Launched Analysis

Project Snapshot

| Attribute | Details |

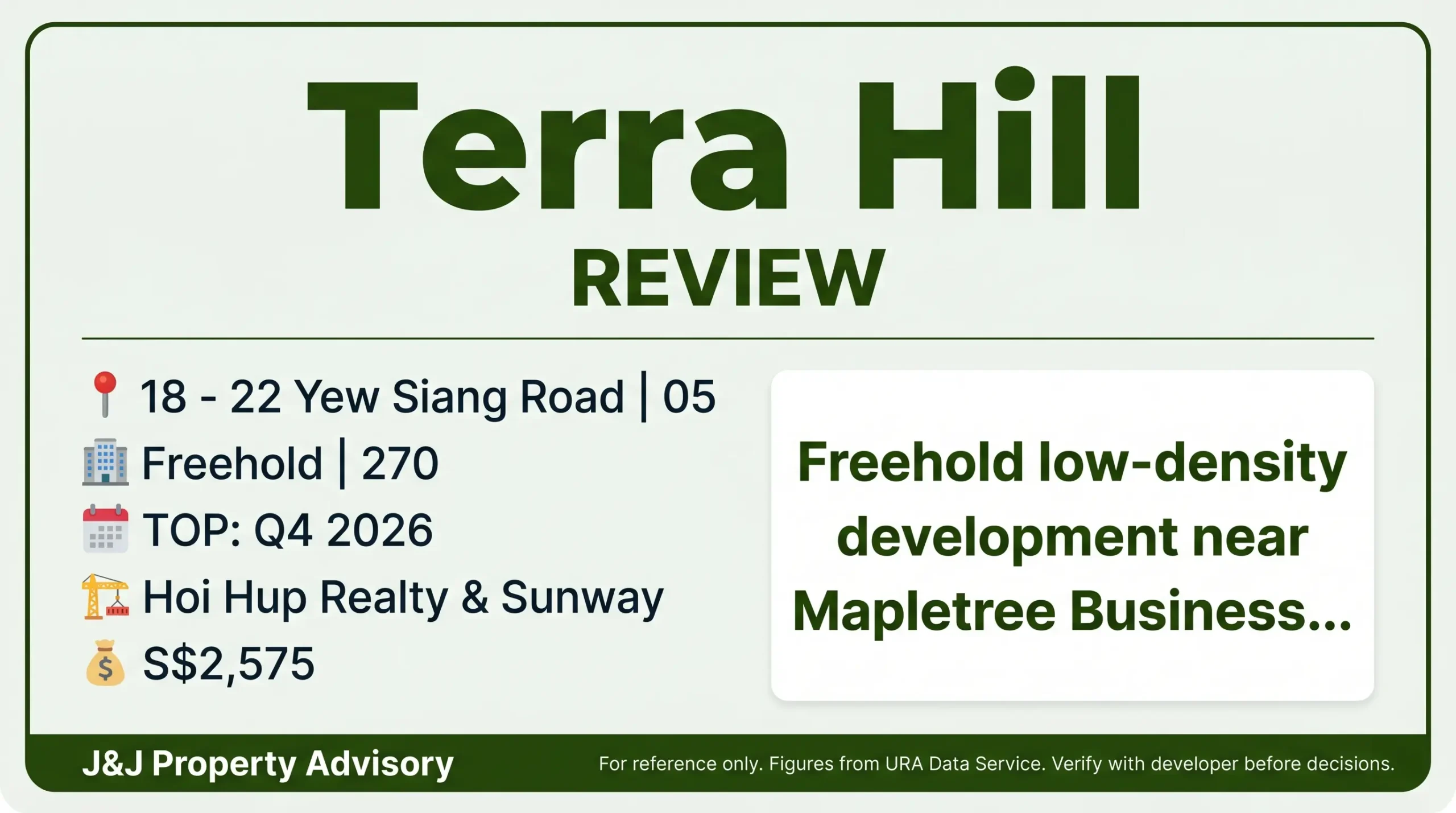

| Site Area | 208,443 sqft / 19,365 sqm |

| Developer | Hoi Hup Realty & Sunway |

| Tenure | Freehold |

| Total Units | 270 |

| Launch Date | 25 Feb 2023 |

| Expected TOP | Q4 2026 |

| Architect | P&T Consultants |

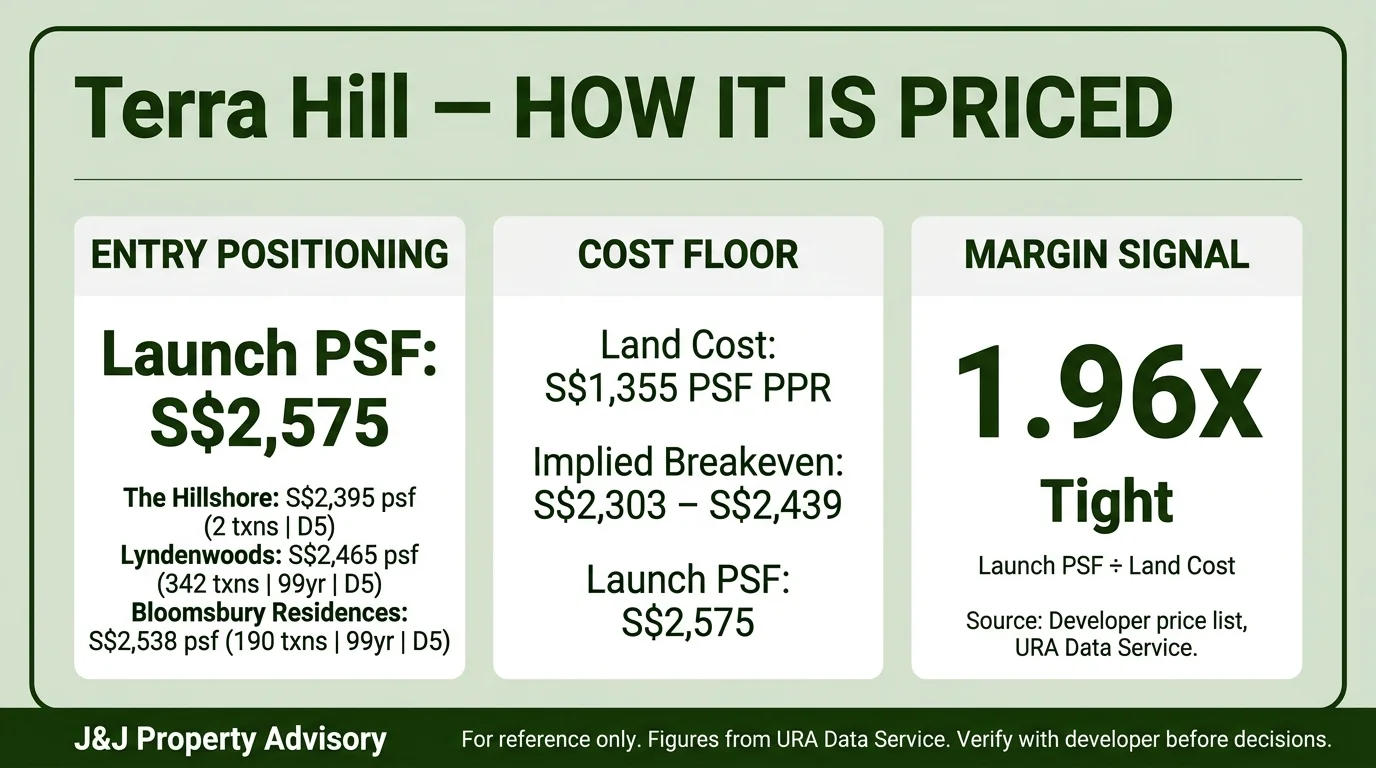

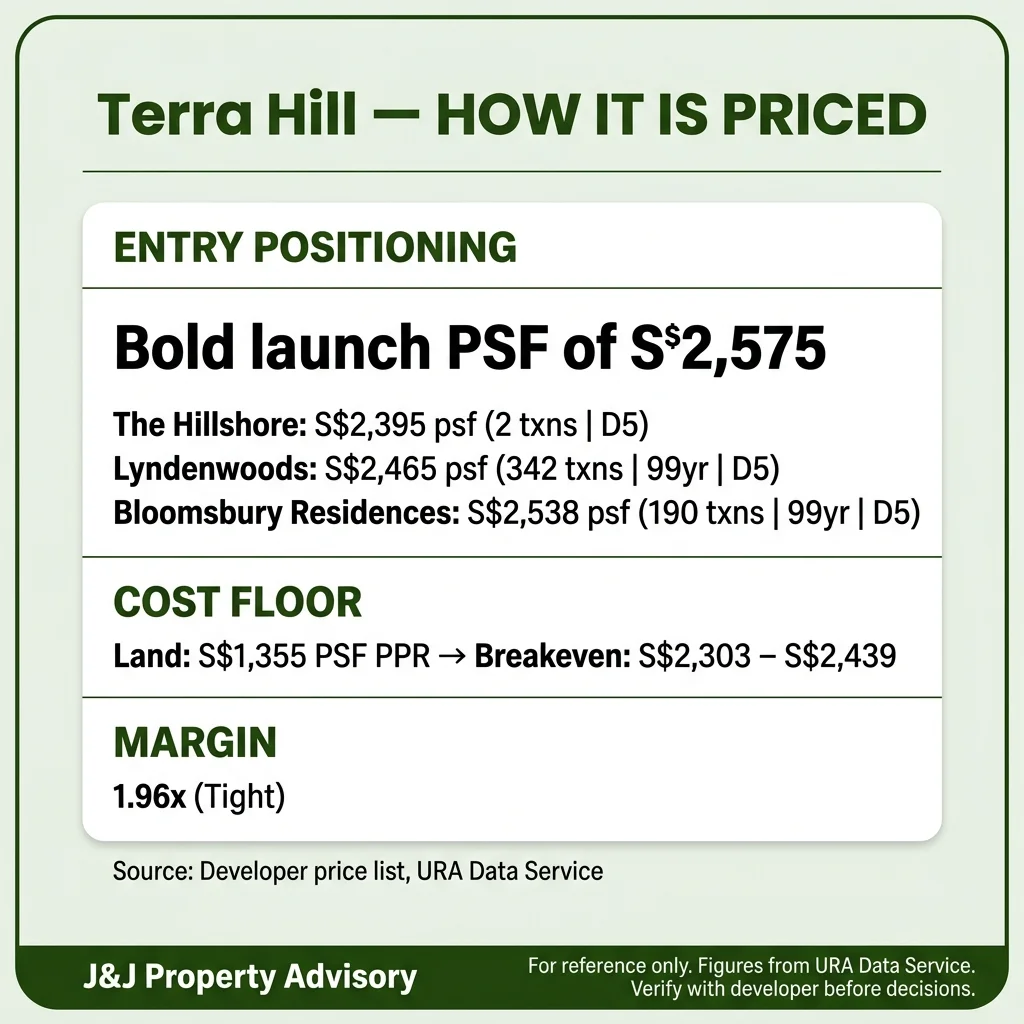

| Land Cost PSF PPR | S$1,355 |

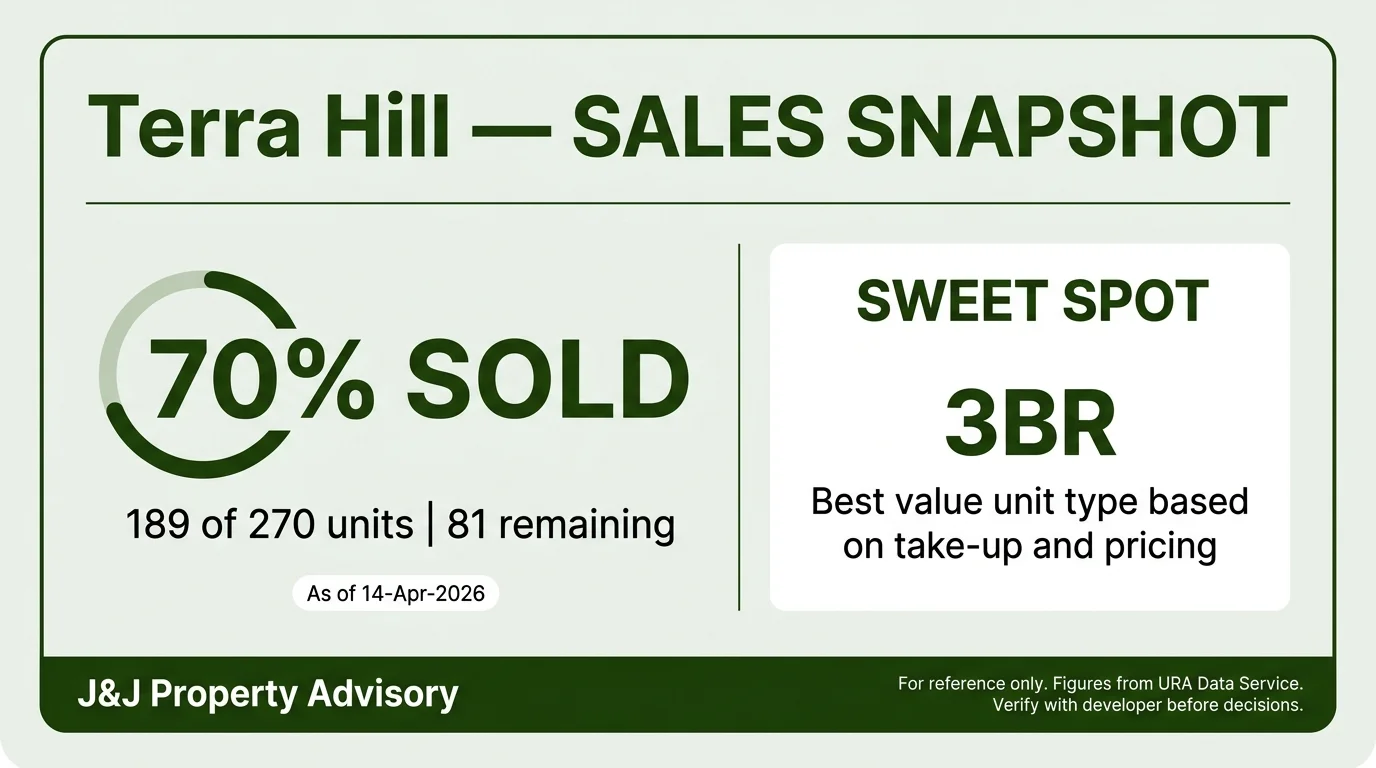

| Units Sold | 189 / 270 (70%) |

| Units Remaining | 81 |

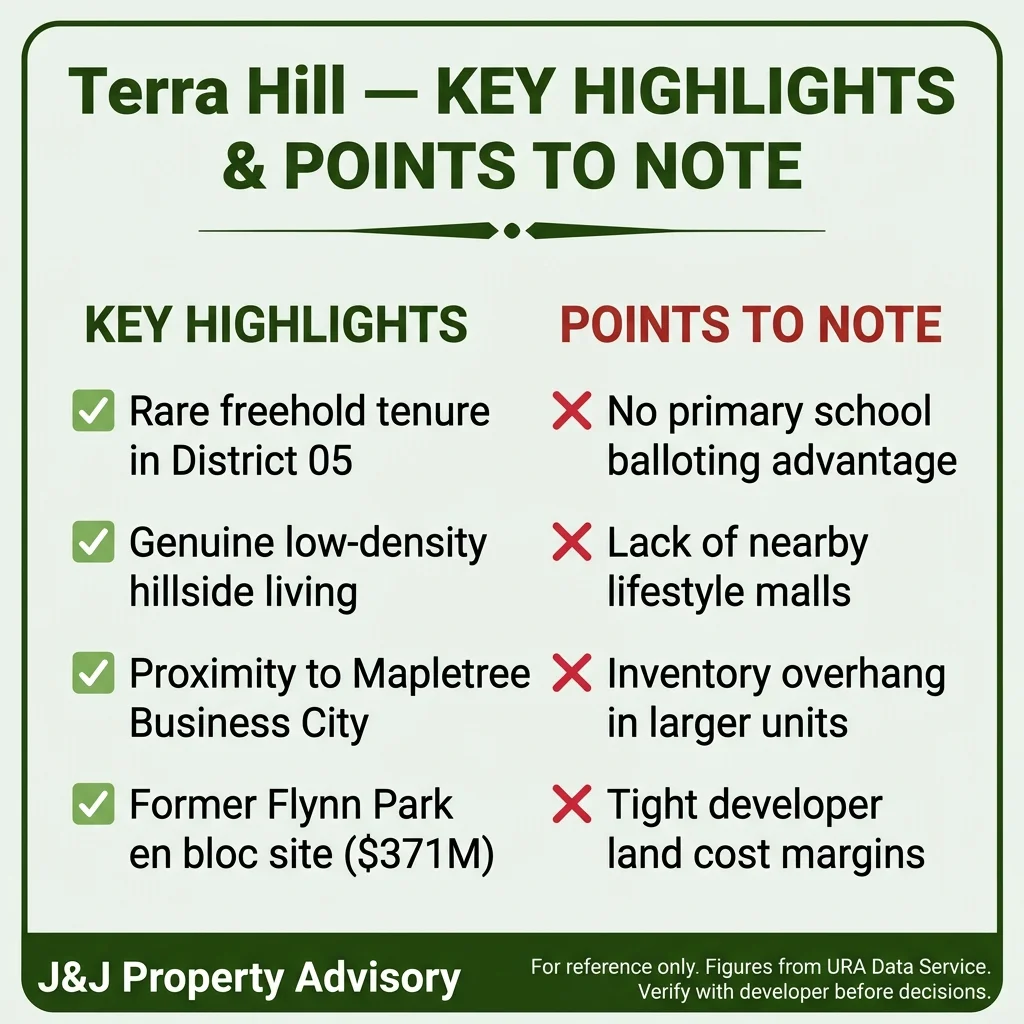

Terra Hill sits on a 19,365 sqm plot along Yew Siang Road, formerly the site of Flynn Park, which was acquired via collective sale for S$371 million in September 2021 by Hoi Hup-Sunway at S$1,355 PSF PPR. It is one of the few new freehold launches in District 05’s supply-constrained Pasir Panjang pocket. The site’s low-density configuration – 270 units across substantial acreage – positions it as a lifestyle-oriented alternative to the denser leasehold projects dominating the Rest of Central Region.

Location & Connectivity

1. Pasir Panjang MRT (CC26) – 330m

The Circle Line station is approximately 330m from the development, translating to a genuine 4-minute walk. This connectivity feeds directly into one-seat rides to Holland Village (CC21), Botanic Gardens (CC19), and Dhoby Ghaut (CC1/NE6/NS24) for CBD interchange. Pasir Panjang’s relatively quiet ridership profile also means less crowding during peak hours compared to major interchanges.

2. Labrador Park MRT (CC27) and Haw Par Villa MRT (CC25)

Labrador Park (CC27) sits approximately 1.24km southeast, while Haw Par Villa (CC25) is approximately 1.37km northwest. Both stations provide redundancy for Circle Line access, though neither is within comfortable walking range. Kent Ridge MRT (CC24) at approximately 1.94km serves National University of Singapore and the adjacent science park clusters, but requires transport from Terra Hill.

3. Major Employment Hubs – Mapletree Business City 740m

Mapletree Business City, one of Singapore’s largest business parks, is approximately 740m away. This cluster houses major tenants including Google, Barclays, and AIA, creating strong rental demand from expatriate executives and regional professionals. The proximity supports both owner-occupier commutes and investment rental positioning. Alexandra Precinct and Queenstown office nodes are also within 2km.

4. Expressway Access – West Coast Highway and AYE

West Coast Highway provides arterial access to the Ayer Rajah Expressway (AYE) within 2km. This routing connects to Jurong Lake District (15-20 minutes off-peak), Tuas industrial zones, and the upcoming Tuas Megaport. City-bound routes via AYE feed into the CBD and Marina Bay within 12-15 minutes under light traffic. The upcoming Greater Southern Waterfront redevelopment will reshape traffic patterns here over the next decade.

5. Schools – Blangah Rise Primary 1.72km

Blangah Rise Primary School sits approximately 1.72km away, placing Terra Hill within the Phase 2C distance band (1-2km). This eliminates eligibility for Phase 2B (within 1km), a meaningful constraint for families banking on proximity-based primary school balloting. No other primary schools fall within the 2km radius. Secondary school options include Henderson Secondary (1.5km) and Queenstown Secondary (1.8km), both non-affiliated neighbourhood schools.

6. Retail and Amenities – Viva Vista 830m, Kent Ridge Park Adjacent

Viva Vista Shopping Mall is approximately 830m away, offering daily essentials through Cold Storage and basic F&B options. Mapletree Business City’s retail podium (740m) provides additional lunch and coffee options, though neither constitutes a lifestyle mall. VivoCity, the district’s primary regional mall, requires a short bus or car ride. Kent Ridge Park and Labrador Nature Reserve provide immediate green buffer – the hillside setting delivers on the nature proximity promise without overstating it.

Sales Performance

Terra Hill has moved 189 of 270 units as of 14 April 2026, representing a 70% take-up rate over 37 months since the February 2023 launch. This translates to an average velocity of 5.1 units per month across the marketing period – a respectable pace for a mid-sized freehold project in the Rest of Central Region.

URA transacted median sits at S$2,690 PSF across 51 caveats lodged in the last 12 months, with a range of S$2,234 to S$2,857 PSF. This transacted median reflects what buyers have actually paid for units where legal completion has progressed, capturing both early launch discounts and subsequent price adjustments. The PSF floor of S$2,234 suggests some units moved at promotional pricing, while the S$2,857 ceiling reflects premium stack or unit type premiums.

Contextualised against District 05’s overall condominium median of S$2,172 PSF (1,947 transactions, last 12 months), Terra Hill trades at a 24% premium. This premium is consistent with freehold tenure and new launch specifications, though buyers should note that the developer’s current asking prices for remaining units may exceed the transacted median, particularly for higher floors and larger layouts.

HDB Upgrader Catchment

Clementi and Queenstown form the primary HDB resale catchment for Terra Hill, with Dawson, Tanglin Halt, Holland Village, and West Coast estates clustered within a 2km radius. Over the past 24 months these towns recorded 2,404 resale transactions:

| Flat Type | Median Price | Typical Equity | Transactions |

| 3 Room | S$420k | S$200k – S$350k | 1,132 |

| 4 Room | S$930k | S$350k – S$500k | 946 |

| 5 Room | S$1.055M | S$500k – S$700k | 292 |

| Executive | S$1.11M | S$600k – S$900k | 34 |

The combined 4-room median of S$800k (Clementi) and S$969k (Queenstown) implies upgrader cash equity of S$350k to S$500k after loan redemption and CPF restoration. Combined with a 75% LTV mortgage, this delivers a purchasing envelope of roughly S$1.4M to S$2.0M. Terra Hill’s S$2.21M entry for a 2-bedroom sits above this band – the compact tier is therefore not accessible to median 4-room upgraders without supplementary capital.

The 3-bedroom at S$2.49M and 4-bedroom at S$3.53M require 5-room or executive equity (S$500k–S$900k) combined with dual-income support. The 5-bedroom at S$5.57M targets established private property owners consolidating freehold assets.

The 70% take-up pace despite the elevated entry quantum indicates Terra Hill is drawing mature Queenstown and West Coast catchment owners, family upgraders with existing private property equity, and legacy-focused buyers attracted to the freehold tenure rather than first-time HDB graduates.

Unit Mix & Pricing

| Type | Size Range (sqft) | From Price | PSF From | Total Units | Remaining |

| 2BR | 624 – 840 | S$2.21M | S$2,745 | 40 | 1 |

| 3BR | 904 – 1,335 | S$2.49M | S$2,531 | 126 | 37 |

| 4BR | 1,302 – 1,894 | S$3.53M | S$2,667 | 63 | 35 |

| 5BR | 2,120 – 3,035 | S$5.57M | S$2,756 | 11 | 8 |

The unit mix skews heavily toward 3-bedroom configurations (126 units, 52% of inventory), with 4-bedroom units forming a meaningful 26% share (63 units). Nearly all 2-bedroom units have been absorbed – only 1 of 40 remains – signalling strong demand at the S$2.21M entry quantum. Conversely, 35 of 63 4-bedroom units (56%) and 8 of 11 5-bedroom units (73%) remain unsold, indicating buyer resistance at the S$3.53M to S$5.57M quantum range.

The developer’s current asking PSF ranges from S$2,531 (3BR entry) to S$2,756 (5BR entry), with 2BR units priced at S$2,745 PSF. This compressed PSF band across unit types suggests the developer is extracting premiums on larger absolute quantums rather than applying aggressive per-square-foot markups to premium layouts. Buyers eyeing remaining 4BR or 5BR units should negotiate – inventory overhang at these tiers provides leverage.

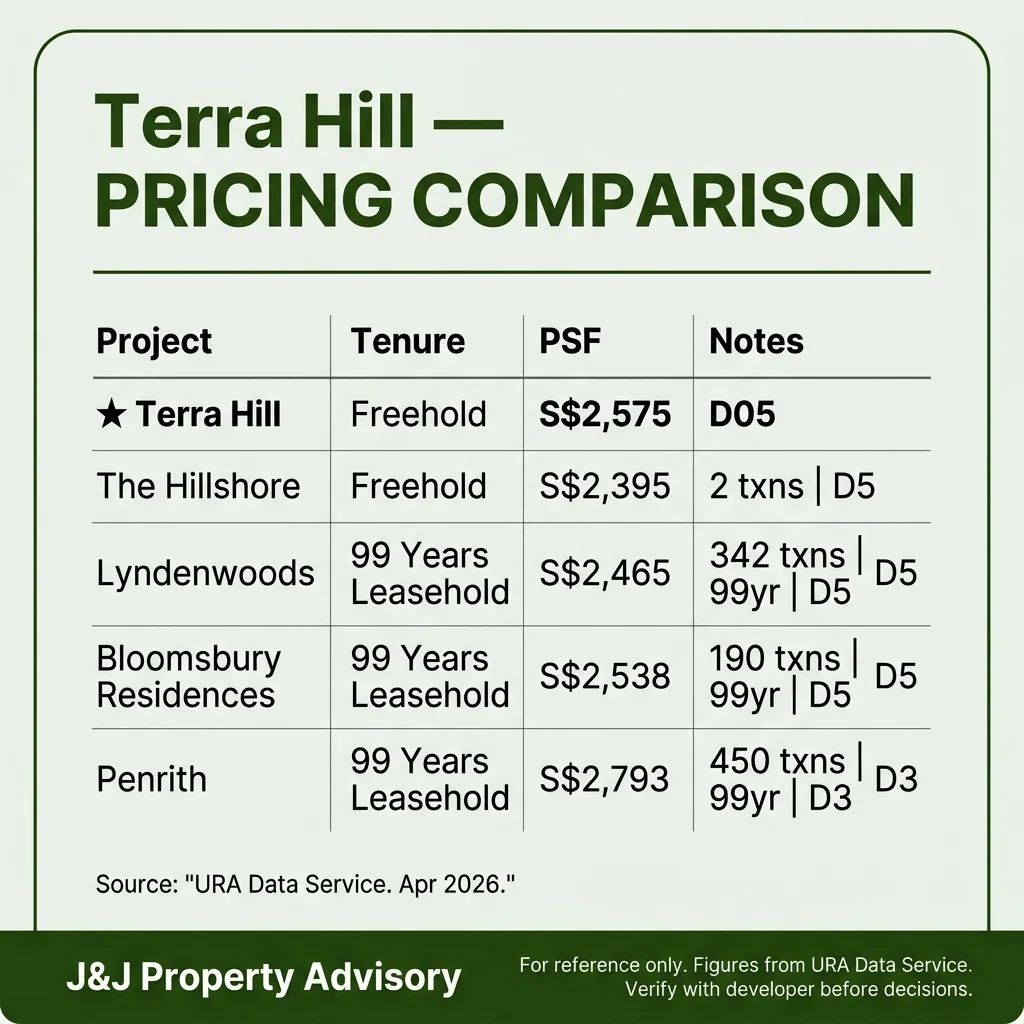

Comparables

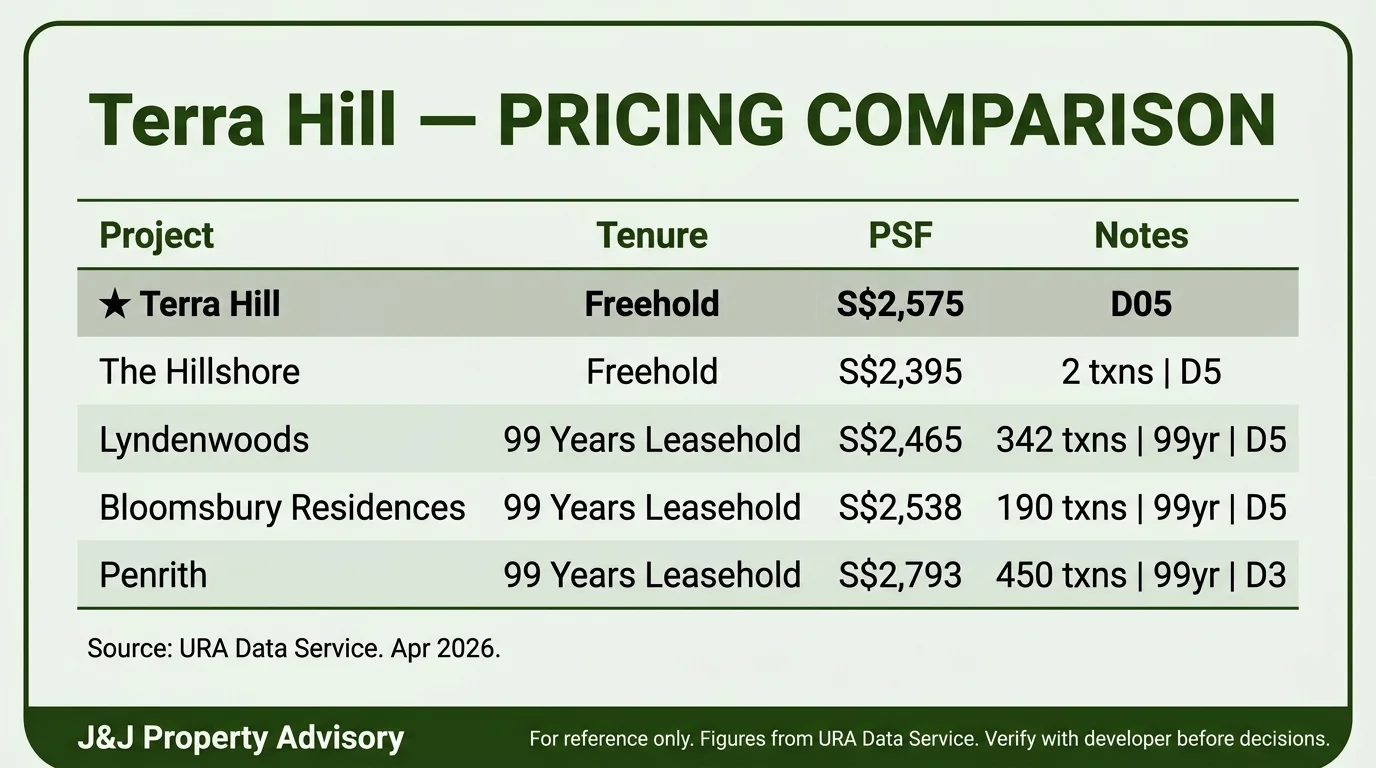

| Project | Median PSF | Transactions | Tenure | Expected TOP |

| Terra Hill | S$2,690 | 51 | Freehold | Q4 2026 |

| The Hillshore | S$2,395 | 2 | Freehold | Q2 2027 |

| Lyndenwoods | S$2,465 | 342 | 99 Years | Jun 2029 |

| Bloomsbury Residences | S$2,538 | 190 | 99 Years | Nov 2028 |

| Penrith | S$2,793 | 450 | 99 Years | Apr 2031 |

Terra Hill’s S$2,690 transacted median positions it at the upper end of District 05’s new launch spectrum. The Hillshore, another freehold project, shows a S$2,395 median across only 2 transactions – too thin for reliable comparison but indicative of freehold pricing below Terra Hill.

Lyndenwoods (99-year leasehold, S$2,465 median) and Bloomsbury Residences (99-year leasehold, S$2,538 median) both trade S$150-225 below Terra Hill on a per-square-foot basis, consistent with the typical freehold premium. Penrith’s S$2,793 median reflects its later TOP (April 2031) and likely newer specifications, though its leasehold tenure narrows the gap.

Terra Hill’s freehold status justifies a 9 – 12% premium over leasehold comparables in the same micro-location, but buyers paying today’s asking prices should ensure stack quality and view premiums validate the spread.

Key Strengths

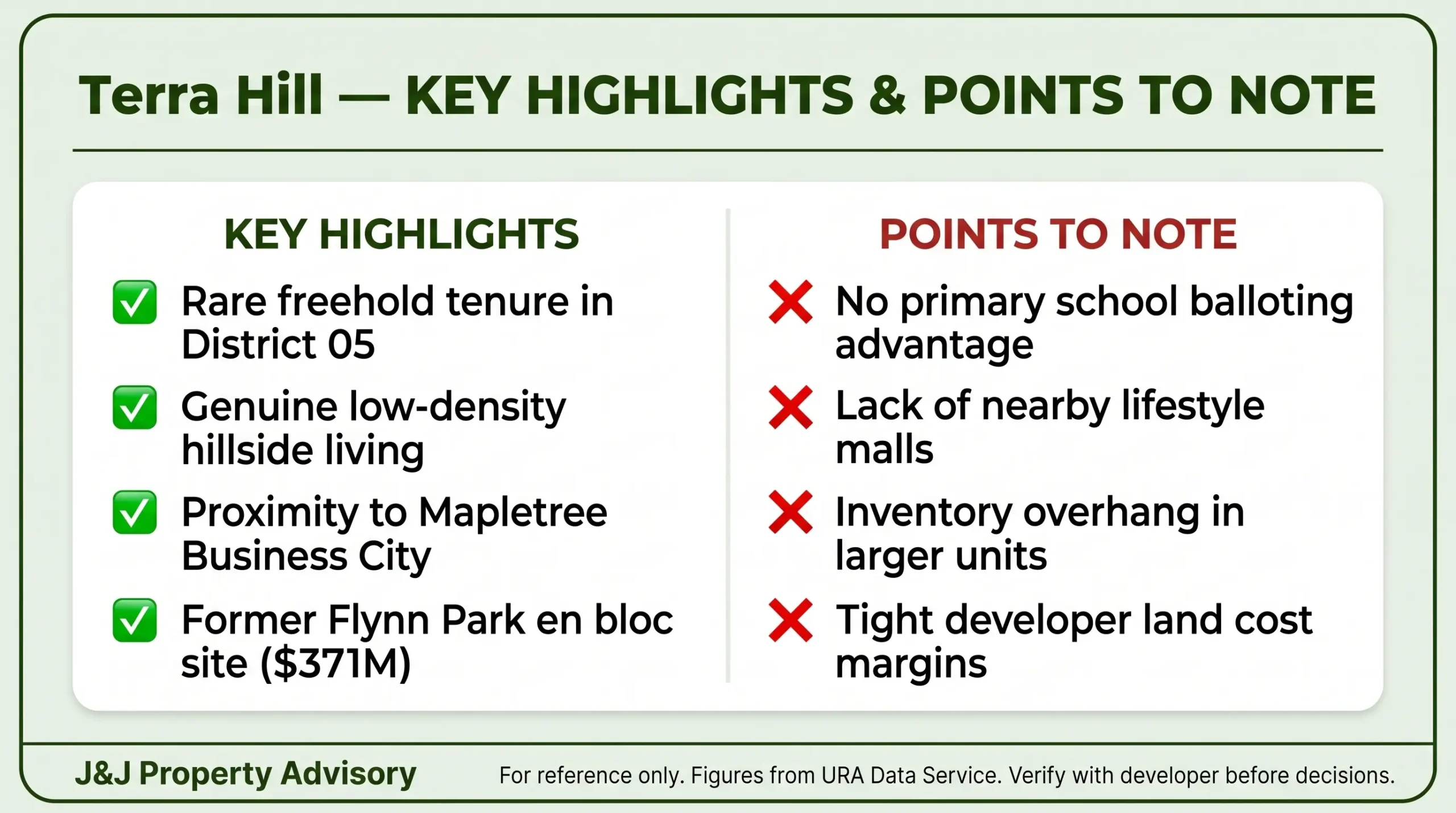

1. Freehold Tenure in a Supply-Tight Segment

Freehold launches in District 05 are scarce – Terra Hill is one of only two freehold projects (alongside The Hillshore) to reach the market in the Pasir Panjang-Queenstown corridor since 2020. This scarcity underpins long-term capital appreciation potential, particularly for buyers holding through multiple decades. The tenure also simplifies estate planning and appeals to legacy-focused local buyers unwilling to accept lease decay risk.

2. Genuine Low-Density Configuration

With 270 units across 19,365 sqm, Terra Hill achieves a site density well below the typical suburban condominium. The low-rise block layout and hillside terracing reduce visual density further, delivering a landed-adjacent living experience. This configuration attracts buyers stepping down from landed housing or upgrading from high-density developments. Facilities loading per capita also benefits from the lower unit count.

3. Proximity to Mapletree Business City and CBD Access

The 740m distance to Mapletree Business City and Circle Line connectivity position Terra Hill as a viable executive rental play. Expatriate tenants working at Google, Barclays, or AIA within the business park cluster will value the commute time, though rental rates must remain competitive against nearby leasehold alternatives. Owner-occupiers working in Alexandra, Buona Vista, or CBD nodes gain similar time efficiency.

4. Green Buffer and Nature Proximity Without Isolation

Kent Ridge Park and Labrador Nature Reserve flank the development, delivering on the hillside retreat narrative without sacrificing urban connectivity. The greenery buffer is genuine – not marketing spin – but buyers should recognise this is city-fringe nature access, not true suburban tranquillity. The trade-off here works for buyers who want weekend trail access without committing to Bukit Timah or East Coast distances.

5. Developer Track Record

Hoi Hup Realty has delivered multiple residential projects including The Tapestry and The Antares, while Sunway Group brings regional property expertise from Malaysia. Their 15-year partnership track record provides confidence in delivery quality and timeline adherence.

Points to Watch

1. Phase 2C School Distance – No Primary School Advantage

Blangah Rise Primary at 1.72km falls within Phase 2C (1-2km), eliminating proximity-based balloting advantages for families. Phase 2C balloting is effectively random, providing no edge over applicants living further away. Families banking on school proximity for primary-age children should recalibrate expectations – this is not a school-zone play. Secondary school options like Henderson and Queenstown Secondary are non-affiliated neighbourhood schools, offering no additional balloting leverage.

2. Retail Amenity Gap – No Lifestyle Mall Within Walking Range

Viva Vista (830m) and Mapletree Business City (740m) cover daily essentials and office F&B, but neither functions as a lifestyle or weekend destination mall. VivoCity requires a bus or car ride, as does Queensway Shopping Centre. Families accustomed to integrated mall-MRT hubs like Tampines or Jurong East will find the amenity landscape sparse. This gap matters most for retirees or non-driving residents who rely on walkable retail variety.

3. Unit Mix Imbalance – Inventory Overhang in 4BR and 5BR Tiers

With 56% of 4-bedroom units and 73% of 5-bedroom units still unsold after 37 months, the developer faces clear inventory pressure at the S$3.53M and S$5.57M quantum levels. This overhang signals buyer resistance to absolute pricing, not necessarily unit quality. Buyers targeting these tiers should negotiate aggressively – the developer’s incentive to clear pre-TOP inventory will strengthen as Q4 2026 approaches. Conversely, this inventory pattern raises questions about resale liquidity for larger units in future cycles.

4. Tight Land Cost Multiple – Limited Developer Margin Buffer

The land cost of S$1,355 PSF PPR against a launch PSF from S$2,531 yields a 1.87x multiple, below the market norm of approximately 2.27x. This tight margin suggests the developer paid aggressively at the land auction, leaving less pricing cushion for future uplifts. While buyers benefit from competitive initial pricing, the narrow spread limits the developer’s ability to absorb market downturns through discounting without eroding profitability. This dynamic could constrain resale pricing flexibility if District 05 softens.

5. Greater Southern Waterfront – Upside With Caveats

Terra Hill benefits from Greater Southern Waterfront proximity, with Phase 1 covering the Pasir Panjang area targeted for completion by the early 2030s and full GSW buildout expected by 2040. The first BTO launch on the former Keppel Club site arrived in October 2025, and port relocation to Tuas is underway. While these catalysts are real, the bulk of infrastructure uplift will materialise after Terra Hill’s Q4 2026 TOP. Buyers should underwrite the purchase based on today’s connectivity, treating GSW as genuine medium-term upside rather than speculative optionality.

6. Rental Yield Compression from New Launch Premium

District 05’s typical gross yield of 3.0-4.0% faces a 0.4% haircut for new launch pricing, compressing expected yields to 2.6-3.4%. A 3-bedroom unit purchased at S$2.49M (developer asking) would need to command approximately S$6,500-7,000 monthly rent to achieve 3% gross yield – achievable for executive tenants at Mapletree Business City but tight against leasehold comparables offering lower quantums. Investors should stress-test rental assumptions against actual Mapletree tenant profiles and existing vacancy rates in the micro-location.

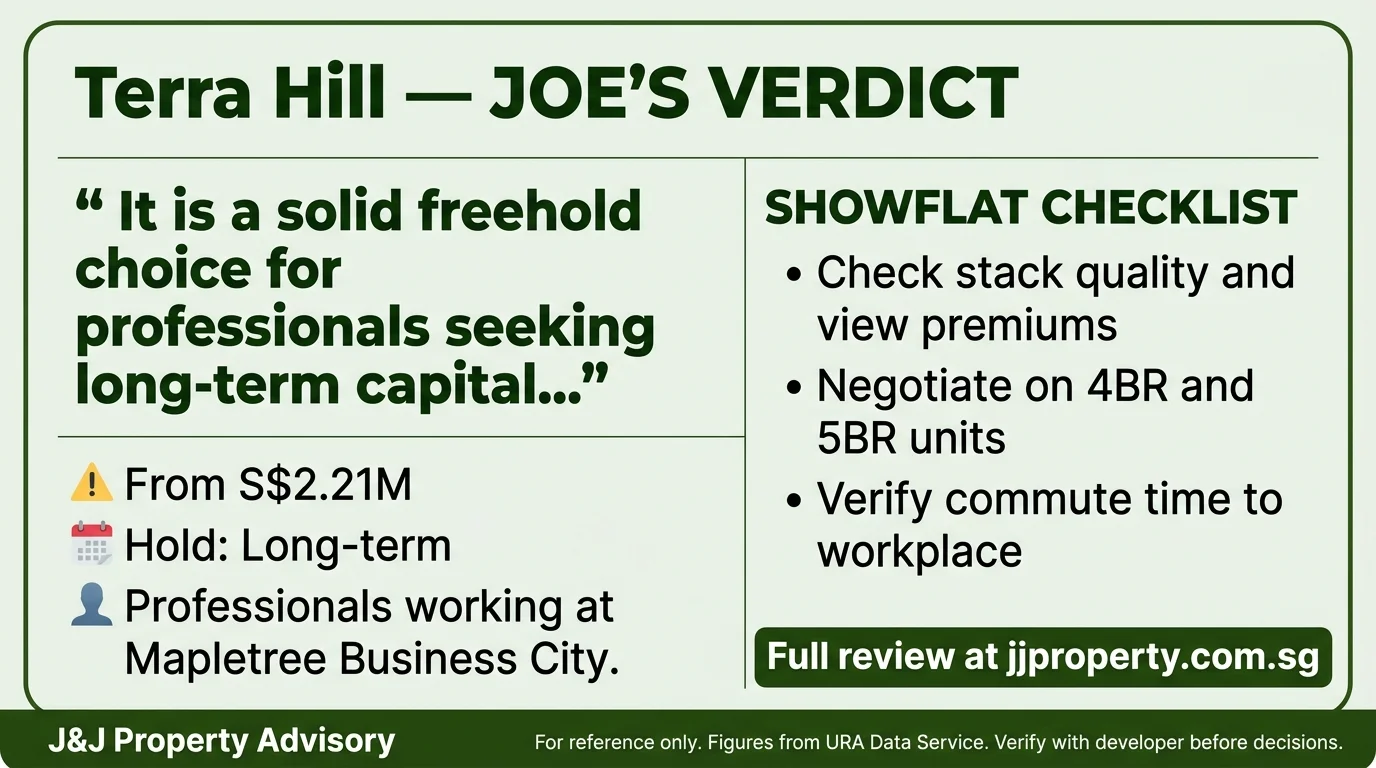

Bottom Line

Terra Hill offers a credible freehold proposition in a supply-starved segment, but buyers must price in the trade-offs. The S$2,690 transacted median reflects genuine scarcity value – freehold tenure, low-density configuration, and proximity to employment nodes justify the 24% premium over District 05’s overall median.

The 70% take-up rate after 37 months confirms steady absorption, though inventory overhang in 4BR and 5BR tiers signals quantum resistance. Buyers should focus on the 3BR segment, where 29% unsold inventory still offers selection without the pricing baggage of larger layouts.

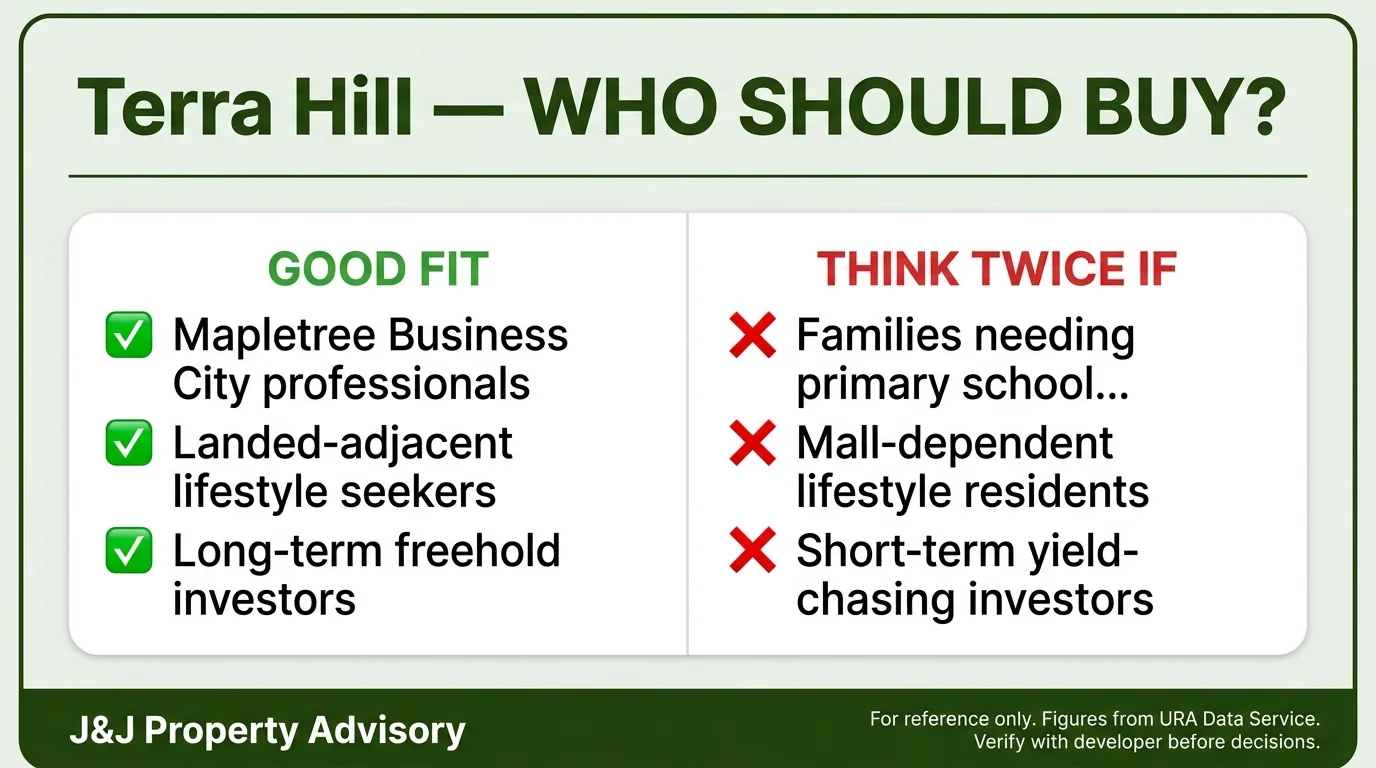

The location works for specific profiles – executives commuting to Mapletree Business City, downsizers seeking landed-adjacent density, and long-term holders banking on freehold appreciation. It does not work for school-focused families (no Phase 2B advantage), mall-dependent lifestyles (retail gap), or yield-chasing investors (compressed rental returns).

The tight land cost multiple (1.87x) delivers competitive entry pricing but limits developer margin for future discounting, reducing resale pricing flexibility if District 05 corrects. Buyers should negotiate hard on remaining 4BR and 5BR units – the developer’s pre-TOP urgency is your leverage.

For Own-Stay Buyers:

If you work at Mapletree Business City, Buona Vista, or Alexandra and value freehold tenure over lease certainty, Terra Hill delivers genuine time-cost savings and long-term holding optionality. The low-density site appeals to downsizers from landed housing or upgraders seeking space without vertical density.

However, families prioritising primary school balloting should look elsewhere—Phase 2C distance provides no advantage. Budget for car ownership given the retail amenity gap, and underwrite the purchase based on today’s connectivity, not speculative Greater Southern Waterfront upside alone.

For Investment Buyers:

Rental yields in the 2.6-3.4% range require disciplined tenant targeting – Mapletree Business City expatriates represent the core demand base, but competition from cheaper leasehold alternatives limits pricing power. The freehold tenure supports long-term capital appreciation over 15-20 year holding periods, but near-term rental returns will lag higher-yielding suburban plays.

Avoid 4BR and 5BR units given the 56-73% unsold inventory – resale liquidity risk is material. If deploying capital for legacy wealth preservation rather than yield optimisation, the freehold play works. If chasing rental income, suburban leasehold delivers better risk-adjusted returns.

Who Is This For

Good fit:

- Mapletree Business City, Buona Vista, or Alexandra professionals prioritising ≤12-minute commutes and freehold tenure over lease certainty. Terra Hill delivers time-cost savings alongside long-term holding optionality that leasehold alternatives cannot replicate.

- Downsizers from landed housing seeking low-density hillside living without the landed quantum. The 3-bedroom from S$2.49M (904 – 1,335 sqft) offers generous layouts with garden views and restrained neighbour density.

- Long-term freehold investors targeting 15–20 year legacy holds in a supply-starved District 05 segment. Freehold tenure insulates against lease decay and supports inter-generational wealth transfer.

- Established private property owners consolidating nearby leasehold stock into permanent ownership. The tight $1,558 PSF PPR land cost (Feb 2022) means minimal developer-margin cushion is embedded in the asking price.

- 3-bedroom buyers targeting the sweet-spot tier with balanced inventory and strong rental demand. Roughly 29% of the 126 three-bedroom units remain unsold – selection still exists without the pricing baggage of larger layouts.

- Negotiation-disciplined buyers willing to anchor on 4BR and 5BR tiers where inventory overhang is material. The developer’s pre-TOP urgency is your leverage, 56 – 73% unsold in larger layouts converts overhang into personal discount.

Not ideal for:

- Families requiring guaranteed 1km school priority for Phase 2B balloting. No primary school falls within 1km of Terra Hill, eliminating priority-distance advantage.

- Mall-dependent lifestyle residents expecting walkable retail density. The nearest large mall (HarbourFront VivoCity) is over 4km away; immediate-area retail is limited to neighbourhood shops.

- Short-term yield-chasing investors expecting suburban-equivalent returns. New launch premium compresses gross yield to 2.6–3.4%, materially below cheaper leasehold alternatives in D05.

- Buyers targeting 4BR or 5BR tiers without long-hold appetite. 56 – 73% unsold inventory in larger layouts signals material resale liquidity risk over 5 – 10 year horizons.

- Investors requiring immediate positive cash flow post-TOP. The tight Mapletree Business City tenant pool creates void-period risk against a backdrop of cheaper leasehold competition.

- Car-free lifestyle buyers dependent on direct MRT access. No station sits within 500m – bus, car, or ride-hail reliance is structural rather than optional.

Review Date: April 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This review is based on publicly available data and official URA transaction records. It is not financial advice. Verify all details with the developer before making purchase decisions.