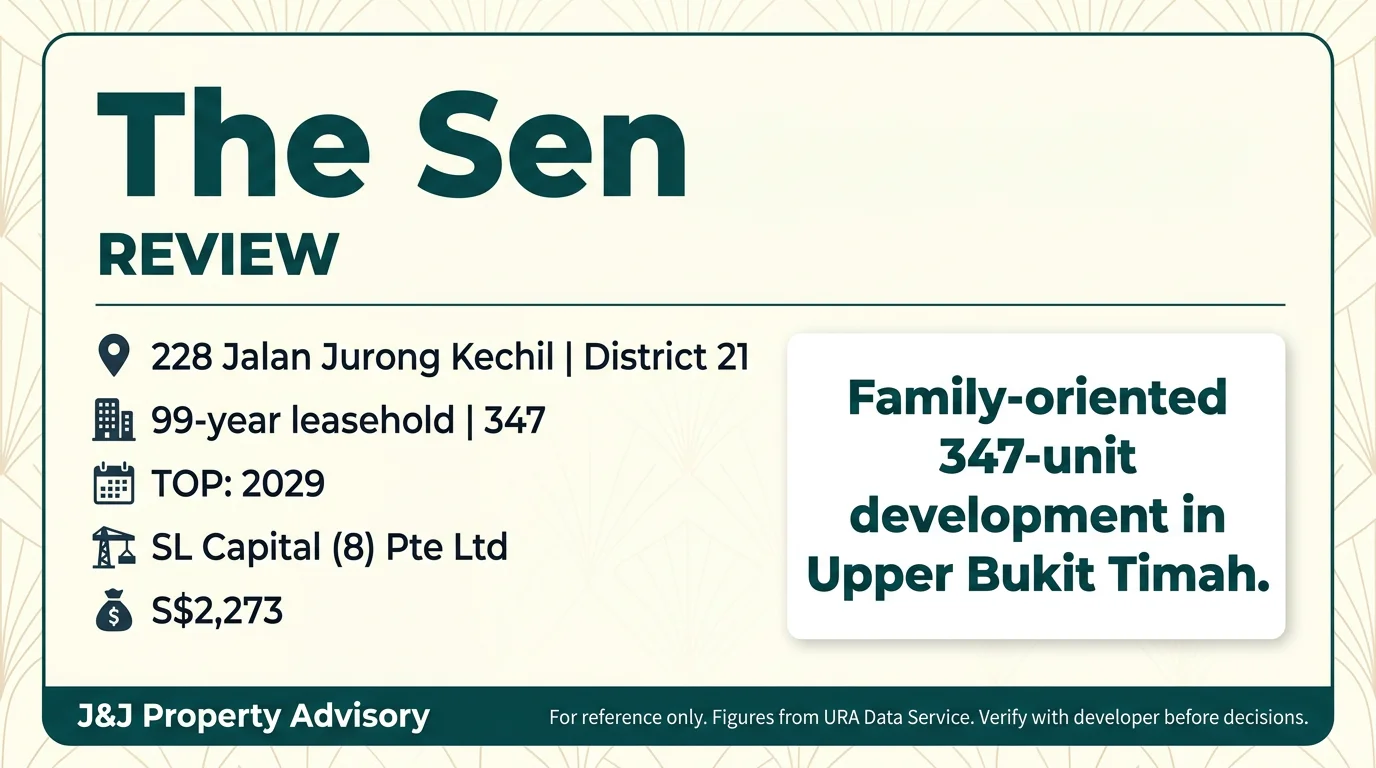

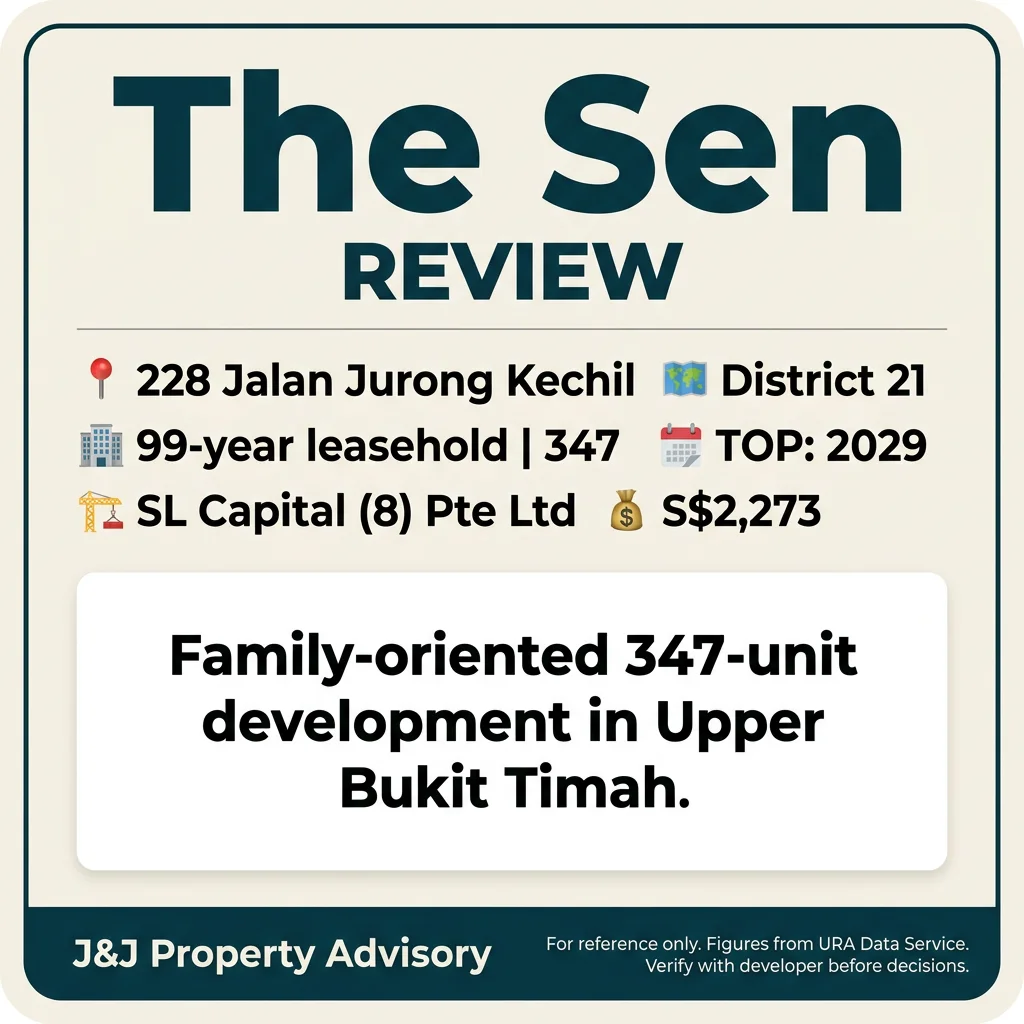

Project Snapshot

| Attribute | Details |

| Site Area | 207,155.6 sqft / 19,245.4 sqm |

| Developer | Sustained Land |

| Tenure | 99 Years Leasehold |

| Total Units | 347 |

| Units Sold | 112 / 347 (32%) |

| Units Remaining | 233 |

| Land Cost PSF PPR | S$841 |

| Launch Median PSF | S$2,273 (URA) |

| Architect | AGA Architects |

| Data as of | 26 Mar 2026 |

The Sen occupies a substantial 19,245 sqm site along Jalan Jurong Kechil, one of the larger land parcels released in District 21’s recent residential pipeline. At S$841 PSF PPR, the land cost positions this firmly in the mid-tier segment, allowing Sustained Land to price competitively while maintaining developer margins at 2.94x – well above the market norm of 2.27x. This cushion suggests potential pricing flexibility if sales velocity softens, though current take-up at 32% after four months indicates moderate rather than strong market reception.

Location & Connectivity

1. Hume MRT (DT4) serves as primary rail access approximately 790m away

The Downtown Line station requires a 10-minute walk, which sits at the outer edge of comfortable walking distance for daily commutes. The 790m distance means most residents will likely drive, cycle, or take feeder buses during peak periods. Direct Downtown Line access connects to Bugis (9 stops), Chinatown (12 stops), and the CBD core within 25-30 minutes.

2. Beauty World (DT5) provides secondary access approximately 1.05km away

The station anchors a more established commercial node with Beauty World Centre and Beauty World Plaza within 1.07-1.08km of the site. This represents a 13-15 minute walk, making it a realistic weekend option for dining and errands but less practical for daily commuting. The dual-station setup offers routing flexibility when Downtown Line experiences service disruptions.

3. Five primary schools cluster within 1-2km, led by Bukit Timah Primary at approximately 1.01km

Bukit Timah Primary sits just outside the 1km priority distance advantage but remains accessible for families willing to navigate Phase 2C balloting. Keming Primary (1.29km), Pei Hwa Presbyterian Primary (1.35km), Bukit View Primary (1.6km), and Lianhua Primary (1.73km) provide backup options with varying academic reputations. None of these schools guarantee admission within walking distance, which limits the education premium versus locations with sub-1km coverage.

4. Expressway connectivity relies on Pan Island Expressway (PIE) and Bukit Timah Expressway (BKE) access points

Upper Bukit Timah Road provides direct connections to PIE via Bukit Timah Road or Lornie Road exits, typically 5-7 minutes during off-peak periods. BKE access via Dairy Farm Road serves drivers heading north to Woodlands or Causeway. Peak hour congestion along Upper Bukit Timah Road remains a persistent issue, with morning westbound traffic frequently backing up from the PIE merge.

5. The Rail Mall (1.23km) and Bukit Timah Plaza (1.48km) anchor neighbourhood retail, with HillV2 at 1.81km

These malls cater primarily to daily needs rather than destination shopping or dining. Beauty World Centre serves wet market and hawker requirements, while The Rail Mall targets the weekend brunch crowd. Residents seeking department stores or cinema options will need to travel to Lot One (Choa Chu Kang), Junction 10, or Westgate in Jurong East.

6. Proximity to Bukit Timah Nature Reserve and Dairy Farm Nature Park positions the site for nature-focused lifestyle

The development sits roughly 2km from Bukit Timah Nature Reserve’s main entrance and similar distance to Dairy Farm Nature Park trails. This makes weekend hikes and trail runs genuinely accessible without requiring long drives. The green corridor appeal forms a core part of the project’s positioning, though daily exposure to nature remains limited compared to actual landed enclave addresses.

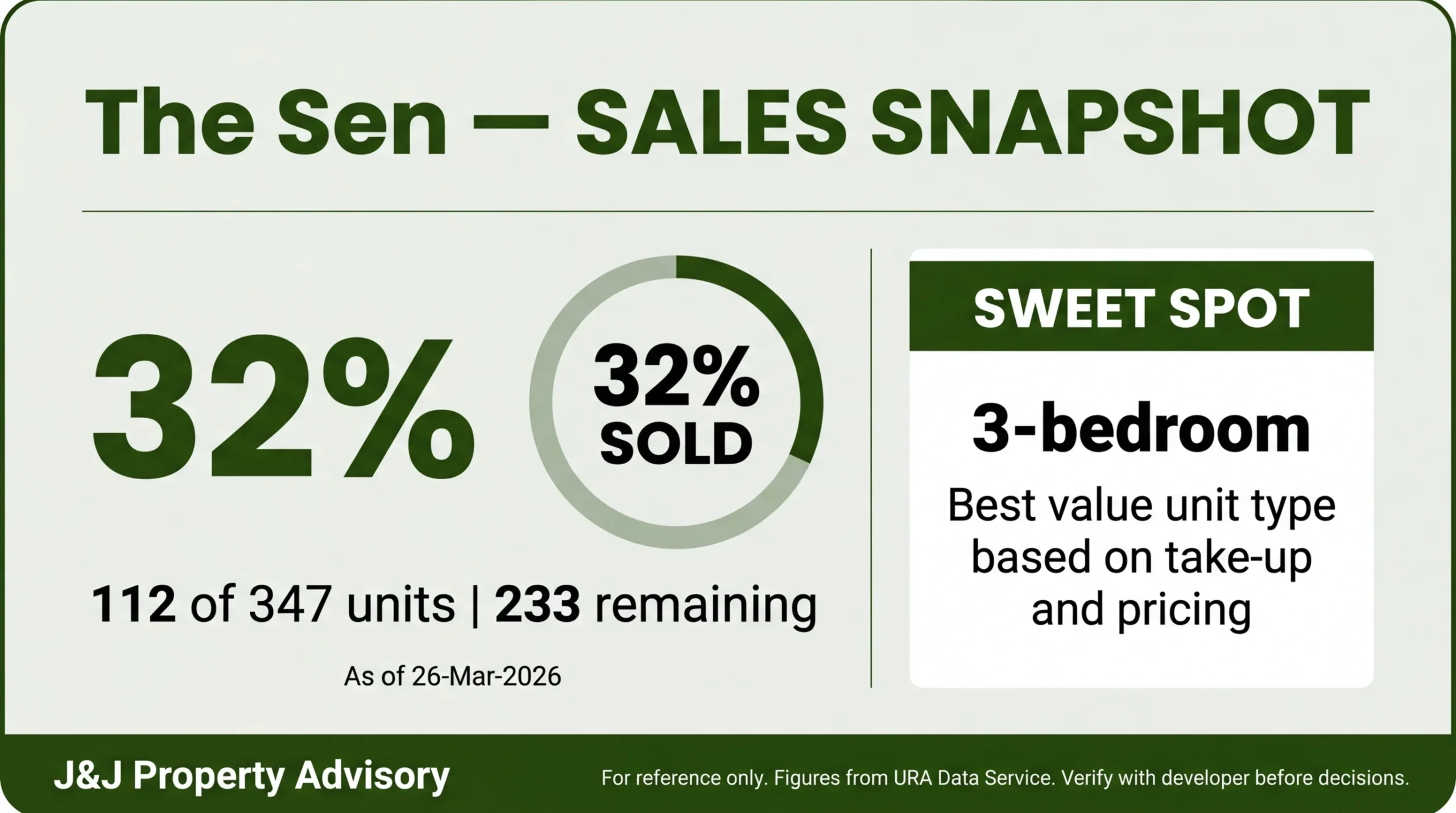

Sales Performance

The Sen has recorded 112 units sold from 347 launched as of 26 March 2026, achieving a 32% take-up rate approximately four months post-launch. URA developer sales data shows 86 units transacted across two quarters at a median PSF of S$2,273, with a range of S$2,220 to S$2,479. Monthly velocity averages 7.0 units, which trails the stronger launches in District 21 such as Nava Grove and Pinetree Hill during their initial quarters.

The URA median PSF of S$2,273 sits 3.3% below the District 21 condo median of S$2,350 over the past two years, reflecting the project’s positioning as a value-oriented option within the precinct. Developer asking prices start from S$2,476 PSF (based on quantum-to-size ratios), suggesting the bulk of early transactions occurred at discounts or on smaller-footprint units. The 32% take-up after four months signals moderate interest rather than urgent demand, likely hampered by the 790m MRT distance and school proximity gaps.

| Metric | Figure |

| Units Sold | 112 / 347 (32%) |

| URA Median PSF | S$2,273 |

| URA PSF Range | S$2,220 – S$2,479 |

| Monthly Velocity | 7.0 units/month |

| District Median PSF | S$2,350 |

HDB Upgrader Catchment

The Sen draws from substantial HDB upgrader pools in Bukit Batok and Bukit Timah, with 1,375 four-room flat transactions recording a median price of S$615k over the past 24 months. Four-room owners exiting at this median price typically extract S$350k-S$500k in equity after CPF refunds and accrued interest, which translates to purchasing power of approximately S$1.4-1.8M for a new launch unit when factoring in 25% down payment requirements and mortgage capacity.

Bukit Batok dominates the volume with 1,338 four-room transactions at S$612k median, while Bukit Timah’s smaller sample of 37 transactions commands a premium at S$850k median. Executive flat owners, representing 166 transactions at S$874k median, can potentially access S$600k-S$900k in equity, positioning them comfortably for three-bedroom or small four-bedroom units.

The developer’s two-bedroom pricing from S$1.515M creates a viable entry point for four-room upgraders with S$400k+ equity and stable dual incomes. However, the three-bedroom range starting at S$1.956M requires executive flat equity or five-room upgrader profiles to meet Total Debt Servicing Ratio requirements comfortably. The project’s 790m distance from Hume MRT represents a noticeable step-down from BTOs with 400m station access, which may deter upgraders prioritising public transport convenience.

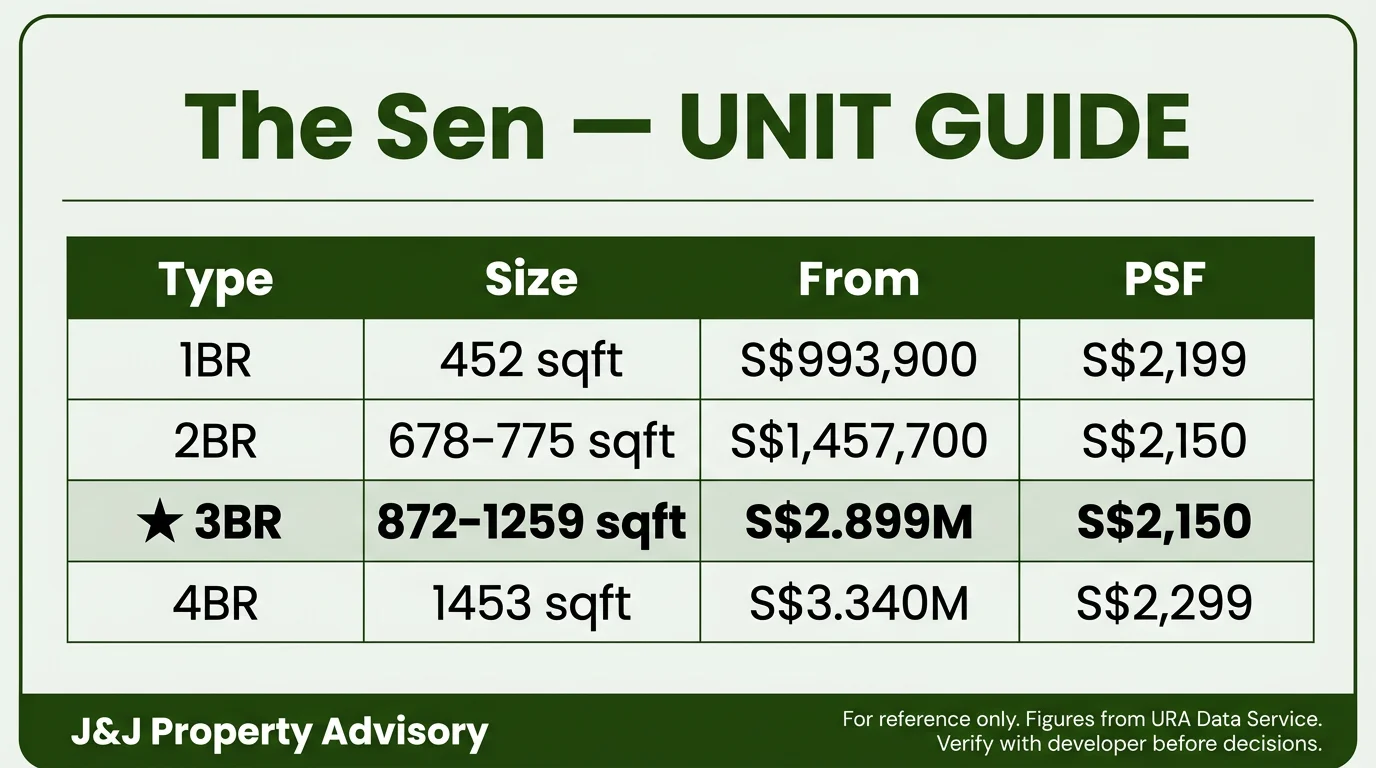

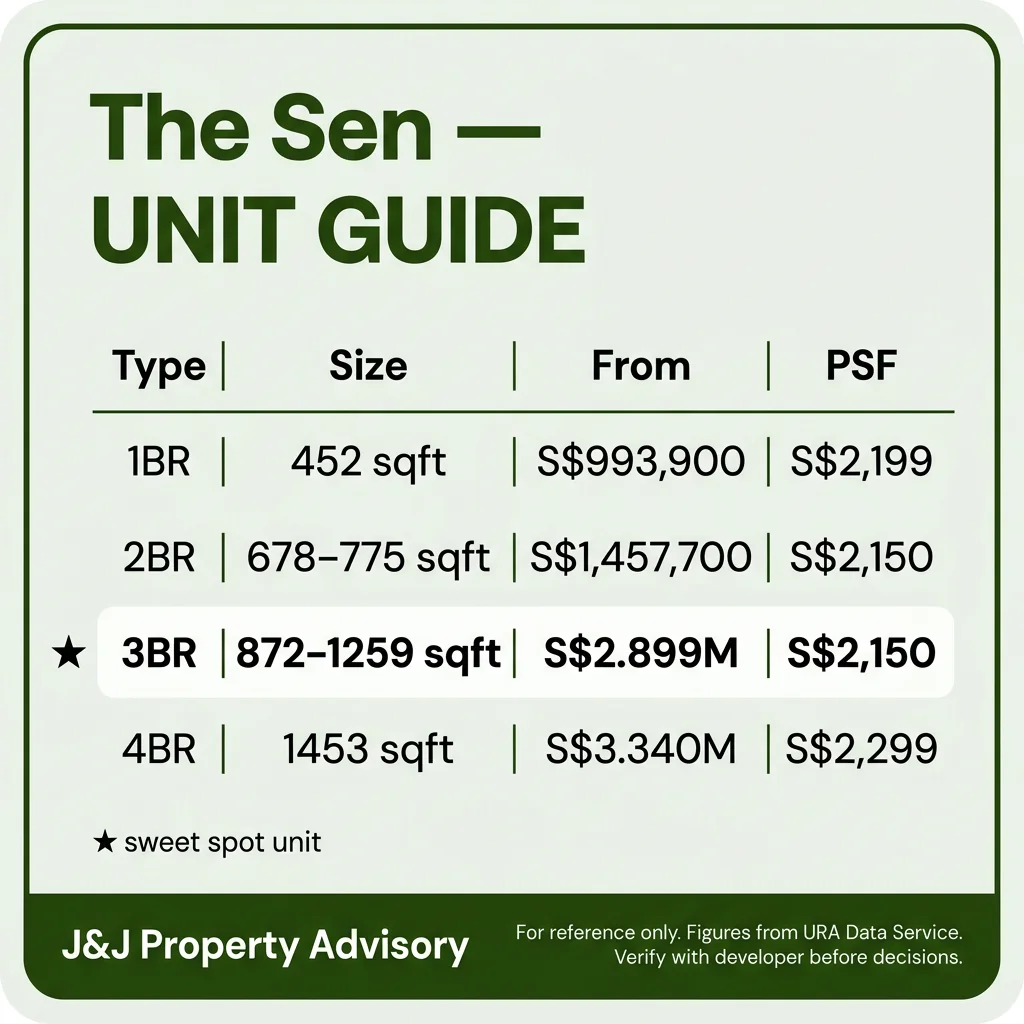

Unit Mix & Pricing

| Type | Size Range (sqft) | Quantum From | PSF From |

| 2 Bedroom | 678 – 775 | S$1.515M | S$2,481 |

| 3 Bedroom | 872 – 1,259 | S$1.956M | S$2,471 |

| 4 Bedroom | 1,453 | S$3.341M | S$2,482 |

The Sen allocated approximately 50% of its 347 units to one-bedroom and two-bedroom formats, creating significant exposure to the investor and small household segment. The two-bedroom range from 678-775 sqft offers functional layouts with the S$1.515M entry quantum targeting HDB upgraders and first-time private market buyers. Three-bedroom units span an unusually wide 872-1,259 sqft range, suggesting the developer created distinct compact and premium tiers within the same bedroom count.

The four-bedroom units at 1,453 sqft command S$3.341M, which prices them into competition with resale landed terrace houses in outer districts. The consistent S$2,471-S$2,482 PSF across bedroom types indicates the developer avoided significant quantum discounting on larger units, maintaining pricing discipline that benefits early buyers but may slow absorption velocity.

The heavy weighting toward smaller units creates built-in supply risk when these owners eventually exit in 5-10 years, as they will compete against a large pool of similar-sized units within the same development and neighbouring projects. Buyers targeting long-term own-stay should favour the three-bedroom and four-bedroom formats that face thinner competition and attract family upgraders rather than pure investors.

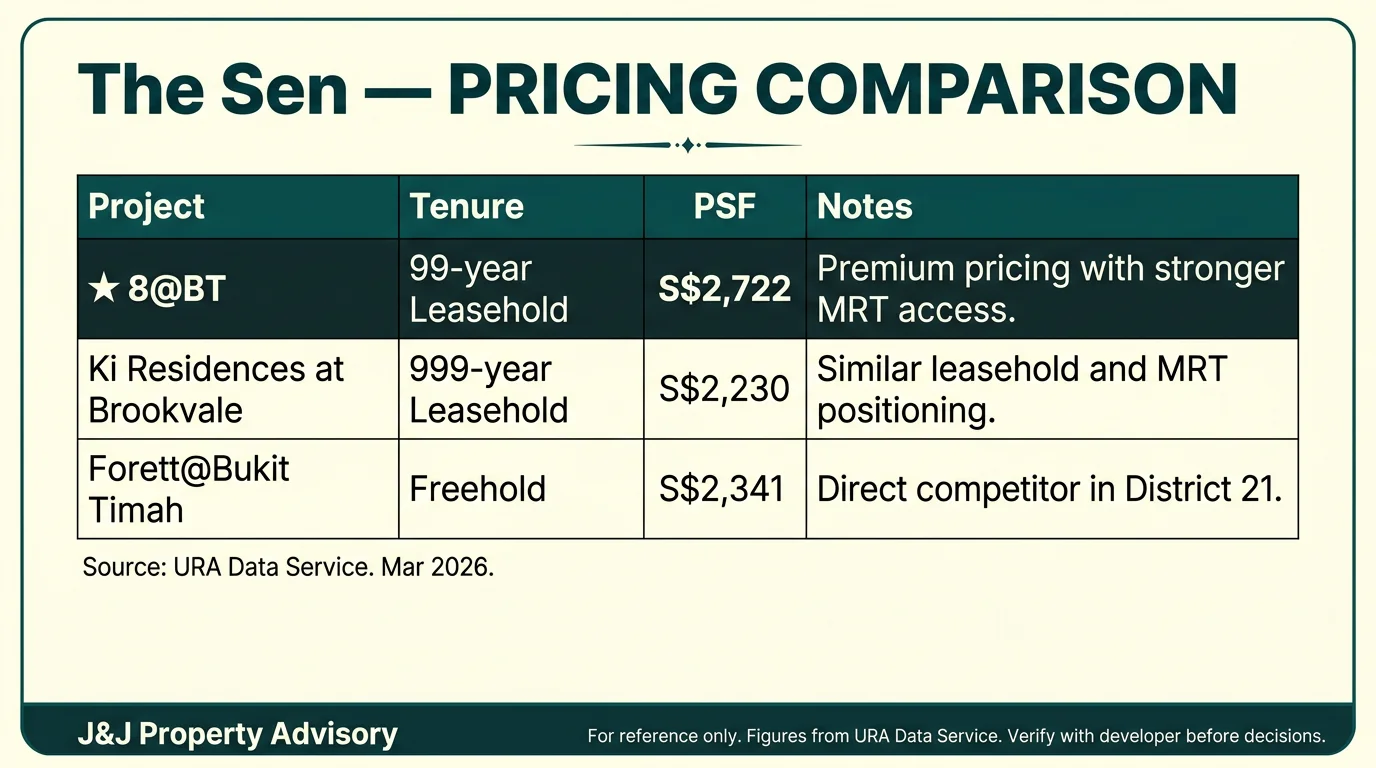

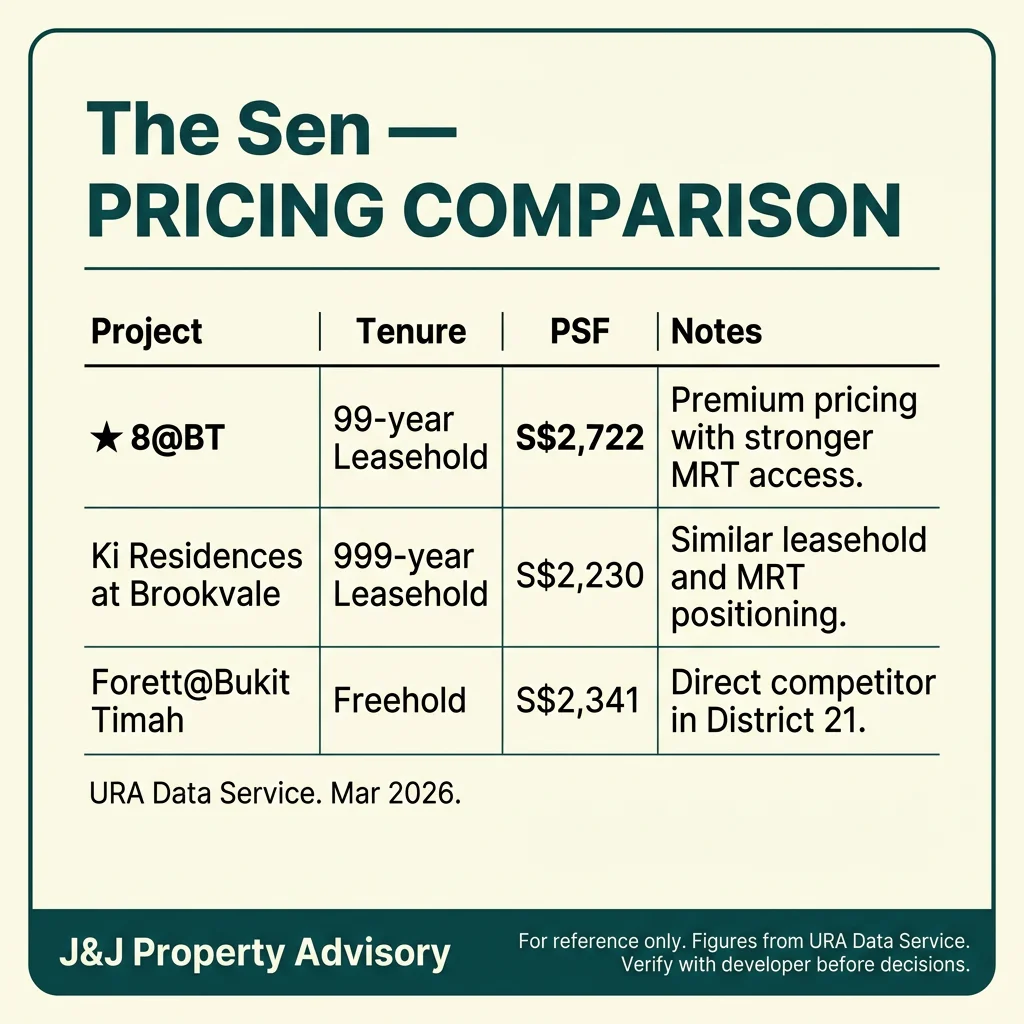

Comparables

| Project | Median PSF | PSF Range | Transactions | Tenure |

| 8@BT | S$2,727 | S$2,527 – S$3,033 | 101 | 99-year leasehold |

| Nava Grove | S$2,478 | S$2,209 – S$2,771 | 529 | 99-year leasehold |

| Pinetree Hill | S$2,548 | S$2,139 – S$2,763 | 310 | 99-year leasehold |

| Ki Residences at Brookvale | S$2,242 | S$1,869 – S$2,392 | 70 | 99-year leasehold |

The Sen’s median PSF of S$2,273 undercuts all major recent launches except Ki Residences at Brookvale, which sits closer to Hillview MRT (DT3) and traded at S$2,242 median across 70 transactions. The S$454 PSF gap versus 8@BT reflects both location quality differences and 8@BT’s positioning as a boutique 109-unit development that commands scarcity premiums. Nava Grove at S$2,478 median provides the closest comparable with 529 transactions indicating strong market validation, though its Cashew MRT proximity offers superior public transport access.

The Sen slots into the value tier alongside Ki Residences, competing primarily on quantum accessibility rather than location superiority. Buyers comparing these projects should weigh The Sen’s larger site area and more comprehensive facilities against Ki Residences’ closer MRT access at Hillview.

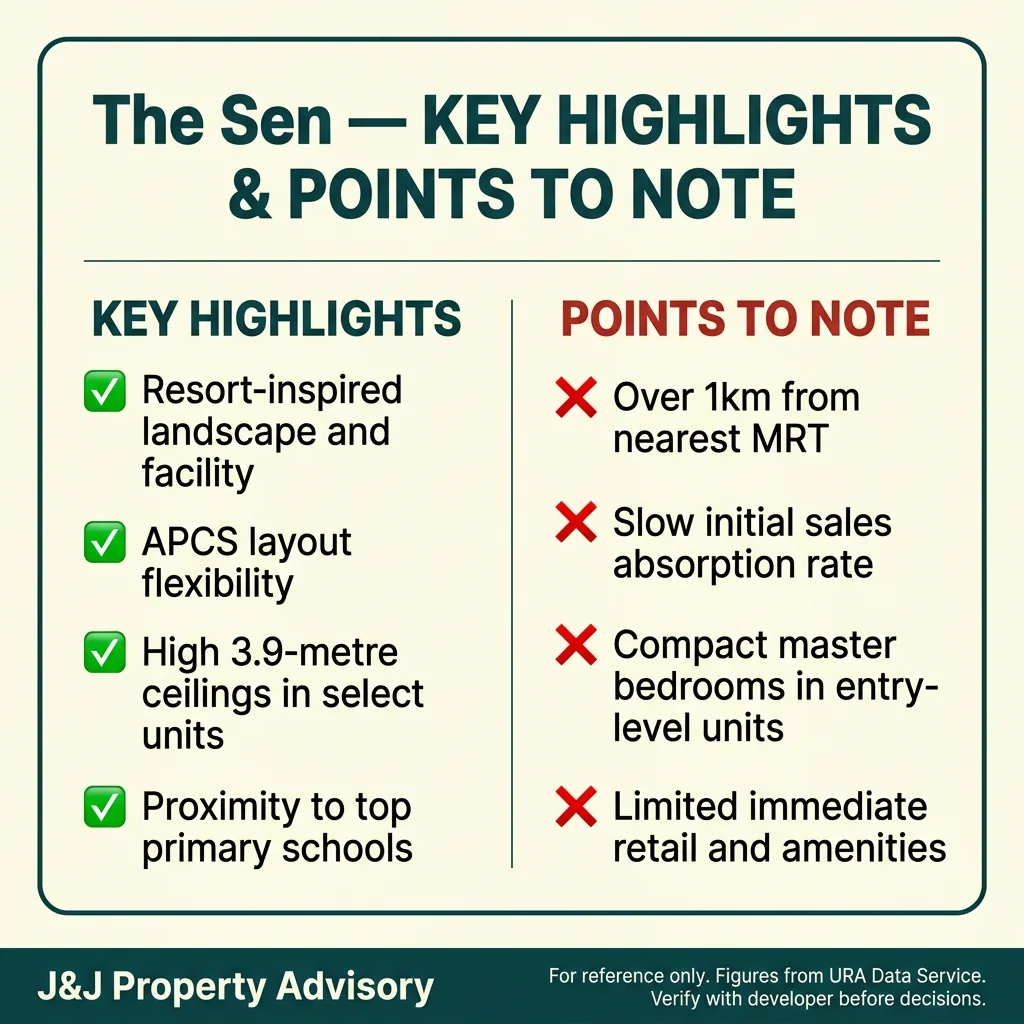

Key Strengths

Competitive pricing relative to District 21 new launch benchmarks creates margin of safety

The S$2,273 median PSF sits 3.1% below the District 21 two-year transaction median of S$2,346, giving buyers a modest entry discount versus established resale stock. The land cost of S$841 PSF PPR provides the developer with healthy margins that reduce pressure for future price increases, though this also signals limited upside leverage compared to sites acquired at S$1,000+ PSF PPR that force developers to push market pricing.

Substantial site area of 19,245.4 sqm supports genuine resort-style facilities across multiple levels

The project incorporates a 50-metre lap pool, family pool, aqua gym, hot and cold soaking baths, yoga decks, and sky lounge across a proper land area that allows for spatial separation. This contrasts sharply with compact urban sites where facilities exist primarily for marketing brochure appeal rather than practical daily use. The inclusion of an on-site childcare centre adds tangible convenience for dual-income families with young children.

Design execution received positive feedback for practical layouts with high ceilings and bathroom windows

Independent reviews highlighted functional space planning with open-concept living areas, high ceilings that enhance spatial perception, and the inclusion of windows in bathrooms that improve ventilation and natural light. Larger units offer park views and ensuite access, though specific view corridors depend heavily on unit stack and orientation. These design choices should age well compared to trend-driven aesthetics that date quickly.

BCA Green Mark Platinum and Super Low Energy certification delivers measurable operating cost benefits

Solar-powered common area features and enhanced natural ventilation strategies reduce maintenance fees over the building lifecycle. While these certifications serve marketing purposes, they translate to real utility cost savings and improved thermal comfort in common areas. Singapore’s increasingly aggressive green building mandates make these features table stakes rather than differentiators, but early adoption positions the project well versus older stock.

Nature corridor proximity to Bukit Timah Nature Reserve and Dairy Farm Nature Park supports lifestyle positioning

The approximately 2km distance to both major nature reserves makes weekend outdoor activities genuinely accessible without requiring 20-30 minute drives. Trail running, hiking, and mountain biking communities gravitate to this corridor, creating an established lifestyle ecosystem. This matters primarily for own-stay buyers who will use these amenities regularly rather than investors focused purely on rental yield metrics.

Points to Watch

MRT distance at 790m reduces rental appeal and investor liquidity

The 790m walk to Hume MRT places this outside the 400-500m radius where tenants and future buyers apply convenience premiums. Rental yields in District 21 typically range 3.5 – 4.5% for established projects; new launches incur a 0.4% haircut due to pricing premiums, putting The Sen’s realistic gross yield at 3.1-4.1%. Investors banking on strong rental demand should model conservatively, as tenants prioritise MRT proximity when comparing similar-priced units across the district.

School proximity just misses 1km cutoff for distance priority

Bukit Timah Primary School sits 1,010m away – 10 metres beyond the Phase 2B threshold that would have provided distance-based enrolment priority. This marginal miss is material for families treating school access as a primary buying driver, as Phase 2C admission depends on available slots after closer households are allocated. The next four schools fall between 1.29km and 1.73km, all within Phase 2C only. Families should verify current MOE balloting outcomes for these schools before assuming enrolment certainty.

August 2030 TOP timeline extends opportunity cost and market risk

The 4.3-year wait from March 2026 to August 2030 exposes buyers to extended opportunity cost on capital and heightened market cycle risk. Buyers committing S$383k (25% of a S$1.53M 2-bedroom) today will see that capital locked until 2030, during which rental yields and resale comparables may shift. Projects with 2027-2028 TOPs offer faster liquidity and shorter exposure to construction delays or market downturns.

Sales velocity at 7.0 units/month trails stronger District 21 launches

Monthly absorption of 7.0 units over the first two quarters indicates moderate rather than strong demand. Nava Grove and Pinetree Hill recorded double-digit monthly velocities during comparable launch windows, suggesting The Sen’s combination of MRT distance, school gaps, and later TOP has dampened urgency. Slower sales may benefit later buyers through developer incentives, but it also signals weaker resale momentum when current buyers eventually exit.

Heavy 2-bedroom concentration creates future resale competition

With 167 units (50% of inventory) in the 2-bedroom format, future resale markets will see concentrated supply within a narrow buyer segment. When multiple owners exit simultaneously – common around the 3-5 year post-TOP window – pricing power shifts to buyers as competing listings flood the market. Projects with more balanced unit mixes distribute resale pressure across investor, upgrader, and family cohorts.

Phase 2C school access limits premium pricing on family resale

The lack of Phase 2B school proximity constrains the pricing premium achievable on family-focused resale compared to projects within 1km of popular primaries. Buyers banking on school-driven appreciation should adjust expectations, as families willing to pay top dollar for enrolment certainty will gravitate toward true 1km-radius projects. This factor particularly affects 3-bedroom and 4-bedroom resale values, where school access often justifies 8-12% premiums in comparable estates.

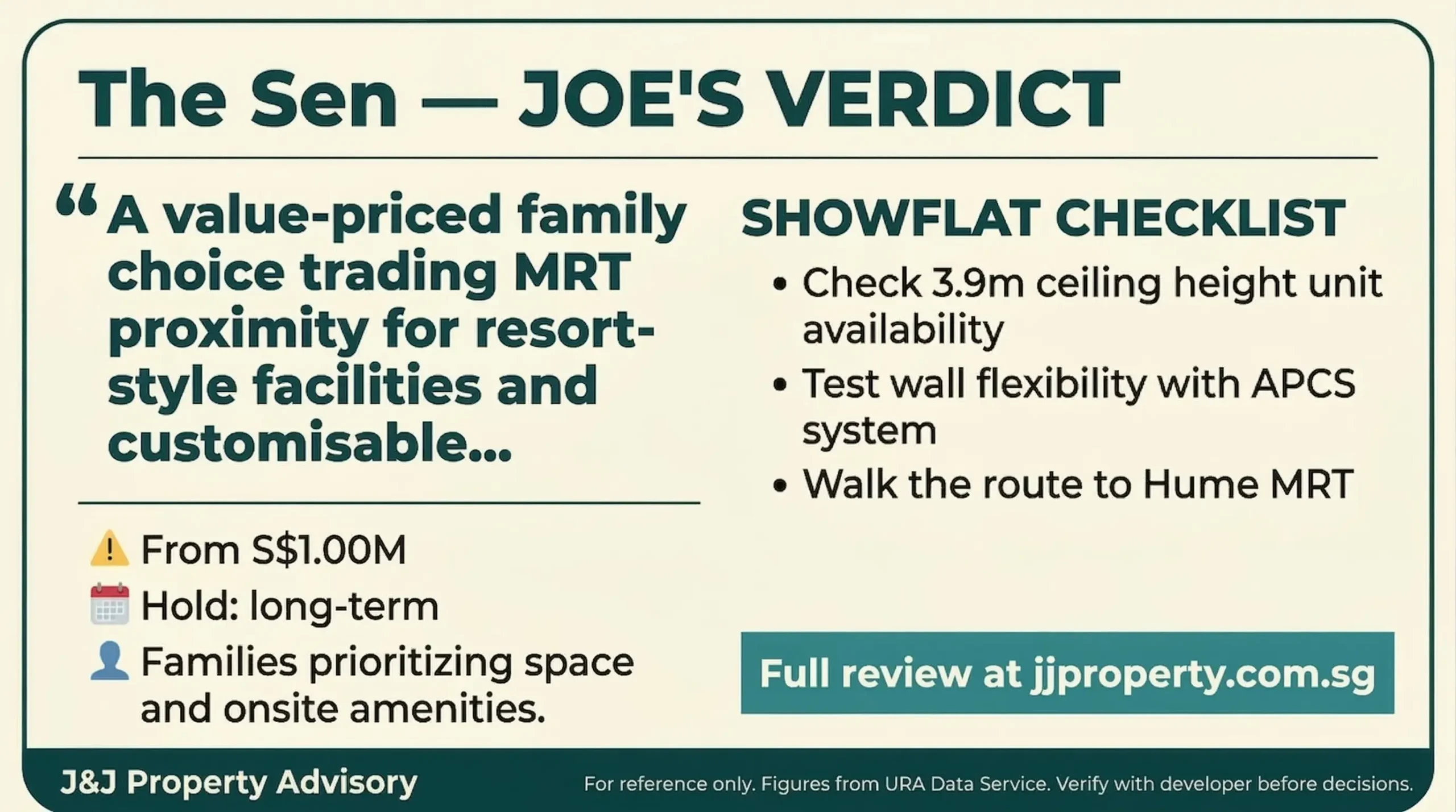

Bottom Line

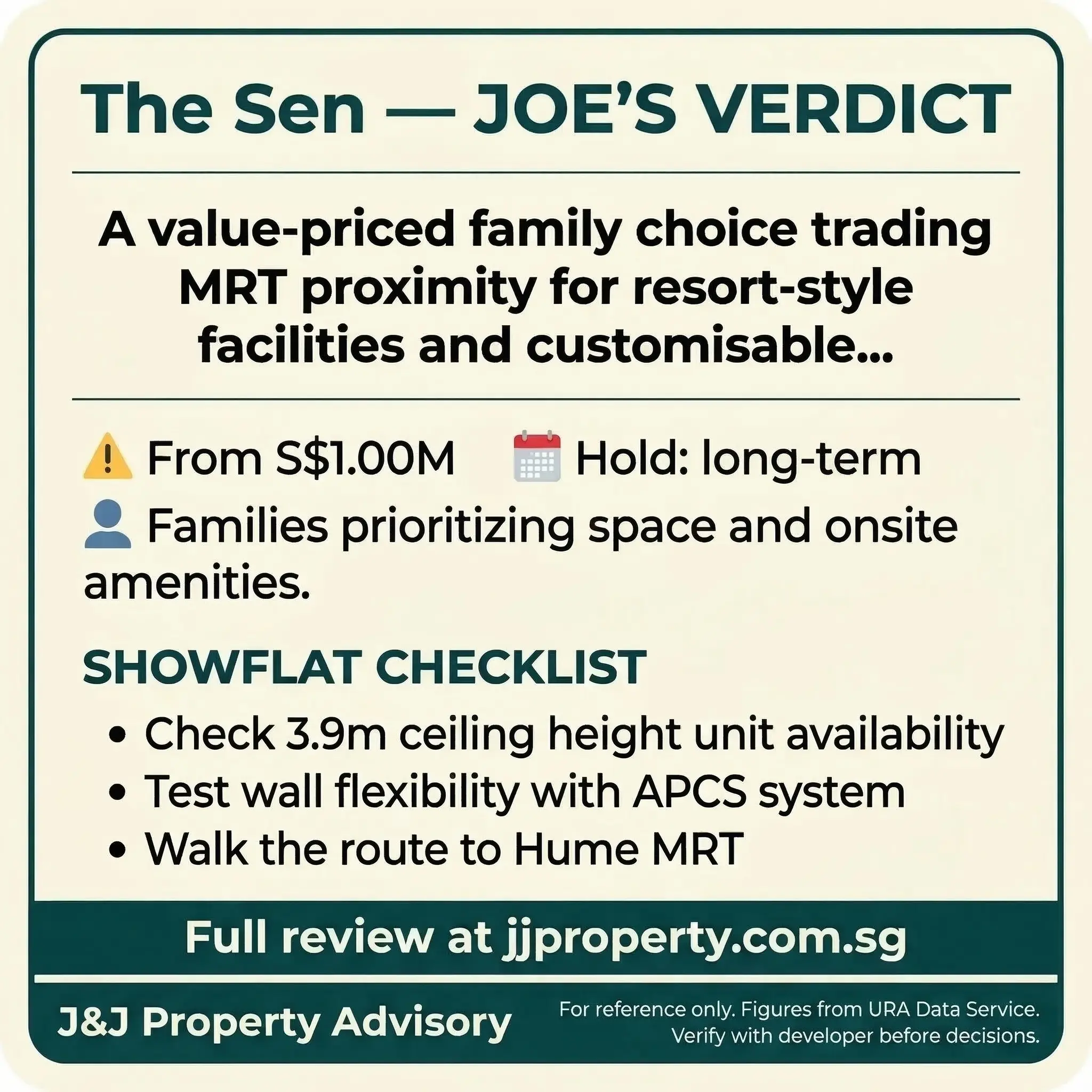

The Sen offers a tangible value equation for buyers prioritising space efficiency and entry quantum over location premiumisation. The S$2,273 median PSF sits 3.3% below District 21 norms, while the 3-bedroom layouts from 872 to 1,259 sqft deliver liveable space uncommon at this price tier. The land cost cushion at 2.94x provides pricing flexibility, reducing downside risk if the developer adjusts incentives to accelerate absorption. For own-stay buyers willing to accept a 790m MRT walk and Phase 2C school access, the lifestyle trade-offs are clear and the quantum structure remains competitive.

The project’s weaknesses—MRT distance, school proximity gaps, and August 2030 TOP—are structural rather than speculative. Investors should model rental yields conservatively in the 3.1 – 4.1% range and recognise that tenant demand tilts toward MRT-adjacent alternatives. The 32% take-up after four months reflects measured rather than urgent demand, suggesting pricing may soften modestly as the developer balances sales velocity against margin targets. Buyers entering today should prioritise layouts over units, focus on the upper-range 3-bedroom formats where space efficiency is strongest, and verify construction progress milestones as TOP approaches.

For Own-Stay Buyers

Families seeking space-efficient layouts in a nature-adjacent enclave will find alignment here, provided MRT dependence is low and school enrolment is not a binding constraint. The 3-bedroom units from 872 to 1,259 sqft deliver genuine layout diversity, with the upper range approaching executive condo standards. Dual-income households with car ownership will extract the most value, leveraging expressway access for varied work locations. Verify developer track record on TOP delivery, as the August 2030 timeline leaves minimal buffer for delays.

For Investment Buyers

Rental yields will compress toward 3.1-3.5% gross given the MRT distance and new launch pricing premium, making this a hold-to-appreciate rather than yield-focused play. The 2-bedroom units from S$1.53M offer the most liquid resale profile for upgrader demand, though the 50% inventory concentration will intensify future competition. Investors with 7-10 year hold horizons may benefit from Beauty World precinct rejuvenation and Rail Corridor infrastructure maturation, but near-term rental comps will favour projects closer to Hume or Beauty World MRT stations.

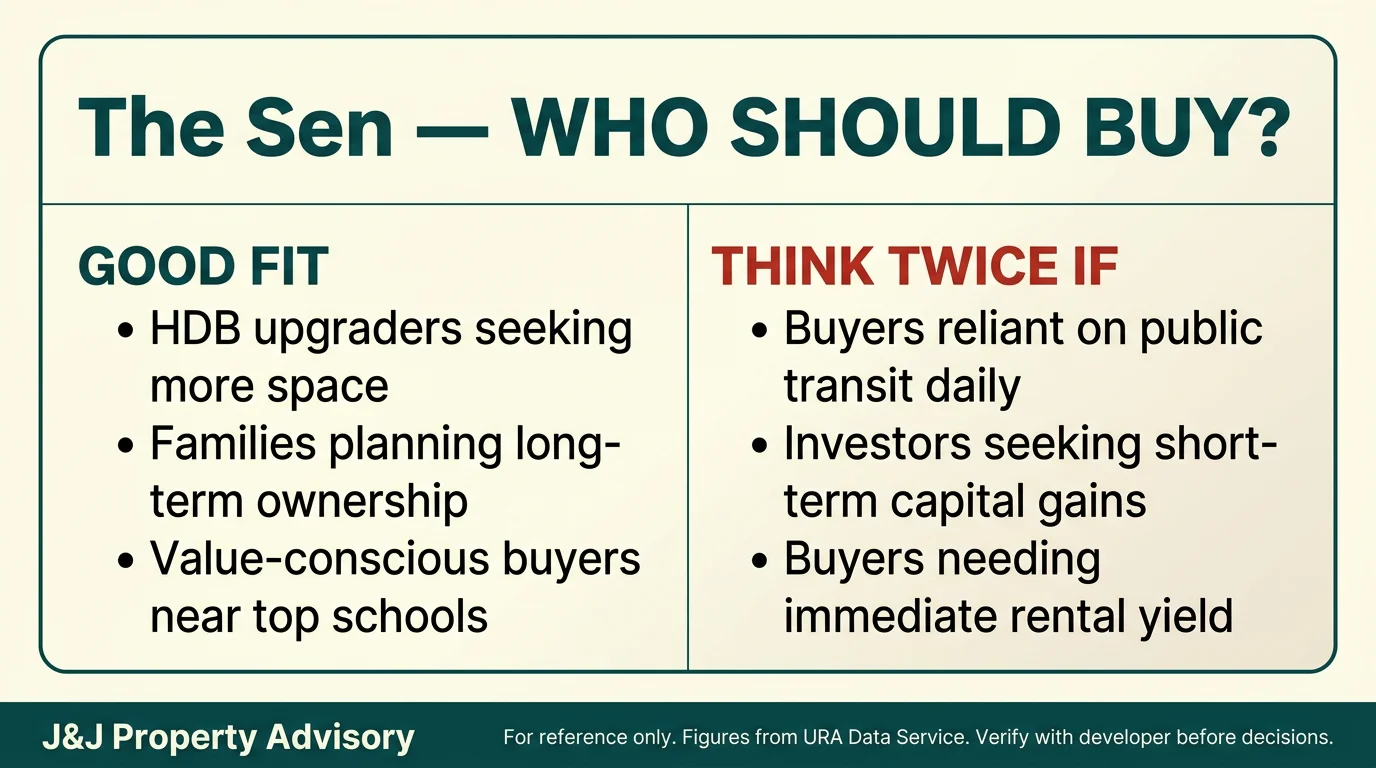

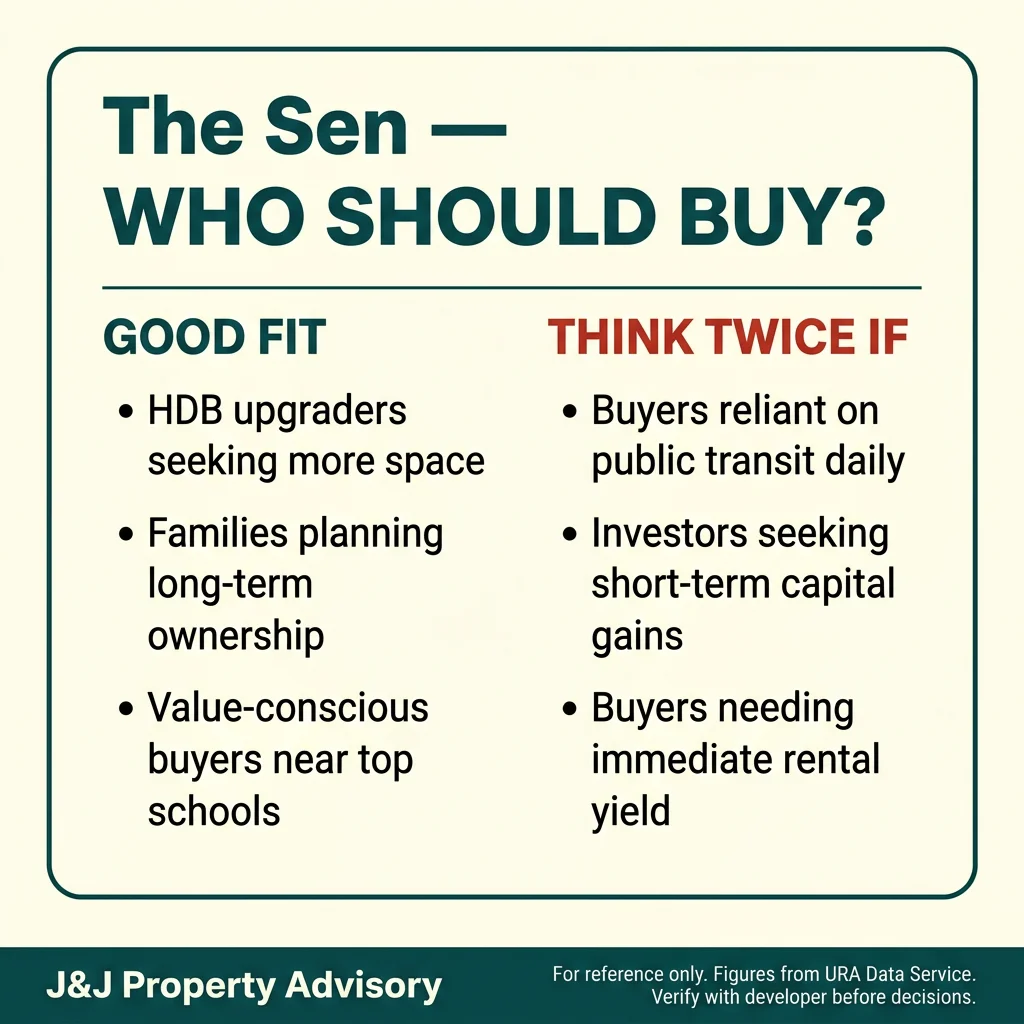

Who Is This For

Good fit:

- HDB upgraders from Bukit Batok 4-room flats with S$350k-S$500k equity seeking 2-bedroom entry quantums below S$1.6M

- Dual-income families prioritising liveable space (872-1,259 sqft 3-bedrooms) over MRT adjacency and willing to drive for daily commutes

- Car-dependent households with work locations across PIE-accessible zones (Jurong, CBD, Changi) valuing expressway connectivity over train reliance

- Outdoor-oriented buyers seeking Rail Corridor and Bukit Timah Nature Reserve access within 1-2km for weekend recreation

- Investors with 7-10 year hold horizons willing to absorb 3.1-3.5% gross yields in exchange for potential precinct appreciation as Beauty World rejuvenates

- Buyers prioritising developer pricing flexibility (2.94x land cost margin) over immediate sales momentum, anticipating potential incentives if absorption slows

Not ideal for:

- Families requiring Phase 2B school enrolment priority within 1km (Bukit Timah Primary sits 1,010m, just outside cutoff)

- MRT-dependent professionals prioritising sub-400m station proximity for daily CBD commutes (Hume at 790m exceeds tenant and investor preference thresholds)

- Investors targeting 4.5%+ gross rental yields common in mature MRT-adjacent estates (new launch premium and location compress yields to 3.1-4.1%)

- Buyers seeking rapid resale liquidity within 3-5 years post-TOP (heavy 2-bedroom concentration at 50% inventory will intensify resale competition)

- Households requiring TOP delivery before 2029 (August 2030 timeline extends opportunity cost and market exposure compared to 2027-2028 alternatives)

- Families banking on school proximity as a primary value driver (all five nearest primaries fall into Phase 2C only, limiting enrolment certainty and resale premiums)

Review Date: March 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This review is based on publicly available data and official URA transaction records. It is not financial advice. Verify all details with the developer before making purchase decisions.