; if the gap exceeds 35%, the older resale unit may offer a meaningful buffer to absorb renovation costs and potential market corrections.

Calculating the True Cost of Renovation for Older Units

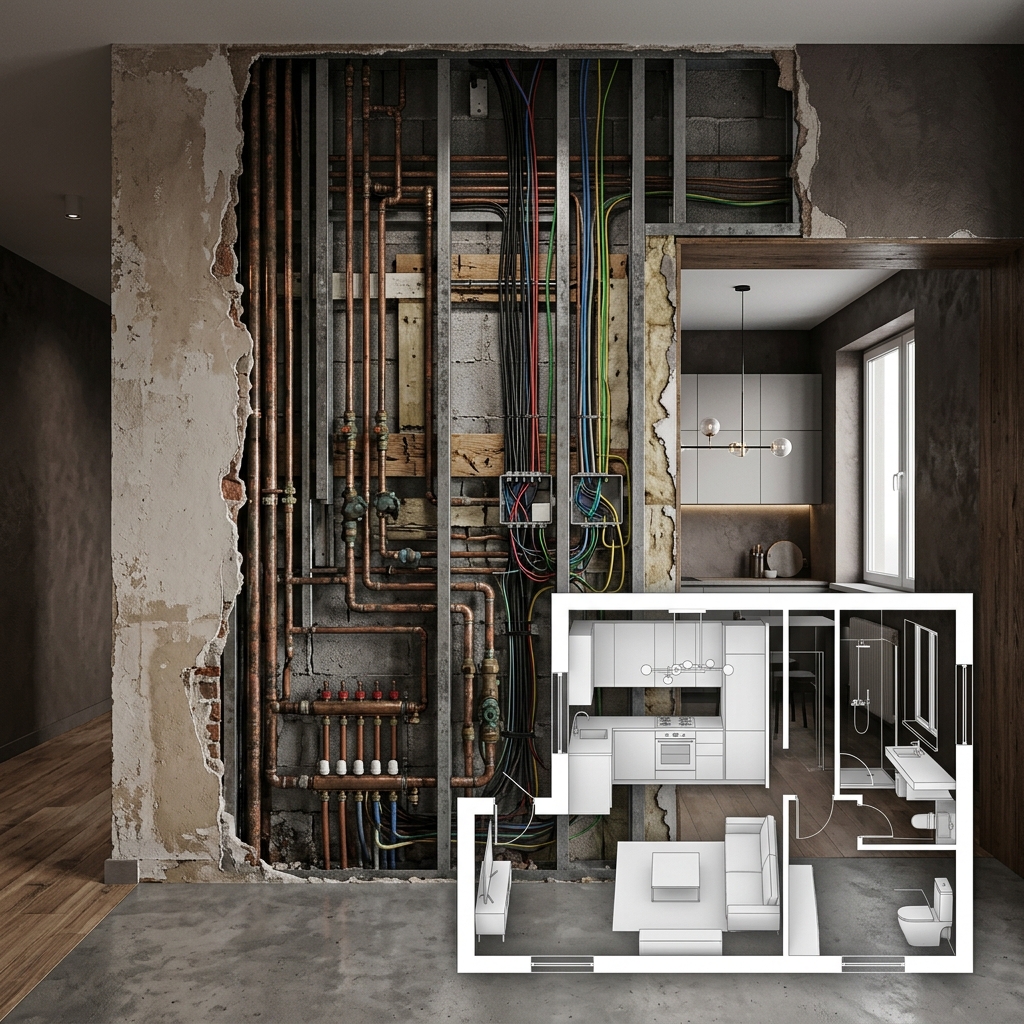

Renovating a property that is 20 years or older involves expenses that go far beyond new cabinetry or flooring. The actual cost of restoring electrical and plumbing systems in older resale units often exceeds aesthetic renovation budgets and should be factored into your entry price. For a 1,200 sq ft apartment, a “gut renovation” — which includes hacking, re-wiring, re-piping, and moisture-proofing — can range from an estimated $120,000 to $180,000 based on industry contractor estimates as of early 2026. While granular data on average renovation cost per square foot is not centrally tracked by authorities such as URA or BCA, industry estimates suggest material and labor costs rose by approximately 15% to 20% between 2023 and 2026.

Buyers often overlook the “invisible” costs. Older developments may have aging central air-conditioning systems or specific management corporation (MCST) guidelines that restrict renovation hours, thereby extending the project timeline and increasing labor costs. Hidden defects such as spalling concrete or water seepage from the unit above may only be discovered after hacking begins. These contingencies can add an estimated 10% to 15% to the initial renovation quote. In contrast, a new launch unit comes with a one-year defects liability period, where the developer is responsible for rectifying flaws, effectively capping the initial move-in cost to basic furnishing.

Another factor is the financing of these costs. While a home loan covers the property purchase, renovation loans in Singapore are typically capped at $30,000 or six times the applicant’s monthly income, whichever is lower, per MAS-regulated guidelines applicable to licensed financial institutions. This means a $150,000 renovation requires at least $120,000 in cash reserves. When this cash is added to the 25% downpayment applicable to a first property purchase under current LTV rules (Source: MAS Notice 632, effective 2023), the initial liquidity requirement for an older resale unit can sometimes exceed that of a new launch, despite the lower purchase price. Cash flow management consequently becomes the primary hurdle when deciding whether to upgrade from an HDB flat to a private condominium.

Practical takeaway: Always set aside a contingency fund of at least 15% above your renovation quote for structural repairs in units older than 15 years to avoid mid-project financial strain.

Comparing Rental Yields and Capital Appreciation Potential

Rental yields for older resale condos often appear higher on paper due to the lower purchase price. However, the net yield — after accounting for higher maintenance fees and more frequent repair costs — can be comparable to or lower than new launches in the same submarket. Tenants in 2025 and early 2026 have shown a preference for newer developments with modern gym facilities, energy-efficient appliances, and smart-home integrations, a trend supported by rental transaction data from URA Realis (Q4 2025). This demand allows new launches to command a rental premium that may offset their higher entry price over a holding period of five to seven years.

Have a question about this? WhatsApp Joe — no obligations, just clarity.

Capital appreciation in older units is frequently tied to the potential for an en-bloc sale. Without a successful collective sale, the appreciation of a 99-year leasehold property typically slows as the remaining lease drops below 60 years. This is due to CPF usage restrictions and tightening loan-to-value (LTV) limits for subsequent buyers, as governed by CPF Board housing rules and MAS Notice 632. New launches, conversely, benefit from the “first-mover advantage.” As the developer raises prices across subsequent phases, early buyers can see an immediate paper gain. Based on URA Realis data for Q3 2025, properties transacted within the first three years post-TOP showed an estimated average price increase of 8% to 12% compared to their launch prices, though outcomes vary by project and market conditions.

For the older unit to match the ROI of a new launch over a comparable holding period, the renovation must be strategic. High-quality finishes in kitchens and bathrooms tend to preserve value better than highly customized built-in furniture that may not suit the next buyer’s taste. The underlying approach is to acquire at a meaningful discount to the district’s average psf, renovate to a contemporary standard, and plan an exit before lease decay becomes a primary concern for the next generation of buyers. If the unit is freehold, the capital preservation aspect is significantly stronger, given that freehold land is not subject to the same CPF and LTV restrictions as shorter-lease leasehold properties.

Practical takeaway: Target resale units where the total cost (purchase price plus estimated renovation) is at least 20% below the nearest comparable new launch to maintain competitive rental yield potential and a viable exit price within a defined holding period.

Maintenance and Facilities: Understanding Depreciation in Older Developments

Maintenance fees in Singapore condominiums are based on share value, but the actual expenditure of the MCST often rises as a building ages. Older developments typically incur higher utility consumption due to dated pump systems and communal lighting. Furthermore, the sinking fund — a reserve mandated for major works such as repainting or lift replacement — may require higher contributions if previous management committees did not plan adequately. While comprehensive longitudinal data on maintenance fee escalation is not publicly tracked in a centralized government database, it is not uncommon to observe older projects with monthly fees estimated at 20% to 30% higher than newer, more efficient developments with a similar facility count.

Facilities in older condos, while often more spacious, may lack the lifestyle appeal of modern developments. A gymnasium or function room that is 20 years old may not attract the same caliber of tenants or buyers as a new launch featuring co-working spaces, gourmet pavilions, or lap pools meeting contemporary standards. This physical depreciation affects the property’s desirability over time. The cost of maintaining expansive grounds in older developments can become a burden, gradually leading to a decline in upkeep quality if the sinking fund is insufficient.

Conversely, new launches are built to current construction standards under BCA guidelines, often with Green Mark GoldPlus or Platinum certification that supports lower long-term utility costs. Buyers should remain aware, however, that highly complex facilities — such as extensive water features or automated parking systems — may generate higher maintenance costs once initial warranty periods expire. These nuances matter when evaluating price per square foot as the sole acquisition metric.

Practical takeaway: Review the last three years of the development’s Annual General Meeting (AGM) minutes to identify any planned special levies, significant sinking fund shortfalls, or pending major repair works before committing to purchase.

Transaction Timelines and Financing Considerations

The timeline for purchasing a resale unit is significantly shorter than that of a new launch. A resale transaction typically concludes within 10 to 12 weeks, allowing for relatively prompt occupation or rental income generation. However, if a major renovation is planned, this effective timeline extends by four to six months. During this period, the owner must service the full mortgage while simultaneously funding renovation works and potentially alternative accommodation — a “double carry” cost that can place meaningful pressure on cash reserves.

New launches utilize the Progressive Payment Scheme (PPS), which allows buyers to pay for the property in stages tied to construction milestones, as governed by the Housing Developers (Control and Licensing) Act. For a project under active construction, the initial monthly mortgage obligation is proportionally lower, as it is calculated only on the amount disbursed to date. This can be advantageous for buyers who are currently renting or need time to consolidate finances. The trade-off is the construction period itself; a project launched in 2026 may not receive its TOP until 2029 or 2030, based on typical build timelines observed in recent Singapore launches.

Financing a resale property also involves a more rigid valuation process. Banks will grant loans based on the lower of the purchase price or the professional valuation. If a buyer pays a Cash Over Valuation (COV) amount for a well-renovated unit, that excess must be funded entirely in cash. For older leasehold units, if the remaining lease does not cover the youngest buyer to at least the age of 95, both the CPF amount that can be applied toward the purchase and the maximum LTV ratio will be pro-rated, per CPF Board housing withdrawal rules (updated 2019, applicable as at 2026). This makes the new launch a structurally cleaner financial transaction for many buyers, as the lease tenure is fresh and the pricing is fixed at the point of booking.

Practical takeaway: Use the Progressive Payment Scheme of a new launch to manage monthly cash flow during the construction phase; opt for resale if immediate rental income is required to service the mortgage from an earlier date.

| Attribute | Older Resale Condo | New Launch Condo |

|---|---|---|

| Initial Capital Outlay | Higher (Purchase + Full Renovation in Cash) | Lower (Progressive Payments during construction) |

| Renovation Requirement | Extensive (Aesthetic + Mechanical and Electrical) | Minimal (Fitting out only) |

| Immediate Rental Readiness | Delayed (Estimated 4–6 months post-purchase) | Delayed (Estimated 3–4 years construction) |

| Facilities and Modern Technology | Dated (Potentially higher upkeep cost) | Modern (Smart home integration, energy efficiency) |

| Depreciation Risk | Higher (Lease decay and physical aging) | Lower (Newest-generation construction standards) |

Risks and Considerations

1. Renovation Budget Overruns

A primary risk in older resale units is the discovery of structural issues after the purchase is finalized. Concealed pipe leakage or compromised electrical load capacity can materially increase the final renovation cost beyond initial estimates.

- Mitigation: Conduct a thorough pre-purchase inspection with a licensed professional surveyor or experienced contractor before exercising the Option to Purchase (OTP).

2. Lease Decay and Financing Limits

For leasehold properties, CPF Board’s pro-ration rules on housing withdrawals and the associated tightening of LTV ratios can restrict the pool of future buyers as the building approaches the 30-year mark, potentially leading to price stagnation or the need for a meaningful discount at exit.

- Mitigation: Focus on resale leasehold properties with at least 70 years of remaining lease, or prioritize freehold options if the intended holding period exceeds 15 years.

3. Construction Delays for New Launches

While Singapore’s regulatory environment under URA and BCA maintains strong developer accountability, global supply chain disruptions or labor shortages may cause delays to the expected TOP date, affecting move-in planning and extending the cost of alternative accommodation.

- Mitigation: Ensure the Sale and Purchase Agreement (S&P) includes clear liquidated damages clauses, and build at least six months of timeline buffer into your move-in planning.

4. MCST Mismanagement and Special Levies

An older development with an underfunded sinking fund may impose a special levy for major works such as roof waterproofing or facade repairs. These one-time assessments can range from an estimated $10,000 to $50,000 per unit depending on the scope of works.

- Mitigation: Request the latest MCST financial statements — including sinking fund balance and recent AGM resolutions — to assess whether reserves are adequate relative to the building’s age and maintenance needs.

5. Interest Rate Sensitivity

With mortgage rates subject to global monetary conditions, the long-term cost of borrowing remains a material variable. Both a high-quantum new launch purchase and a high-renovation resale carry significant compounding interest burdens over a 25-year loan tenure.

- Mitigation: Stress-test your finances at a 5% per annum interest rate and maintain a cash emergency fund sufficient to cover at least 12 months of mortgage payments, independent of rental income.

Data Sources

- Tier 1 — Government: URA Realis (Q3 2025; Q4 2025 flash estimates); BCA Green Mark Certification Records (2025); CPF Board Housing Withdrawal Rules (updated 2019, applicable as at 2026); MAS Notice 632 on Residential Property Loans (effective 2023); Housing Developers (Control and Licensing) Act (Cap. 130).

- Tier 2 — Established Media: The Straits Times (2 January 2026, reporting on URA full-year 2025 and Q4 2025 flash estimates); Global Property Guide (Q3 2025 average psf data, CCR new sale and resale).

- Tier 3 — Industry: Construction and renovation cost estimates based on historical contractor market trends, Singapore (2023–2026); rental demand observations from URA Realis transaction records (Q4 2025).

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence No.: L3010738A

Contact: +65 8098 0916

This article is for general reference only and does not constitute financial, legal, or investment advice. Verify all details with relevant authorities before making decisions.

Frequently Asked Questions

How much does it cost to renovate a 1200 sqft older condo in Singapore 2026?

A gut renovation for a 1,200 sq ft apartment that is 20+ years old ranges from $120,000 to $180,000, including hacking, re-wiring, re-piping, and moisture-proofing. Always budget an additional 15% contingency for hidden defects discovered during renovation.

What is the price difference between new launch and resale condos in Singapore CCR 2025?

As of Q4 2025, new launch condos in the Core Central Region averaged SGD 3,208 psf while resale units averaged SGD 2,261 psf – a difference of nearly SGD 947 psf. If the gap exceeds 35% in your target area, the resale unit may offer meaningful savings even after renovation costs.

Can I use home loan to finance condo renovation costs in Singapore?

No, renovation loans are separate from home loans and capped at $30,000 or 6x monthly income (whichever is lower). For a $150,000 renovation, you need at least $120,000 in cash reserves on top of your property downpayment.

How much do Singapore private condo prices increase per year 2025?

Overall private residential prices rose 3.4% in 2025 according to URA data. New launches within 3 years post-TOP showed 8-12% price increases compared to launch prices, while older resale units typically appreciate slower unless they become collective sale candidates.

What is the minimum lease remaining to use full CPF for condo purchase Singapore?

For leasehold properties, if the remaining lease doesn’t cover the youngest buyer to age 95, both CPF withdrawal amounts and maximum loan-to-value ratios are pro-rated. Focus on properties with at least 70 years remaining lease to avoid financing restrictions.

Need Clarity on Your Next Property Move?

One message. No obligations. We’ll help you see the full picture.