Launched Analysis

Before you read the numbers, here is my view:

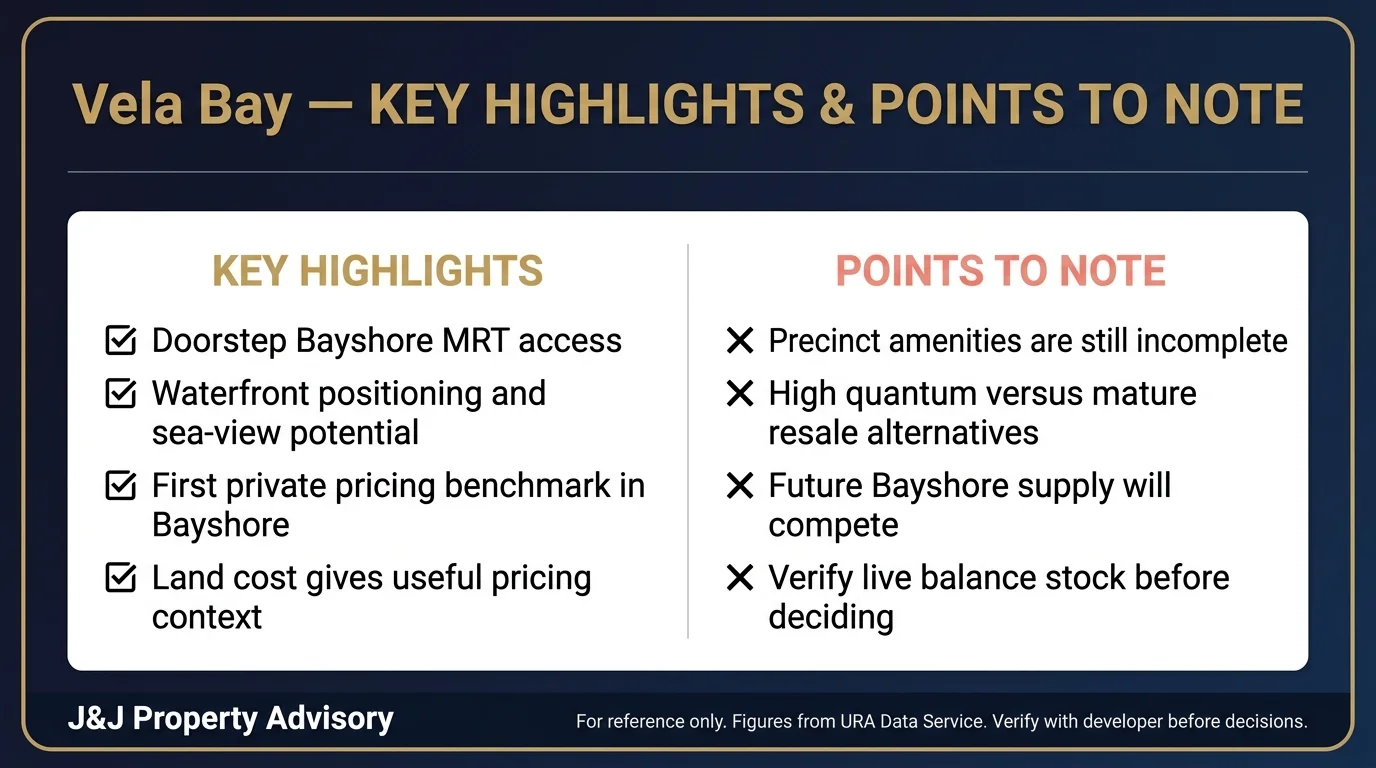

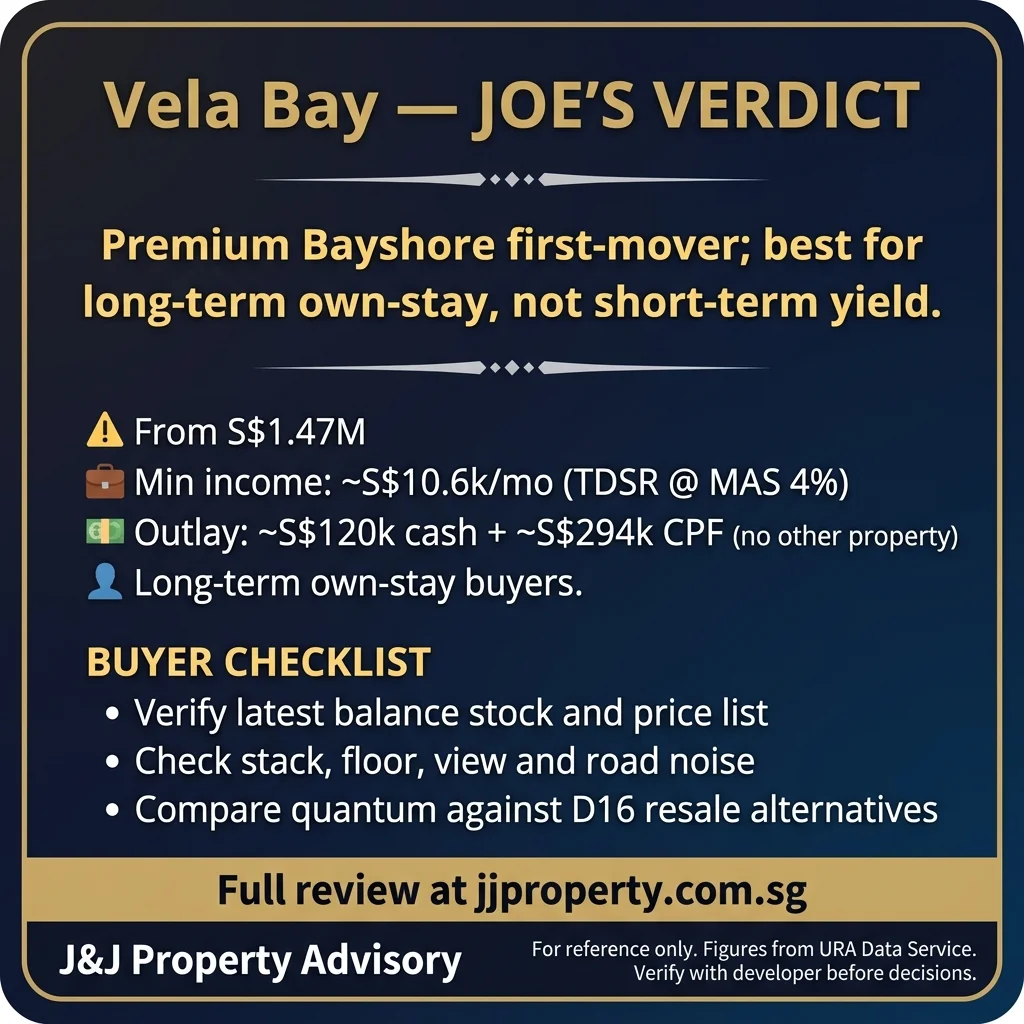

Vela Bay is a first-mover bet on an unproven precinct. You are paying a premium for doorstep MRT access and seafront positioning in a masterplan that has yet to materialise fully.

Public balance-unit data showed 374 units sold, 140 units shown as available and 1 unreleased as of 31 May 2026, so demand is validated but balance stock is still meaningful, especially in larger formats. Buyers need to separate launch hype from actual value against mature resale alternatives that may trade meaningfully lower on a PSF basis.

This review breaks down where the value is — and where buyers need to be careful.

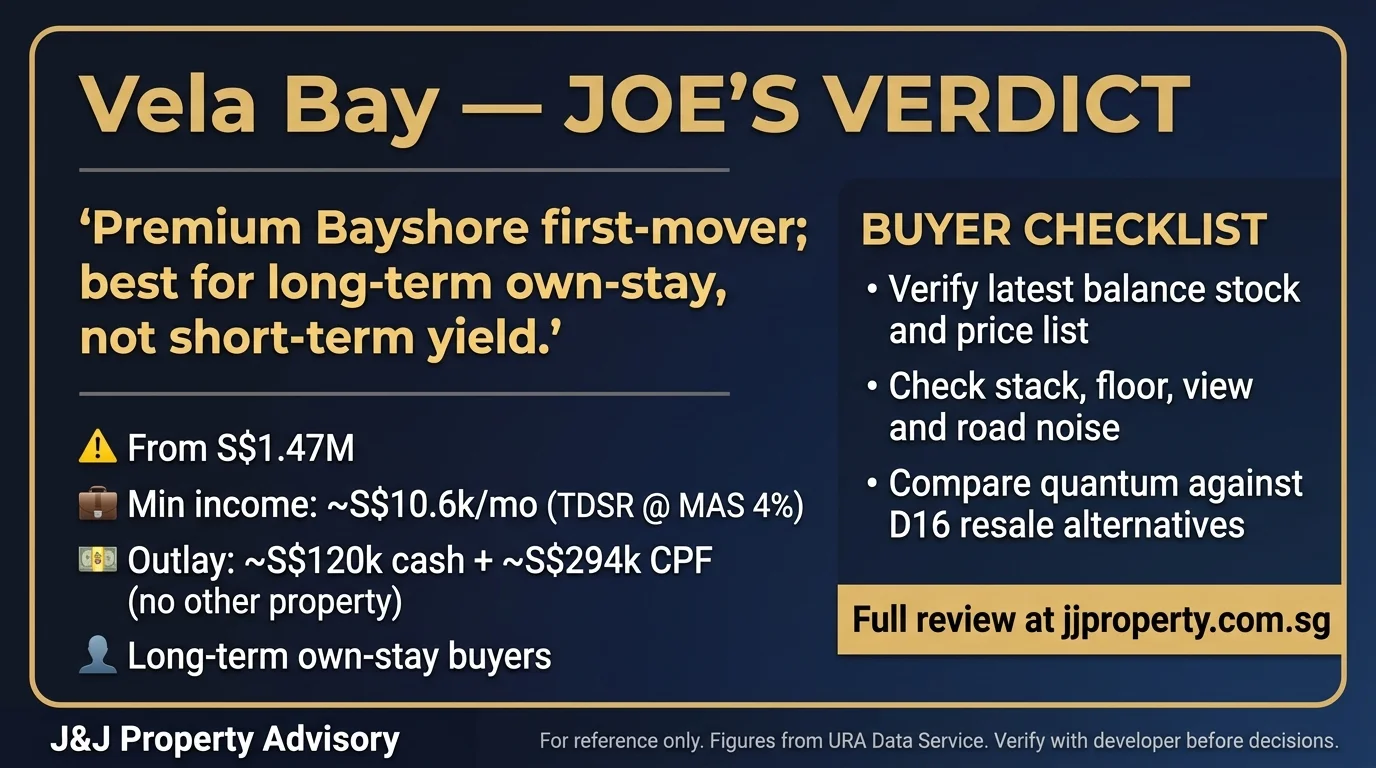

Bottom Line

Vela Bay is a calculated bet on the Bayshore precinct transformation, with URA caveat median pricing about 14 percent above the District 16 median. The MRT integration and seafront positioning are genuine strengths, but the precinct is unproven, amenities are incomplete, and the quantum sits at the upper end of Outside Central Region pricing. Public tracker data validates demand, but the absorption was concentrated in smaller units, and balance stock remains meaningful in higher-quantum formats.

For Own-Stay Buyers:

If you are willing to absorb 5 to 7 years of precinct development risk and prioritise MRT-integrated, car-lite living with unobstructed sea views, Vela Bay is defensible. The first-mover advantage gives you early exposure to Bayshore before the precinct is fully built, but it does not guarantee future outperformance. If you need mature amenities, established schools and immediate neighbourhood character, you may be better served by resale alternatives in Marine Parade or the Katong belt that trade meaningfully lower on a PSF basis. Do not buy this project if you expect a fully-formed township on move-in day.

For Investment Buyers:

The rental yield will likely be compressed due to premium pricing, and the four-year SSD schedule makes short exits less attractive. The precinct upside is real, but the timeline is uncertain, and future government land sales will introduce competing supply under different market conditions. If you are looking for immediate rental income or near-term capital appreciation, this is not the play. Buy only if you have a long holding horizon and believe the masterplan will deliver institutional-grade mixed-use development.

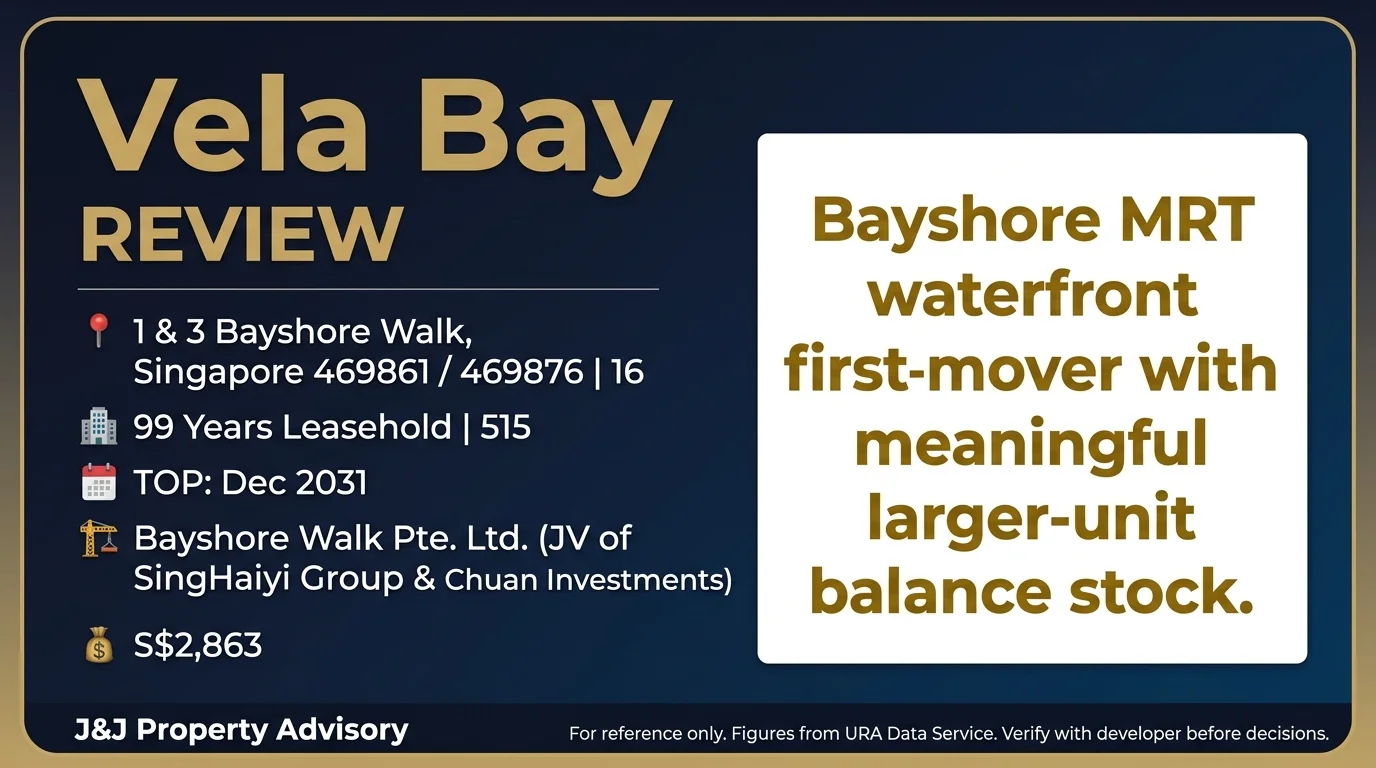

Project Snapshot

| Attribute | Details |

| Site Area | 112,991.9 sqft / 10,497.3 sqm |

| Developer | Bayshore Walk Pte. Ltd. (JV of SingHaiyi Group & Chuan Investments) |

| Tenure | 99 Years Leasehold |

| Total Units | 515 |

| Launch Date | 25 Apr 2026 |

| URA Median PSF | S$2,863 (371 caveats at launch) |

| Sales Status | Public tracker: 374 / 515 sold, 140 shown as available, 1 unreleased (updated 31 May 2026) |

Vela Bay sits within the newly planned Bayshore neighbourhood, where URA has outlined future housing, an integrated transport hub, a central park, a school and a transit-priority corridor. The site is directly above Bayshore MRT (TE29), with approximately 70 percent of units marketed as sea-facing and unobstructed views from the 11th storey upward. The project represents the first large-scale private residential launch in this precinct, giving it first-mover advantage but also exposure to untested infrastructure and neighbourhood maturity.

Location & Connectivity

1. Bayshore MRT (TE29) – approximately 110m

The station is effectively at your doorstep, accessible via sheltered connection. The key value is direct Thomson-East Coast Line access toward Shenton Way, Marina Bay and Orchard without needing a feeder bus. This is genuine MRT-integrated living, not a 10-minute walk marketed as “near MRT”.

2. Bedok South MRT (TE30) – approximately 890m

A secondary option for eastward connectivity as the remaining Thomson-East Coast Line stages complete. For airport access, buyers should check the actual routing and transfer requirements rather than assuming a single-seat trip.

3. East Coast Park – direct sheltered access

The developer markets a covered linkway to the park, a material amenity for families and fitness-focused buyers. East Coast Park’s 15km cycling and running routes, beaches, and hawker centres are a genuine lifestyle draw, not a sales gimmick.

4. School proximity – limited within 1km

Temasek Primary School sits approximately 750m away, which may help under MOE home-school distance priority if balloting is required. This does not guarantee admission or create Phase 2B eligibility by itself. Bedok Green Primary School is approximately 1.38km away. Secondary school options in the immediate vicinity are thin, so families prioritising school strategy need to check the exact registration rules and address eligibility.

5. Retail and daily amenities – still developing

Bedok Mall is approximately 1.96km away. The Bayshore precinct masterplan includes future retail and community facilities, but these have yet to materialise. Early residents should expect to rely on Bedok Mall or Marine Parade for groceries and services.

6. Expressway access – ECP within 1km

The East Coast Parkway is nearby, offering fast access to the CBD and Changi Airport. However, peak-hour congestion on this corridor is chronic, particularly during morning and evening commutes. If you are driving to the CBD daily, budget for delays.

Sales Performance

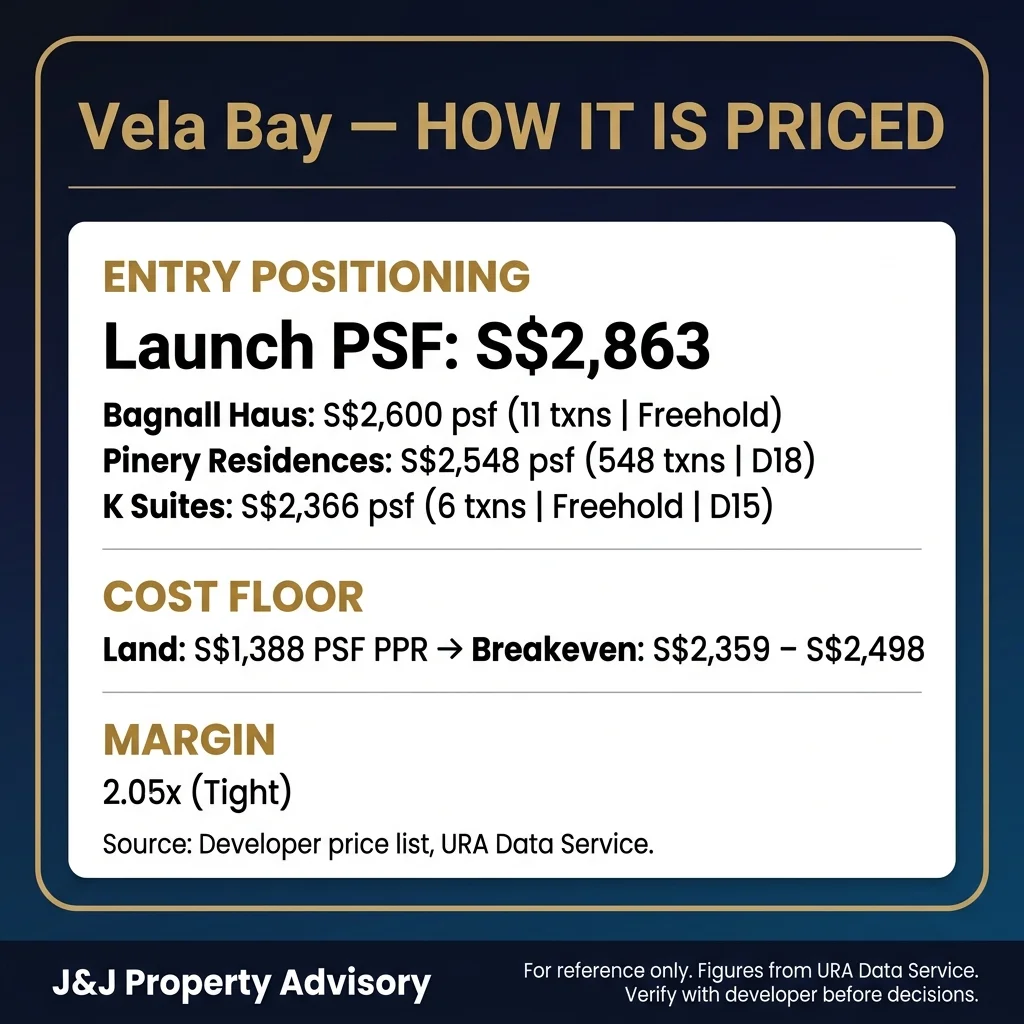

Vela Bay launched on 25 April 2026. A public balance-unit tracker updated on 31 May 2026 showed 374 / 515 units sold, 140 units shown as available and 1 unreleased; treat this as public tracker data rather than live developer-confirmed availability. URA’s developer-sales snapshot records 370 units sold in the April 2026 launch period, while URA caveats show a transacted median of S$2,863 PSF across 371 caveats, with a range of S$2,532 to S$3,302 PSF. This is a strong debut, particularly for a project in an unproven precinct with no mature amenities.

The district median for condos and apartments in District 16 stands at S$2,517 PSF (1,481 transactions), meaning Vela Bay’s URA caveat median sits about 14 percent above the district median. This premium reflects the MRT integration, seafront positioning, and new-development specifications.

However, buyers should note the difference between median and average pricing. Media launch coverage cited average prices around S$2,886 PSF, while the URA caveat median used here is S$2,863 PSF. The 371 caveats were concentrated in the launch phase, and the transacted median includes early-bird units likely priced below current asking rates. Remaining balance stock is priced higher, with developer asking prices ranging from S$2,721 PSF (4-bedroom units) to S$3,249 PSF (penthouse).

The important point is not to extrapolate the launch spike as a normal monthly run-rate. The current buyer decision is different from launch weekend: smaller units are largely absorbed, while remaining choice is more meaningful in higher-quantum formats. Future sales velocity will depend on how quickly the precinct matures and whether subsequent buyers remain willing to pay a premium for first-mover positioning.

HDB Upgrader Catchment

Vela Bay sits within the Bedok and Tampines HDB catchment, where recent 24-month resale data pulled on 30 May 2026 shows 4-room flats at a median of S$655,000 and 5-room flats at S$808,000. This gives some upgraders a meaningful equity base, but the actual cash-and-CPF position still depends on outstanding loan, CPF usage, accrued interest and sale proceeds.

For upgraders targeting 2-bedroom units, the quantum ranges from S$1.675M to S$2.087M, requiring approximately S$420,000 to S$520,000 in cash and CPF for the 25 percent downpayment, excluding BSD, legal fees and any ABSD if applicable. This may be within reach for some 4-room and 5-room sellers with clean CPF balances and moderate savings, but it is not automatic. The 1-bedroom plus study units, priced from S$1.466M, are the most accessible entry point, though only 8 units are shown as available out of 27 total in the public balance tracker.

The 2-bedroom units have seen near-total absorption (92.9 percent for standard 2-bedroom, 91.2 percent for 2-bedroom premium), signalling that upgraders were the dominant buyer segment at launch. Remaining 2-bedroom stock is tight, with only 6 standard and 10 premium units left.

Unit Mix & Pricing

| Unit Type | Size (sqft) | Price From | Price To | PSF From | PSF To | Available | Sold % |

| 1BR + Study | 484 | S$1,466,000 | S$1,553,000 | S$3,029 | S$3,209 | 8 / 27 | 70% |

| 2BR | 592 | S$1,675,000 | S$1,710,000 | S$2,829 | S$2,889 | 6 / 84 | 93% |

| 2BR Premium | 678-689 | S$1,890,000 | S$2,087,000 | S$2,743 | S$3,029 | 10 / 113 | 91% |

| 3BR | 883-893 | S$2,314,000 | S$2,676,000 | S$2,591 | S$3,031 | 10 / 87 | 89% |

| 3BR Premium | 1,033 | S$2,832,000 | S$3,093,000 | S$2,742 | S$2,994 | 35 / 88 | 60% |

| 4BR | 1,173 | S$3,192,000 | S$3,618,000 | S$2,721 | S$3,084 | 34 / 62 | 45% |

| 4BR (Pte Lift) | 1,378 | S$3,839,000 | S$4,362,000 | S$2,786 | S$3,165 | 16 / 26 | 39% |

| 5BR (Pte Lift) | 1,582 | S$4,543,000 | S$5,136,000 | S$2,872 | S$3,247 | 20 / 26 | 23% |

| Penthouse 1 | 1,765 | Unreleased | Unreleased | — | — | 0 / 1 | Unreleased |

| Penthouse 2 | 1,765 | S$5,735,000 | S$5,735,000 | S$3,249 | S$3,249 | 1 / 1 | 0% |

The 2-bedroom premium units (113 units, 22 percent of inventory) dominated the unit mix and saw the strongest take-up. Nearly all smaller 1-bedroom and 2-bedroom stock is gone, leaving buyers with primarily 3-bedroom, 4-bedroom and 5-bedroom options. The buyer profile has therefore shifted: early upgrader-friendly units were absorbed quickly, while today’s buyer is more likely comparing higher-quantum own-stay units against mature East Coast resale alternatives. The 3-bedroom premium units and larger 4-bedroom and 5-bedroom units offer the most choice, though the quantum climbs quickly above S$2.8M.

Balance stock is meaningful, particularly in the larger categories. Buyers shopping today should focus less on the launch headline and more on the specific remaining stack, facing, floor height, afternoon sun, road noise and whether any view premium is recoverable at resale. Verify live availability with the developer, as public balance-stock data can lag actual bookings by days.

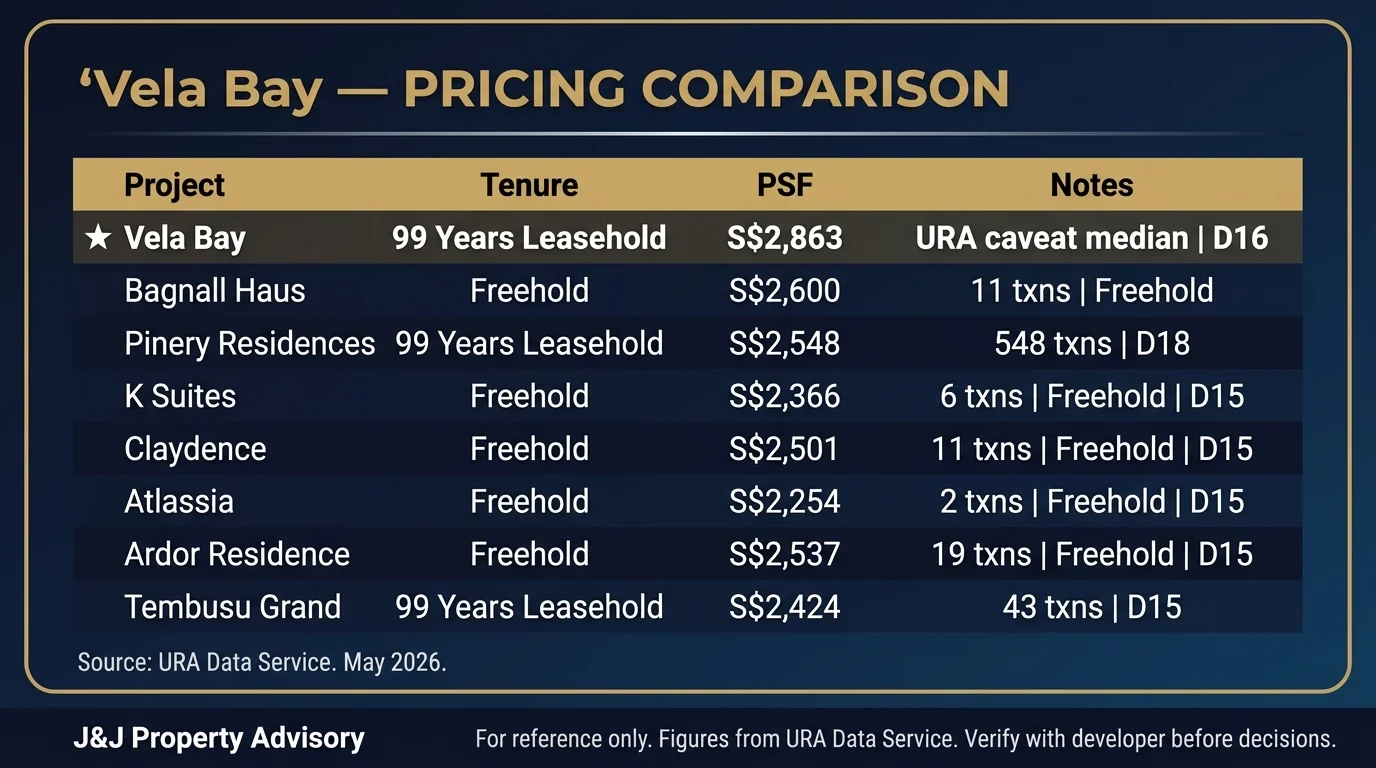

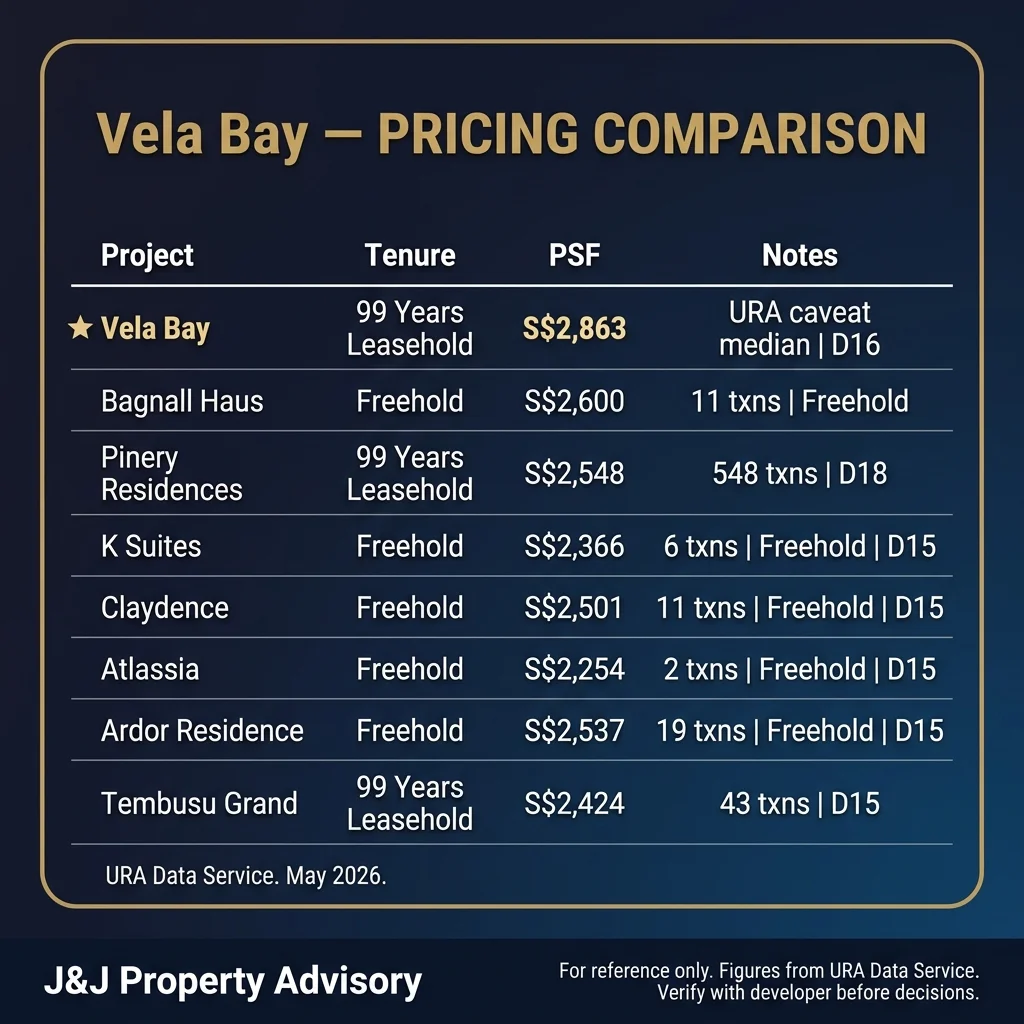

Comparables

| Project | Median PSF | Transactions | Tenure | Expected TOP |

| Bagnall Haus | S$2,600 | 11 | Freehold | Dec 2028 |

| Pinery Residences | S$2,548 | 548 | 99-Year | Q4 2029 |

| Ardor Residence | S$2,537 | 19 | Freehold | Oct 2026 |

| Tembusu Grand | S$2,424 | 43 | 99-Year | Oct 2028 |

| Claydence | S$2,501 | 11 | Freehold | 2026 Completed |

Vela Bay’s URA transacted median of S$2,863 PSF sits 10 to 18 percent above comparable 99-year leasehold projects like Pinery Residences (S$2,548 PSF) and Tembusu Grand (S$2,424 PSF). It also exceeds freehold projects like Bagnall Haus (S$2,600 PSF) and Ardor Residence (S$2,537 PSF), despite the tenure disadvantage.

The premium is justified primarily by MRT integration and seafront positioning, neither of which the comparables offer. Bagnall Haus is a boutique freehold project but sits inland without direct MRT access. Pinery Residences is MRT-integrated (Bedok South, TE30) but lacks the scale and waterfront narrative. Buyers paying the premium are effectively buying into the Bayshore masterplan upside, not the current state of the precinct.

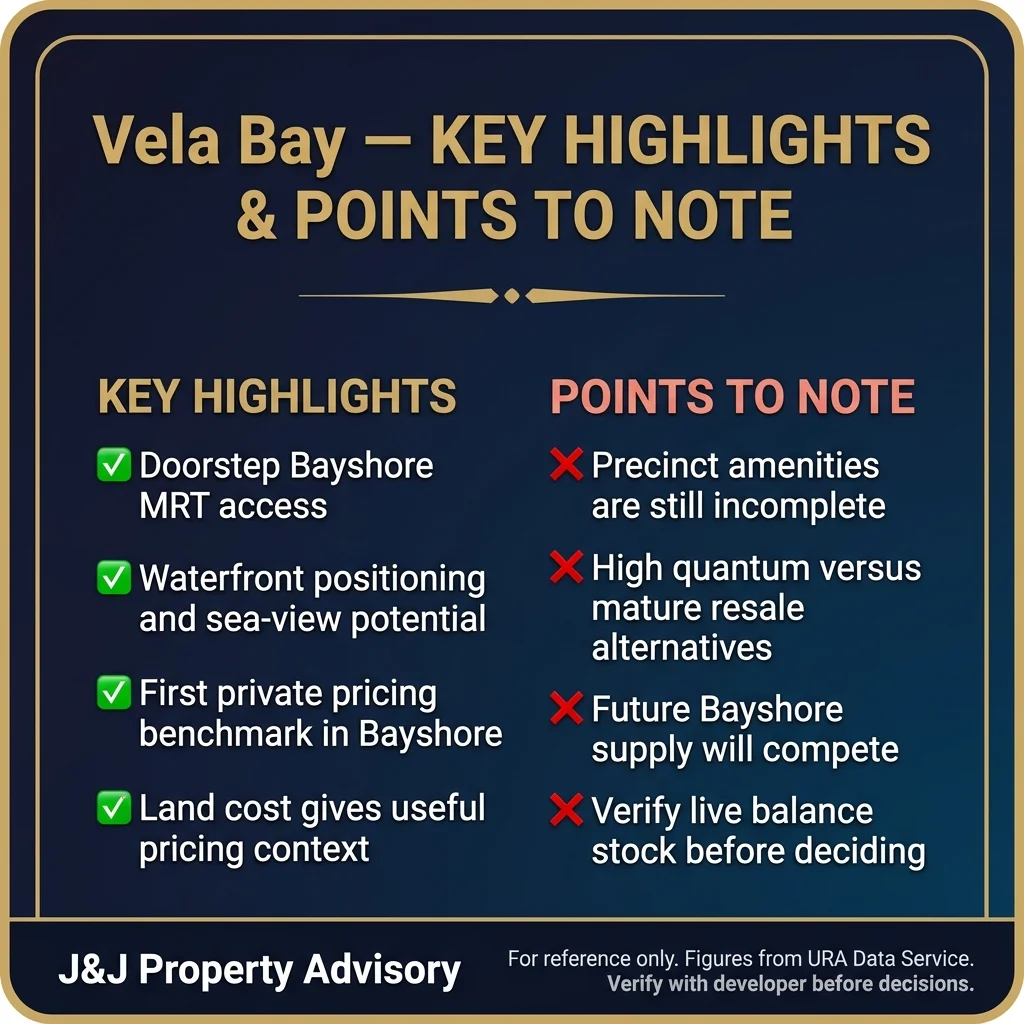

Key Strengths

1. Genuine MRT integration – 110m to Bayshore (TE29)

This is not “near MRT” marketing. The station is at your doorstep, with sheltered access and direct TEL connectivity toward the CBD, Marina Bay and Orchard. For buyers prioritising genuine car-lite living, this is a material differentiator.

2. Seafront positioning with unobstructed ocean views from mid-floors

Approximately 70 percent of units are marketed as sea-facing, with unobstructed views from the 11th storey upward. This is a rare offering in District 16, where most new launches are inland. The premium for sea-facing units can be real, but buyers should still verify exact stack, floor height, facing and future obstruction risk.

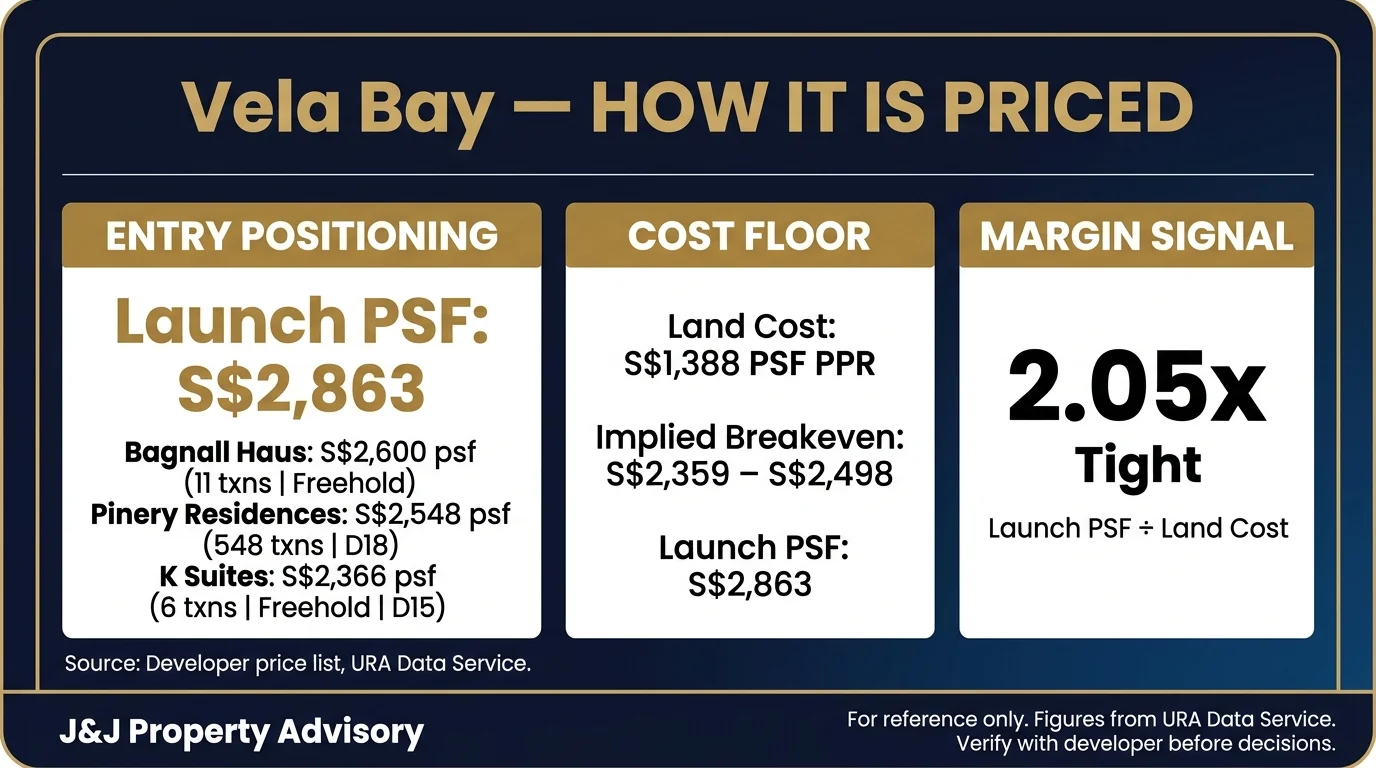

3. Land cost gives useful pricing context

Vela Bay’s land cost sits at S$1,388 PSF PPR, while current entry pricing starts from about S$2,591 PSF. That is roughly a 1.87x entry-price-to-land-cost multiple; using the URA caveat median of S$2,863 PSF, the multiple is about 2.06x. This gives buyers a useful reference point, but it does not automatically make the project cheap. The more important test is whether today’s remaining units are defensible against mature D16 resale alternatives and future Bayshore supply.

4. First pricing benchmark in Bayshore

Vela Bay is the first large-scale private residential project in the Bayshore precinct, so it sets an early private-condo price benchmark. That can be an advantage if the precinct matures well, but it is not a guarantee that future launches will be more expensive or more successful. Buyers are also absorbing first-mover risk while the retail, community and transport ecosystem is still incomplete.

5. Strong launch take-up validates demand

The public balance tracker showing 374 units sold out of 515 confirms that the market is willing to pay a premium for MRT integration and waterfront positioning. This is not a speculative project struggling to find buyers. However, the take-up was concentrated in smaller units, and larger 4-bedroom and 5-bedroom stock remains more selective.

Questions You Should Be Asking

1. What happens if the Bayshore precinct masterplan stalls or underdelivers?

The developer is selling the vision of a mixed-use waterfront township, but the reality today is limited retail, no mature amenities, and no established neighbourhood character. Future supply is also real: a larger Bayshore GLS site has already entered the pipeline, and future tender pricing, launch timing and unit mix will affect Vela Bay’s resale context. If the wider precinct rollout is delayed or underdelivers, Vela Bay buyers absorb that first-mover downside.

2. Why is the quantum so high relative to mature resale alternatives?

Older resale condos in District 16 can trade meaningfully lower on a PSF basis than Vela Bay’s asking price. Buyers need to decide whether the new-development premium is justified by MRT access and modern fittings, or whether they are overpaying for first-mover positioning.

3. Can the precinct support long-term rental yields?

Rental yield is likely to be compressed because the entry price is materially above many mature D16 resale alternatives. Investors should compare expected rents against actual resale rental comparables, not simply assume that the MRT and waterfront story will offset the premium. The precinct may attract tenants over time, but the rental case should be tested against actual asking rents and holding costs.

4. What is the exit strategy if you need to sell before the precinct matures?

The holding period matters because residential properties purchased from 4 July 2025 may face SSD if sold within the first four years. A short exit window should therefore be stress-tested, especially if the precinct is still incomplete when you need liquidity. If you need flexibility, this is a poor fit.

5. How exposed are you to peak-hour expressway congestion?

The ECP is nearby, but chronic congestion during rush hours is a known issue. If you are driving to the CBD daily, the MRT integration becomes critical. Buyers who assume they can drive everywhere should recalibrate expectations.

6. Are you paying for a view that will hold resale value?

About 70 percent of units are marketed as sea-facing, but not all view premiums are equal. Check exact stack, floor height, future obstruction risk, afternoon sun, road noise and whether the premium paid for view is recoverable at resale.

7. Why is the take-up rate so uneven across unit types?

The 2-bedroom units are about 91 to 93 percent sold in the public balance tracker, while larger 4-bedroom and 5-bedroom categories are materially slower. This signals that upgrader-friendly smaller formats dominated launch demand, while buyers targeting higher-quantum family units remained more selective. Buyers shopping for 4-bedroom or 5-bedroom units today should ask why uptake was weaker and whether the quantum is justified.

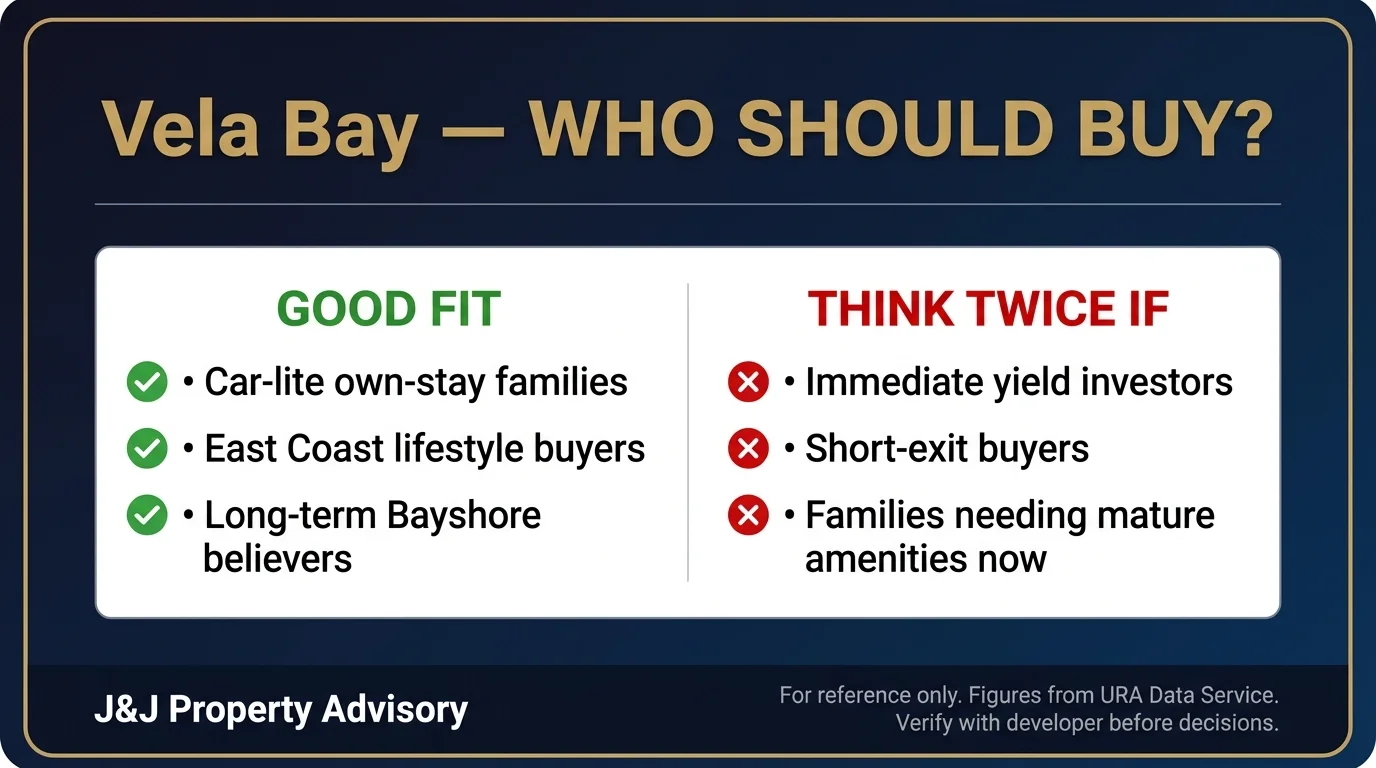

Who Is This For

Good fit:

- Own-stay families prioritising MRT-integrated, car-lite living at Bayshore (TE29), with direct TEL connectivity toward the CBD, Marina Bay and Orchard.

- HDB upgraders from Bedok or Tampines with sufficient sale proceeds, CPF and cash buffer, targeting 2-bedroom units in the S$1.675M to S$2.087M range (note: only 16 units are shown as remaining across both 2-bedroom types in the public balance tracker).

- Buyers willing to absorb 5 to 7 years of precinct development risk in exchange for first-mover pricing and unobstructed sea views from mid-floors upward.

- Fitness-focused or lifestyle buyers who place material value on direct sheltered access to East Coast Park’s 15km cycling and running routes.

- Long-term holders with 10-year investment horizons who believe the Bayshore masterplan will deliver material precinct upside.

Not ideal for:

- Families prioritising school admission certainty – Temasek Primary is within roughly 1km, but distance priority is not the same as guaranteed admission or Phase 2B eligibility.

- Buyers expecting mature retail, F&B, and community amenities on move-in – the precinct is incomplete and Bedok Mall (1.96km) remains the primary option.

- Investors seeking immediate rental yield or near-term capital appreciation – the 4-year SSD and premium pricing compress returns materially.

- Buyers requiring liquidity or flexibility – selling within the first four years may trigger SSD, and the precinct may still be incomplete when you need to exit.

- Cost-conscious buyers who can accept older resale stock in Marine Parade or Katong at meaningfully lower PSF with mature amenities and immediate neighbourhood character.

Review Date: May 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This review is based on publicly available data and official URA transaction records. It is not financial advice. Verify all details with the developer before making purchase decisions.