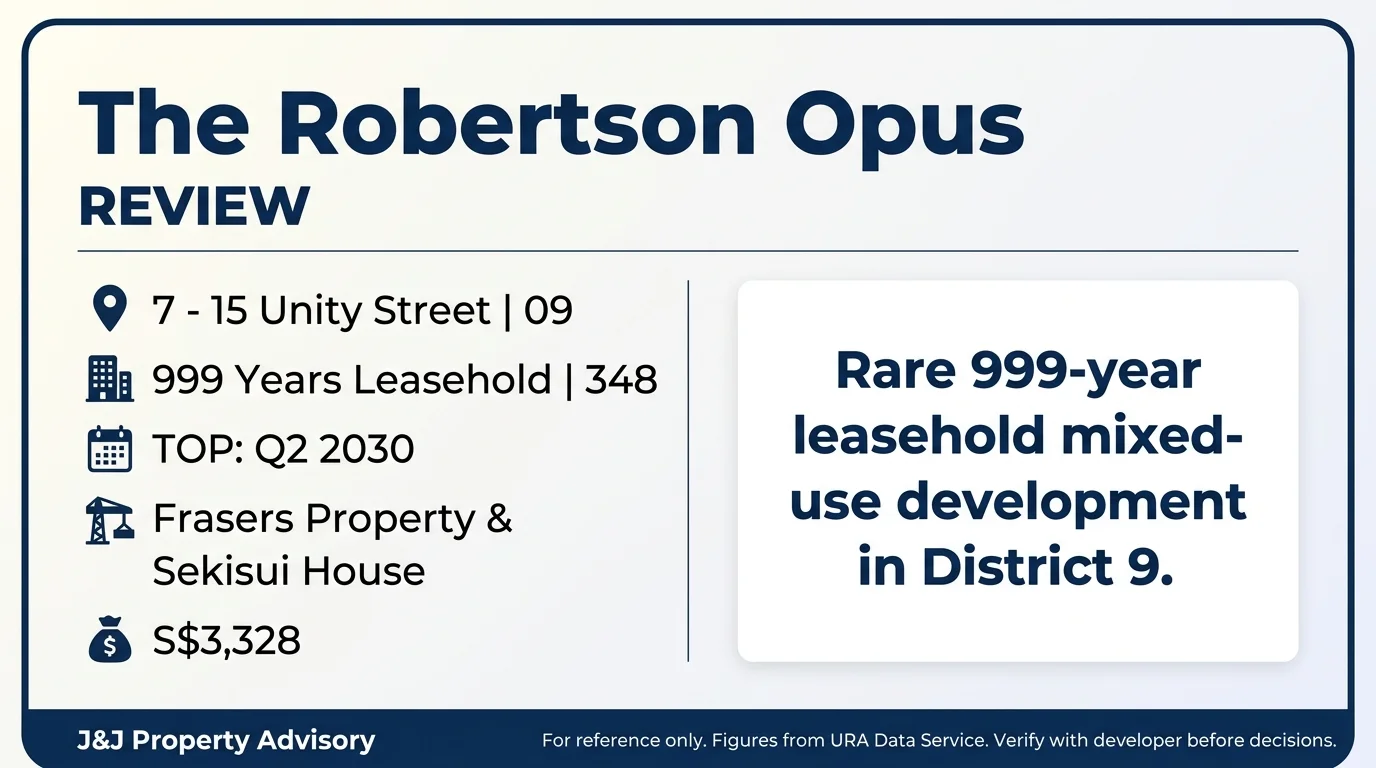

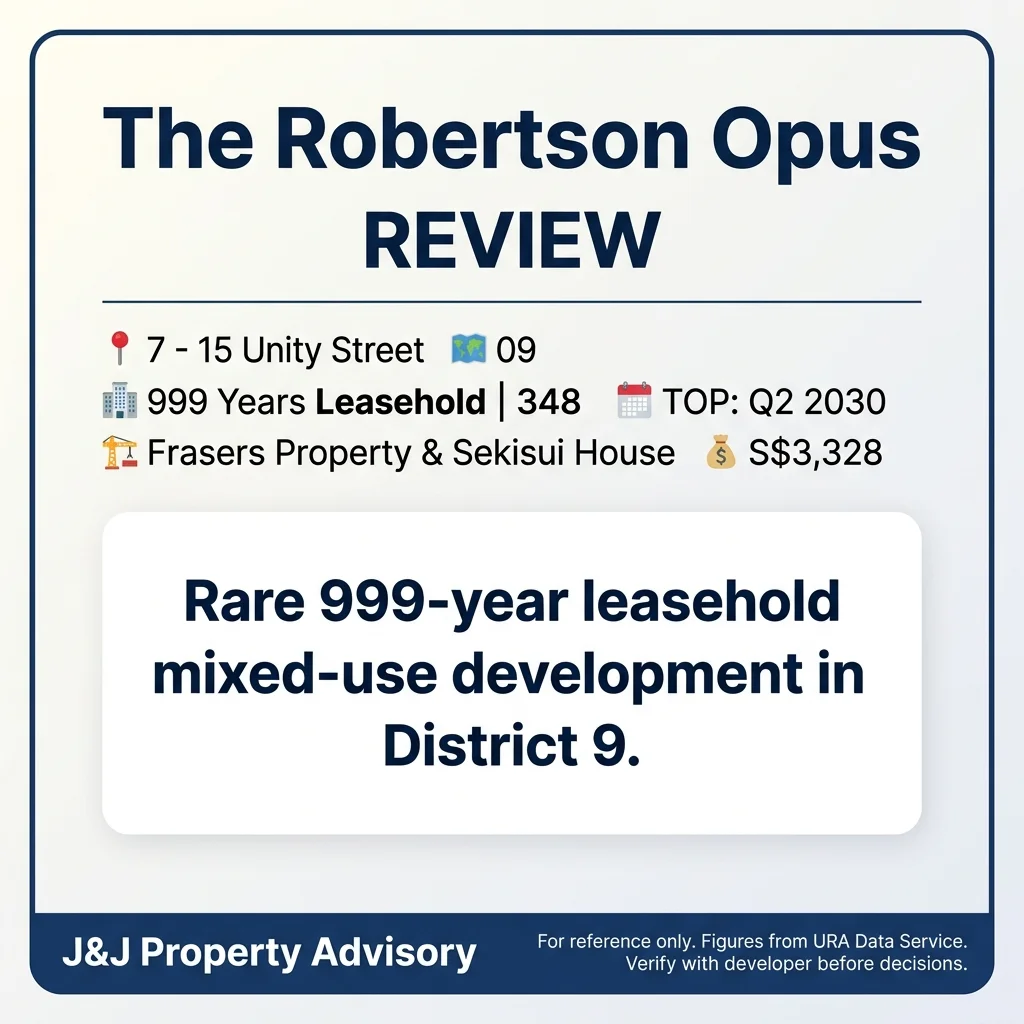

Project Snapshot

| Attribute | Details |

| Site Area | 97,980.8 sqft / 9,102.7 sqm |

| Developer | Frasers Property & Sekisui House |

| Tenure | 999 Years Leasehold |

| Total Units | 348 |

| Units Sold | 197 (56.6% take-up) |

| Median PSF | S$3,328 |

| Architect | ADDP Architects |

The Robertson Opus is a mixed-use development on Unity Street, occupying a site that sits within the Robertson Quay lifestyle belt and offers one of the longest leaseholds available in Singapore’s Core Central Region. The 999-year tenure positions this project as a quasi-freehold asset, a rare proposition in District 9 where the vast majority of new launches are 99-year leaseholds. The site’s integration of ground-level retail with residential towers above creates a live-work-play environment anchored within a mature, expatriate-heavy precinct known for its dining and riverside character.

Location & Connectivity

1. Fort Canning MRT (DT20) at approximately 300m

This is the primary access point for residents, providing Downtown Line connectivity that links directly to Marina Bay Financial Centre, Bugis, and Chinatown in under 10 minutes. The short walk from the development makes this a genuinely car-lite proposition for CBD commuters. Fort Canning station opened in 2017, ensuring modern platform amenities and barrier-free access.

2. Clarke Quay MRT (NE5) at approximately 710m and Chinatown MRT (NE4/DT19) at approximately 850m

The North-East Line provides additional redundancy for commuters heading towards Serangoon, Punggol, or HarbourFront, while Chinatown functions as an interchange station offering both Downtown Line and North-East Line options. This tri-station catchment within 850m is a strong connectivity advantage for a Core Central Region project. Clarke Quay’s nightlife and commercial activity may also influence buyer perception depending on unit orientation.

3. Dhoby Ghaut MRT (NS24/NE6/CC1) at approximately 930m and Havelock MRT (TE16) at approximately 950m

Dhoby Ghaut offers the widest network reach, connecting North-South, North-East, and Circle Lines, making Orchard Road, Marina Bay, and Harbourfront accessible without transfers. Havelock station on the Thomson-East Coast Line opened in 2021, further enhancing access to Caldecott, Woodlands, and Gardens by the Bay. The five-station catchment within 1km is among the strongest in District 9.

4. River Valley Primary School at approximately 640m

This co-educational school is the closest primary option and likely to be within the 1km distance priority bracket for most units, making it the primary choice for families targeting MOE placement. The school’s enrolment trends and recent PSLE performance should be reviewed separately, as proximity alone does not guarantee balloting success. St. Margaret’s Primary School at approximately 1.43km and Cantonment Primary School at approximately 1.79km provide additional options for families prioritising girls’ education or alternative catchment strategies.

5. The Central at approximately 650m, with Funan at approximately 940m

The Central offers grocery, F&B, and lifestyle retail in a mixed-use tower, providing day-to-day convenience without needing to travel to Orchard. Funan adds a more curated retail and tech-focused experience, while Chinatown Point and People’s Park Centre at approximately 730-870m provide budget-friendly dining and services. The neighbourhood is well-stocked for errands and casual dining but lacks the anchor department stores of Orchard Road.

6. Expressway access via River Valley Road and Havelock Road

The Ayer Rajah Expressway is accessible within 5-7 minutes via Havelock Road, connecting to the western corridor and Changi Airport. However, River Valley Road and adjacent streets experience moderate congestion during peak hours, particularly near Clarke Quay. Drivers should expect slower exit times during morning and evening rush periods, though this is manageable given the strength of MRT connectivity.

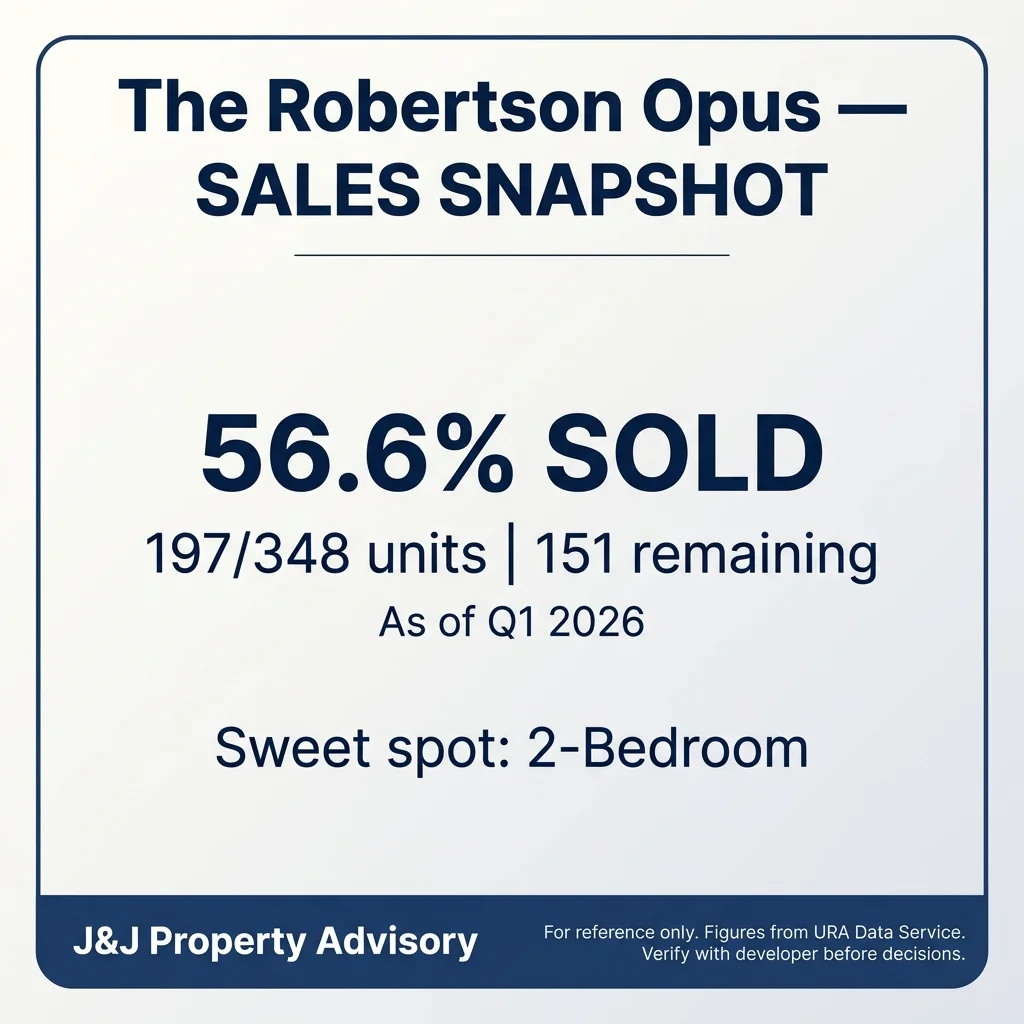

Sales Performance

| Metric | Figure |

| Units Launched | 348 |

| Units Sold | 197 (56.6%) |

| Median PSF | S$3,328 |

| PSF Range | S$3,245 – S$3,411 |

| Monthly Velocity | 56.3 units/month |

| District 9 Median | S$2,850 |

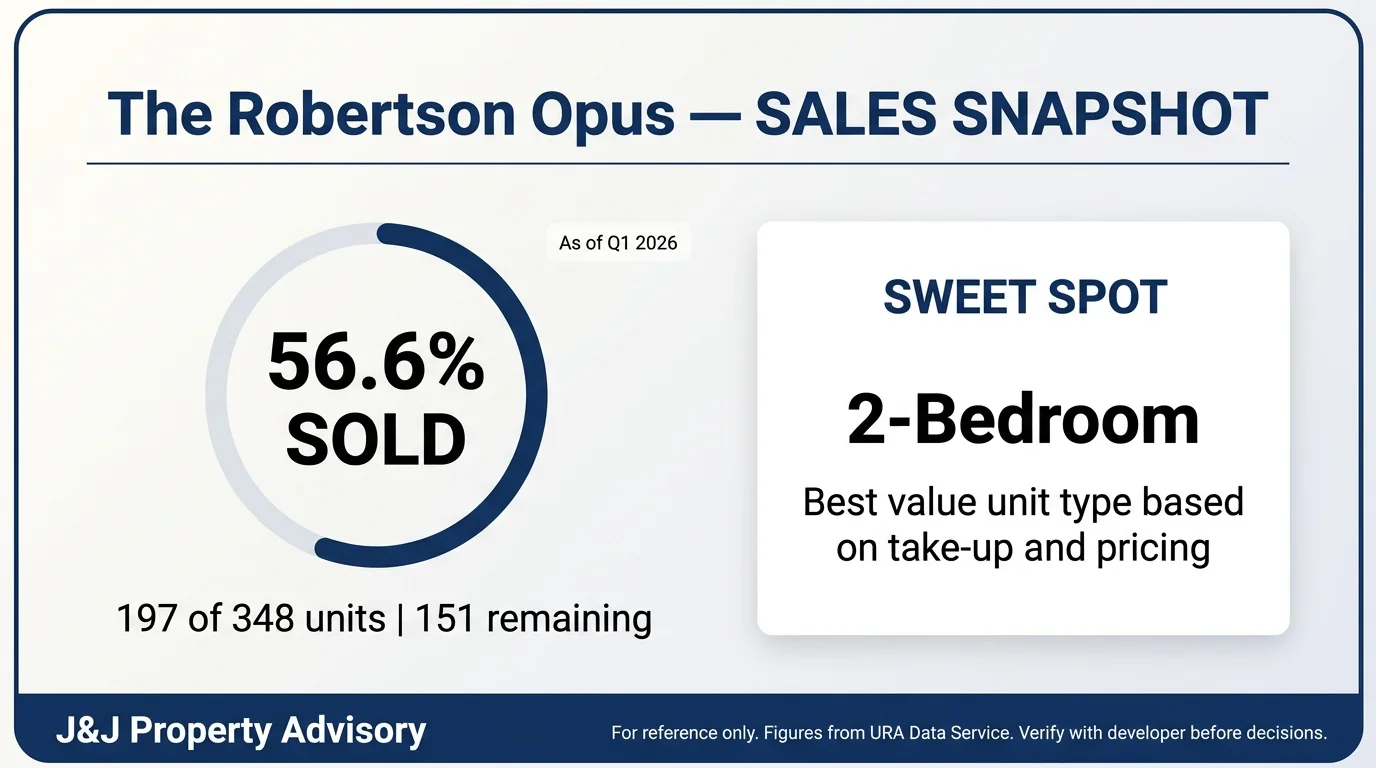

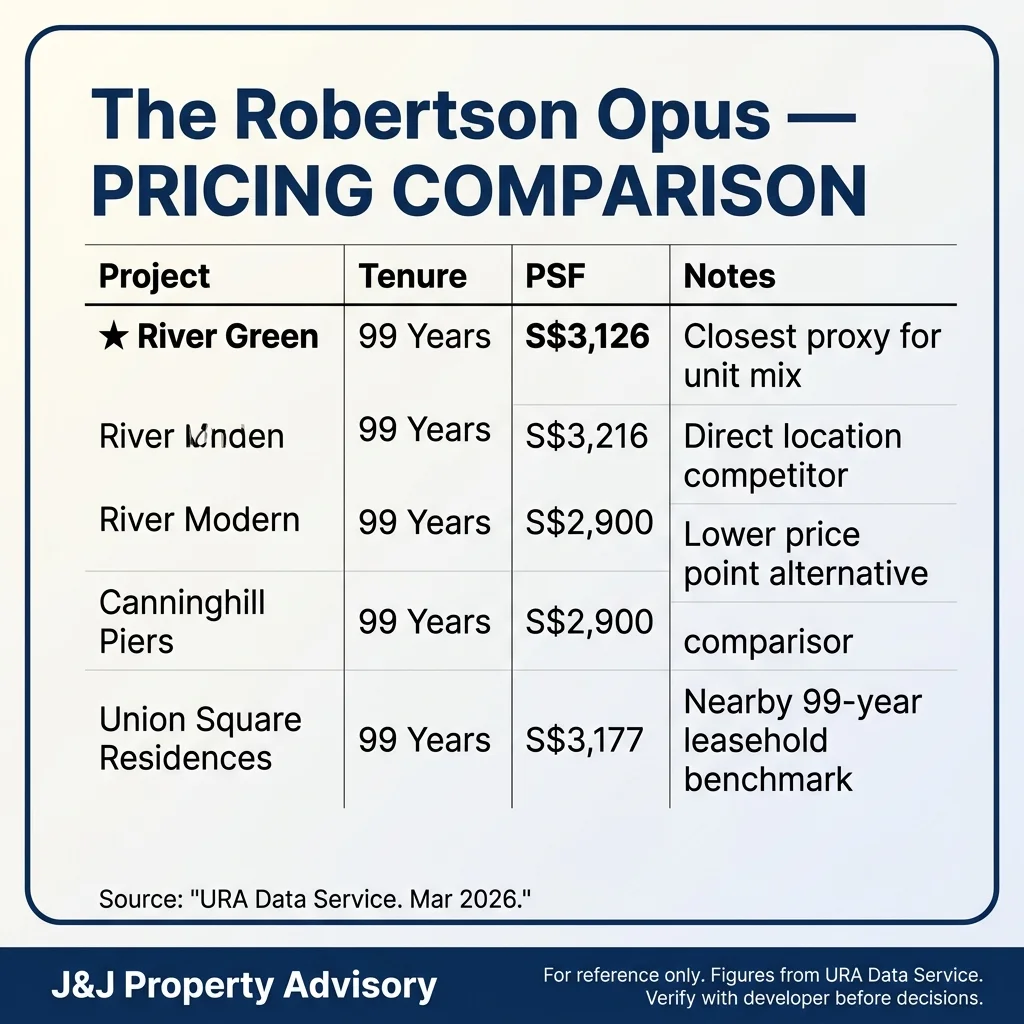

The Robertson Opus has sold 197 units out of 348 launched as of Q1 2026, reflecting a 56.6% take-up rate over three quarters of data. This translates to an average velocity of 56.3 units per month, which is solid for a Core Central Region project at this price point. The median PSF of S$3,328 sits comfortably above the District 9 median of S$2,850, reflecting a premium of approximately 16.8% over the broader district average.

The PSF range of S$3,245 to S$3,411 shows relatively tight pricing discipline, suggesting the developer has maintained consistency across unit types and stack levels without excessive discounting. When benchmarked against other 99-year leasehold launches in the same precinct—River Green at S$3,126 and River Modern at S$3,216—the tenure premium is evident. The 999-year leasehold commands approximately 6-7% above comparable 99-year projects, which is modest given the tenure differential but reflects the current market’s price sensitivity.

The sales pace indicates steady demand rather than speculative frenzy, which aligns with the project’s positioning as a legacy asset for long-term holders rather than a flippable investment product.

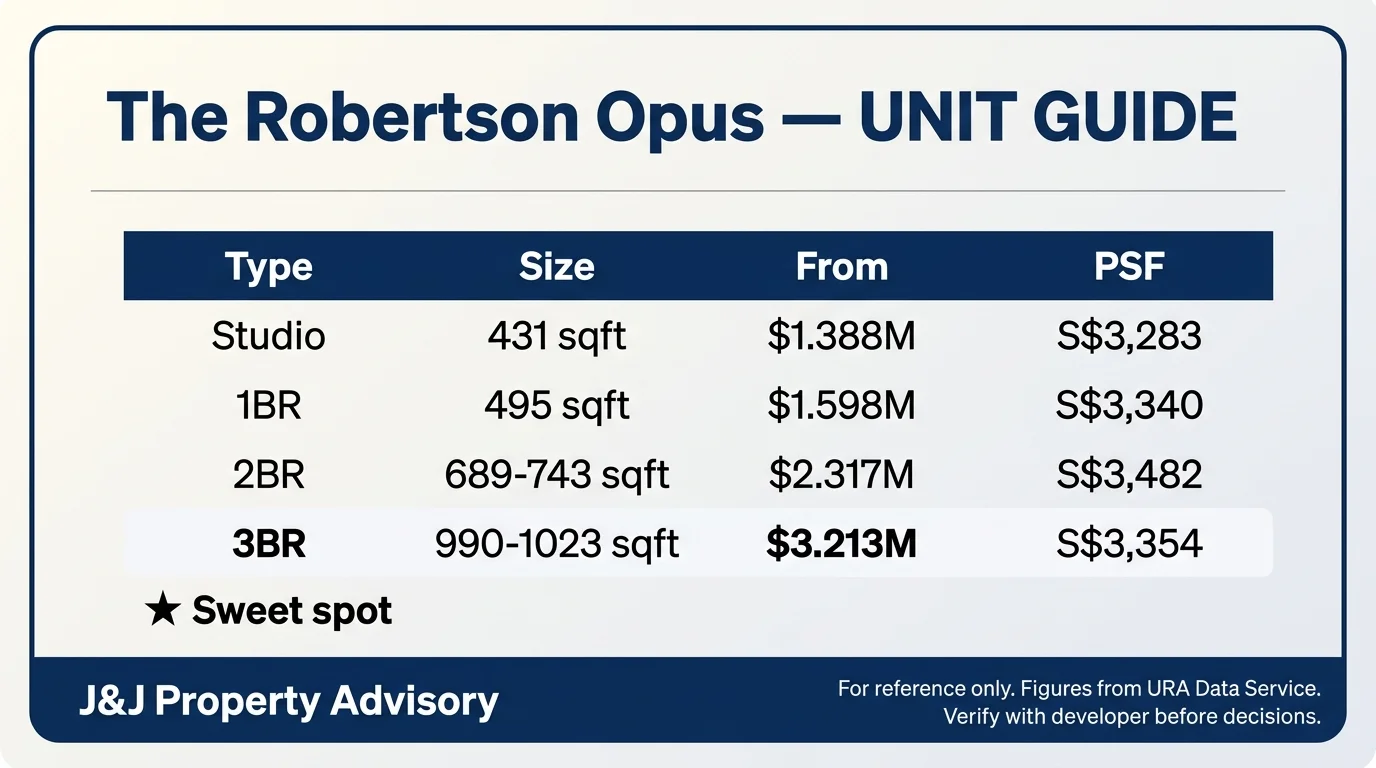

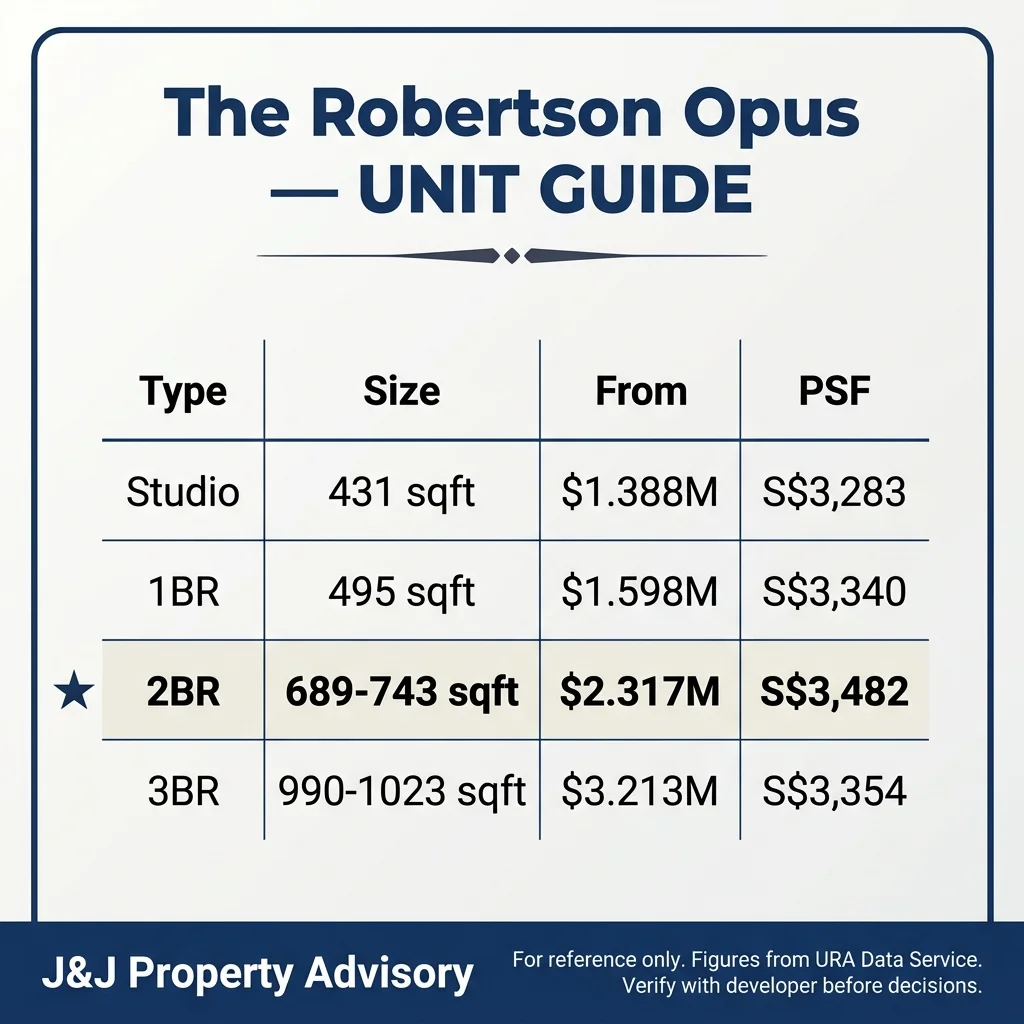

Unit Mix & Pricing

| Type | Size (sqft) | Quantum From | PSF From | Units |

| Studio | 431 | S$1.388M | S$3,283 | 32 |

| 1-Bedroom | 495 | S$1.598M | S$3,340 | 27 |

| 2-Bedroom | 689 – 743 | S$2.317M | S$3,482 | 60 |

| 3-Bedroom | 990 – 1023 | S$3.213M | S$3,354 | 29 |

The Robertson Opus offers a range of unit types skewed towards compact layouts, reflecting the developer’s read on demand from investors and expatriate tenants. The pricing reflects the developer’s launch figures and should be used as the baseline for quantum expectations.

The studio and 1-bedroom units are priced to attract investors chasing rental yields from single expatriates and young professionals working in the CBD. The 2-bedroom units at 689-743 sqft represent the volume segment, offering a balance between affordability and rental appeal. The 3-bedroom units at 990-1023 sqft are positioned for families but remain compact by District 9 family-unit standards, where 1,100-1,200 sqft is more common.

The entry quantum of S$1.388M for studios puts this project within reach of buyers with S$350K cash and CPF, assuming standard 75% LTV financing. The 3-bedroom units at S$3.213M require approximately S$800K in cash and CPF, which narrows the buyer pool to higher-net-worth households or dual-income families with significant accumulated CPF balances.

Comparables

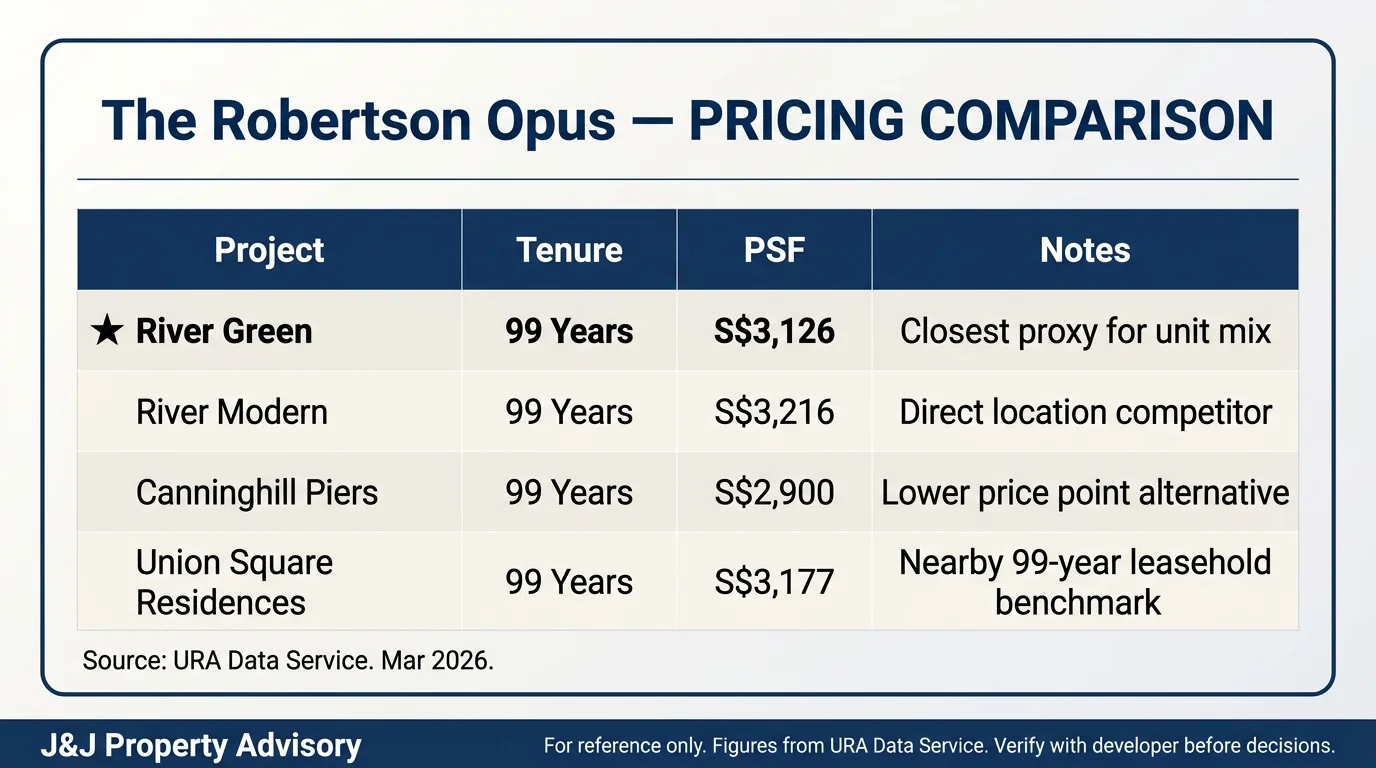

| Project | Median PSF | Transactions | Tenure | Expected TOP |

| River Green | S$3,126 | 485 | 99 Years Leasehold | Q1 2029 |

| River Modern | S$3,216 | 412 | 99 Years Leasehold | H2 2030 |

| Canninghill Piers | S$2,900 | 44 | 99 Years Leasehold | Jun 2027 |

| Union Square Residences | S$3,177 | 138 | 99 Years Leasehold | Q1 2029 |

The following projects provide transaction-based benchmarks for pricing and tenure positioning within District 9. All data is sourced from URA official records.

The Robertson Opus’s median PSF of S$3,328 places it approximately 6.5% above River Modern and 3.6% above River Green, the two closest proxies in terms of location and unit mix. The premium is justifiable on tenure grounds alone, though it is worth noting that Canninghill Piers transacted at S$2,900, which is 14.8% below The Robertson Opus. Canninghill Piers has a smaller sample size and an earlier TOP, which may explain the gap, but it also highlights the price sensitivity in the current market. Sophia Regency, a freehold project, recorded a median of S$1,978, but the 12-transaction sample size and December 2025 TOP make it a poor comparator for a 2030 project.

Key Strengths

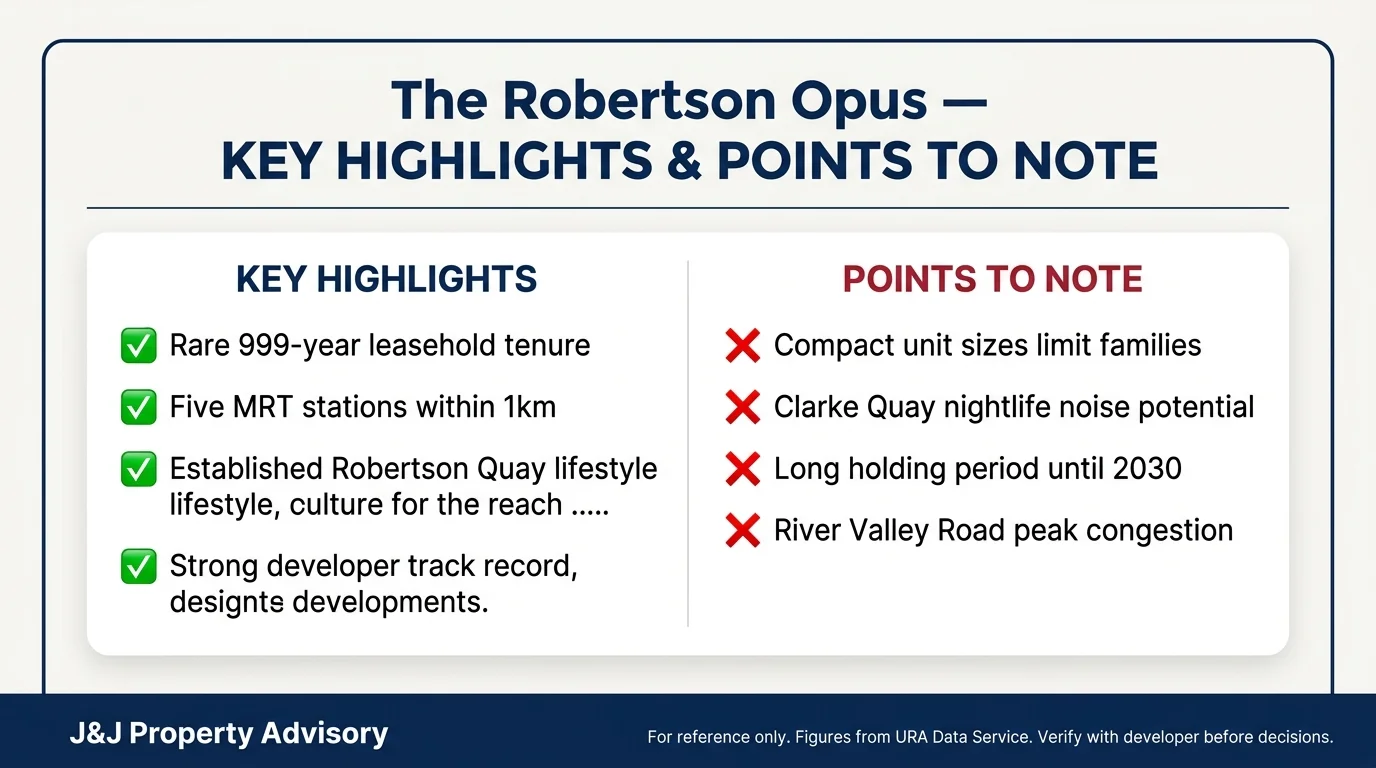

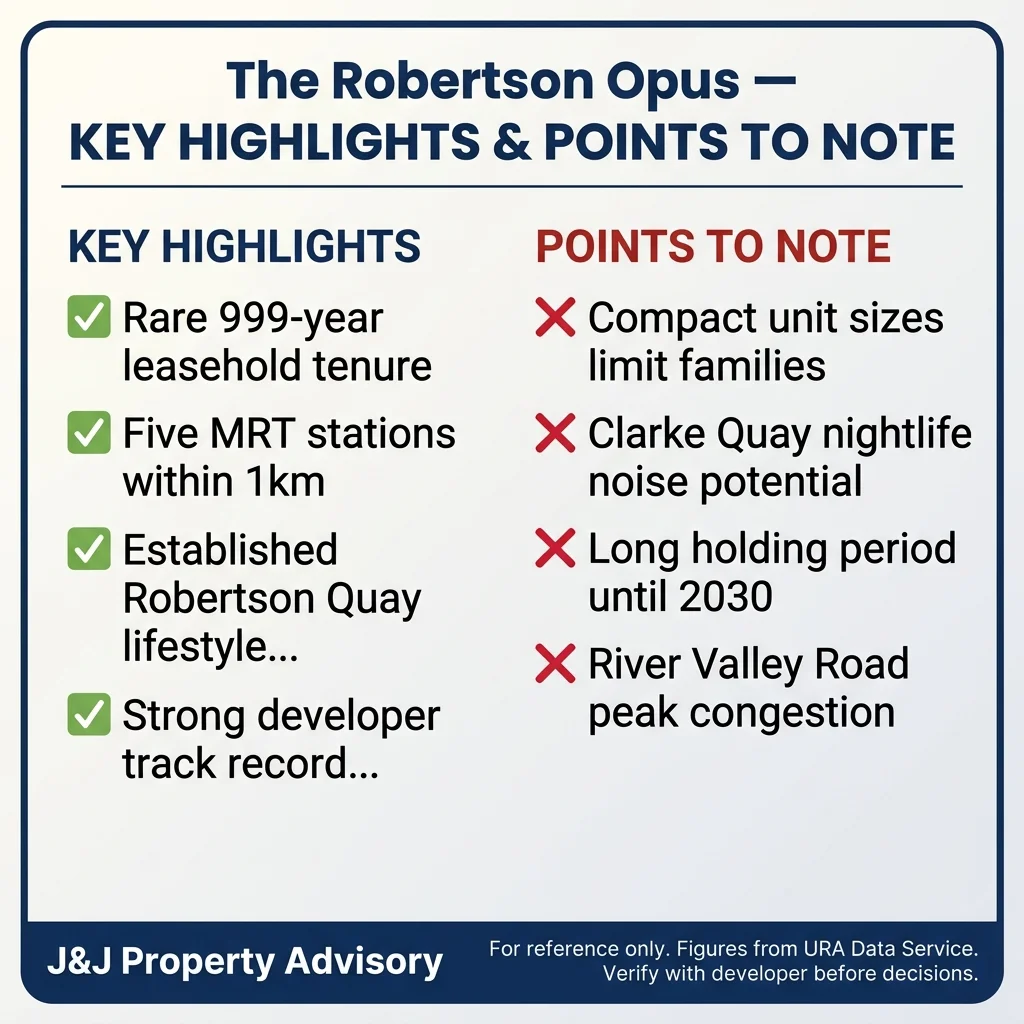

999-year leasehold tenure in a district dominated by 99-year projects

This is the single most differentiating attribute of The Robertson Opus. The tenure effectively eliminates lease decay concerns for at least three generations, making the property function more like a freehold asset in terms of resale and estate planning. For buyers prioritising long-term wealth preservation, this tenure removes the anxiety associated with the rapid depreciation curve that 99-year leaseholds experience after year 40-50.

Five MRT stations within 1km, covering four major lines

Fort Canning, Clarke Quay, Chinatown, Dhoby Ghaut, and Havelock provide Downtown, North-East, Circle, North-South, and Thomson-East Coast Line access within a 10-12 minute walk. This level of redundancy is rare and provides genuine optionality for both owners and tenants. A station closure or service disruption has minimal impact on daily commutes.

Established Robertson Quay lifestyle precinct with sustained expatriate demand

The neighbourhood has a 20-year track record as a preferred address for expatriate professionals, bankers, and diplomats. The concentration of boutique F&B outlets, riverfront promenades, and low-rise character creates a distinct identity that differentiates it from the high-density Tanjong Pagar corridor. This demand base provides rental resilience even during economic downturns.

Mixed-use integration with ground-level retail

The inclusion of retail units at the podium level adds convenience and creates an active street frontage that enhances the development’s sense of place. While retail success depends on tenant curation, the presence of commercial activity often supports long-term property values by embedding the project into the neighbourhood fabric rather than standing as an isolated residential tower.

Developer track record with Frasers Property and Sekisui House

Frasers Property Limited manages S$39.2 billion in assets across multiple geographies and asset classes, with a long history of delivering residential projects in Singapore. Sekisui House, headquartered in Osaka, has delivered over 2.6 million homes globally and brings Japanese construction quality standards to the partnership. This reduces completion risk and provides confidence in build quality and defect management post-handover.

Points to Watch

Modest 6-7% tenure premium suggests market is not fully pricing in 999-year value

While the tenure is a clear advantage, the pricing gap between The Robertson Opus and comparable 99-year projects is narrower than expected. This suggests that either the market is discounting the tenure due to current economic conditions, or buyers are prioritising quantum affordability over long-term tenure benefits. Resale buyers in 10-15 years may re-evaluate this premium, but today’s buyer is paying a relatively modest markup for a significant structural advantage.

Compact unit sizes limit family appeal for long-term owner-occupiers

The 3-bedroom units at 990-1023 sqft are functional but small for families with two or more children. Comparable family-oriented projects in Districts 10 and 11 typically offer 1,100-1,300 sqft for 3-bedroom layouts, which provide more flexible space planning as children age. Buyers targeting a 15-20 year own-stay horizon should evaluate whether the unit size supports their lifestyle needs beyond the first 5-7 years.

Clarke Quay nightlife proximity may affect liveability for families

Units facing Clarke Quay at approximately 710m may experience noise spillover during weekends and public holidays, particularly from outdoor dining and riverfront events. While the development’s mid-rise design and landscaping provide some buffer, families with young children should visit the site during evening hours to assess ambient noise levels. This is a locational trade-off inherent to the Robertson Quay precinct.

Q2 2030 TOP introduces 4-year holding period before resale eligibility

Buyers collecting keys in mid-2030 cannot sell until mid-2034 under current Seller’s Stamp Duty rules, which locks in a significant holding period during a phase of economic uncertainty. The 999-year tenure mitigates long-term depreciation risk, but short-term capital appreciation depends on District 9 sentiment over the next decade. Buyers should model cash flow and financing costs across the full holding period before committing.

Ground-level retail success depends on tenant mix and foot traffic activation

Mixed-use projects live or die based on the quality and stability of their retail tenancies. If the ground-floor units remain vacant or attract low-footfall businesses, the development loses its intended vibrancy and becomes a maintenance burden for the MCST. Buyers should monitor the retail leasing progress in 2028-2029 as an indicator of the developer’s ability to curate a sustainable tenant mix.

River Valley Road congestion during peak hours reduces driving convenience

While MRT access is strong, owners who drive will face slower exit times during morning and evening peaks, particularly when heading towards the CBD or AYE. This is less of an issue for car-lite households but may frustrate families reliant on school runs or weekend trips. The trade-off is inherent to Core Central Region living but worth factoring into daily routine planning.

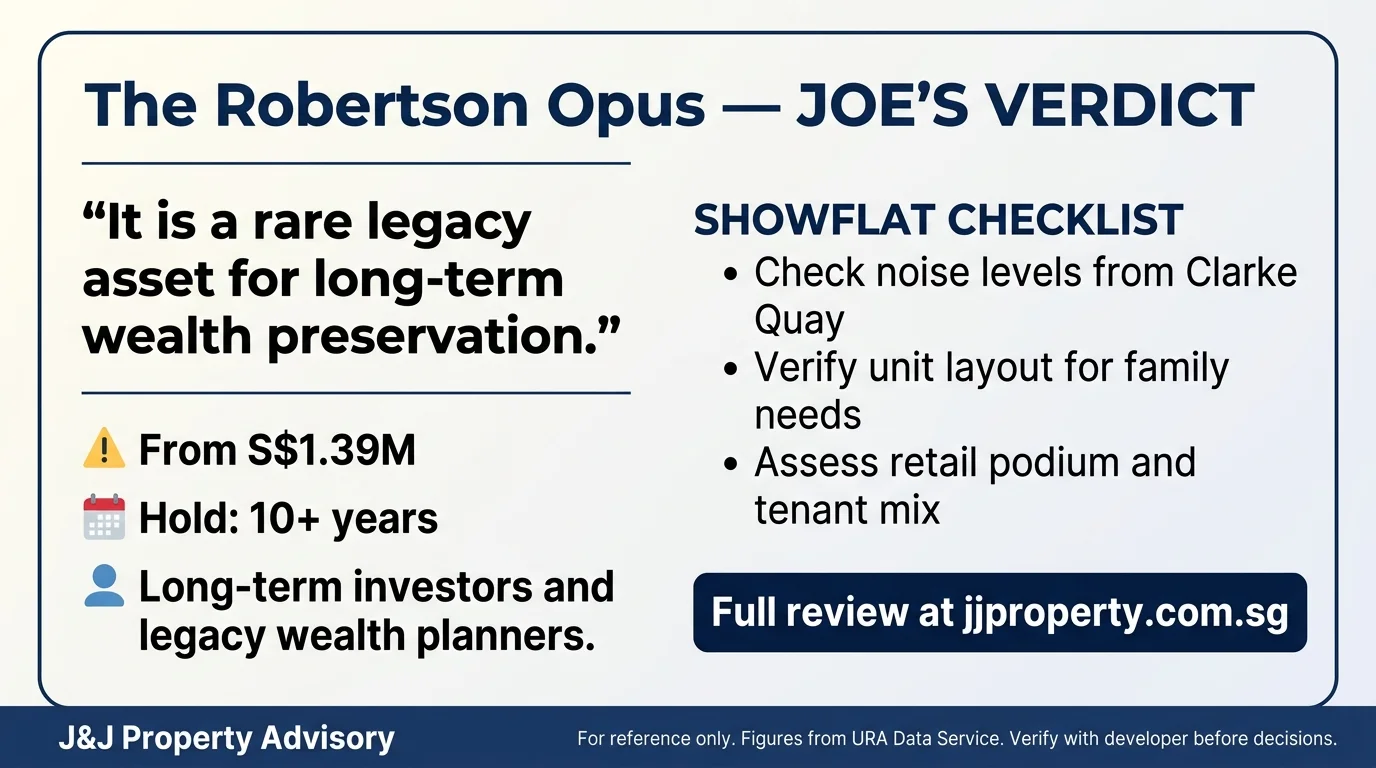

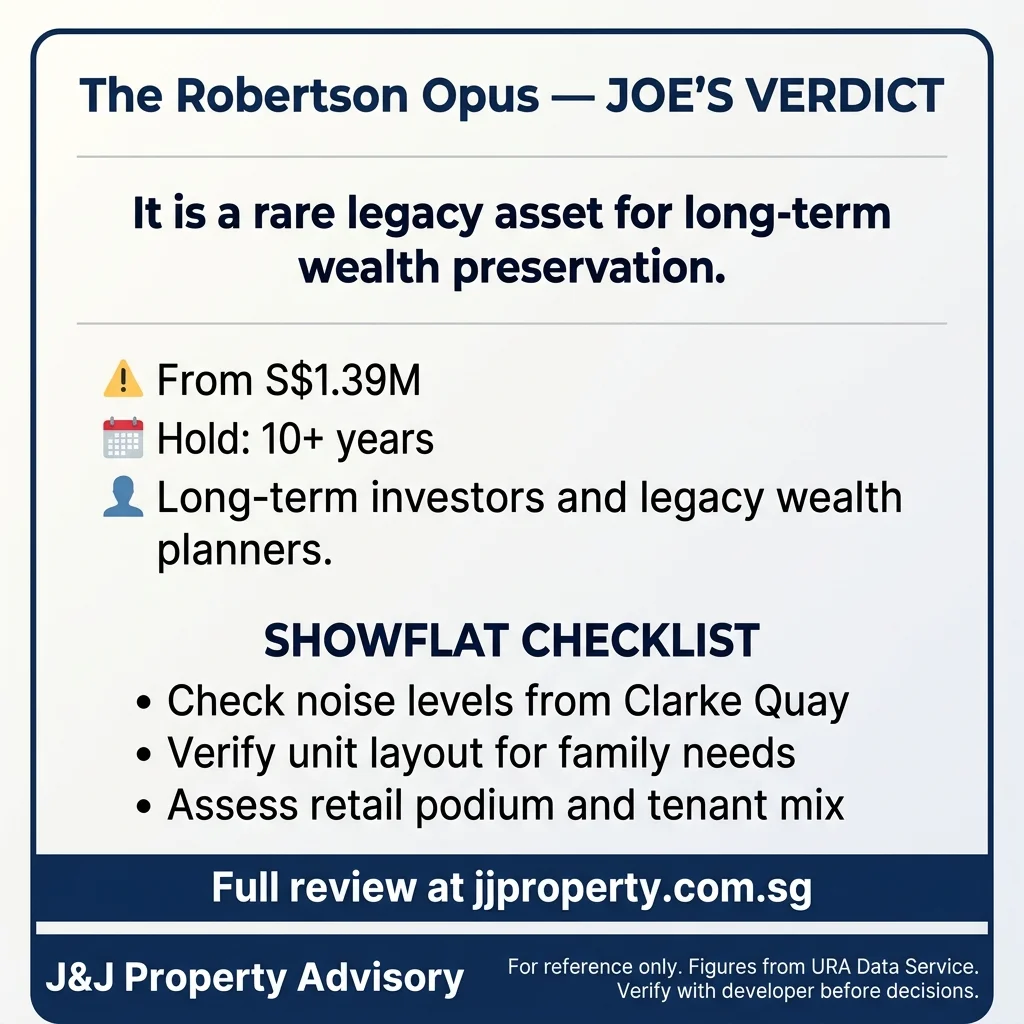

Bottom Line

The Robertson Opus is a disciplined play on tenure scarcity within a mature, expatriate-preferred precinct. The 999-year leasehold removes the primary structural weakness of most new launches—lease decay—and positions the asset as a multi-generational hold. The pricing at S$3,328 median PSF reflects a 6-7% premium over comparable 99-year projects, which is modest given the tenure differential but also suggests the market is not yet fully rewarding long-term thinking. The 56.6% take-up rate and steady monthly velocity indicate solid demand from buyers who understand the value proposition, but the compact unit sizes and Q2 2030 TOP introduce constraints for families and short-term investors.

This is not a project for buyers chasing quick gains or high rental yields. The rental market for Core Central Region properties at this quantum typically delivers 2.5-3.5% gross yields, which is respectable but not compelling for investors focused purely on income. The real value lies in the tenure, the location, and the resilience of the Robertson Quay precinct, which has weathered multiple economic cycles while retaining its expatriate appeal.

For Own-Stay Buyers

Families targeting a 15-20 year own-stay horizon will appreciate the tenure security and MRT connectivity, but should carefully evaluate unit sizes to ensure the layout supports long-term liveability as household needs evolve. The River Valley Primary School catchment at approximately 640m is a tangible advantage for young families, though balloting success is never guaranteed. Couples without children or empty-nesters will find the compact layouts functional and the neighbourhood amenities well-suited for a low-maintenance, walkable lifestyle. The project works best for households prioritising location and tenure over space.

For Investment Buyers

The 999-year tenure provides a clear differentiation point for expatriate tenants who value stability and are willing to pay a modest premium for it. Rental demand in the Robertson Quay belt is consistent, driven by banking professionals, embassy staff, and senior corporate executives who prefer the quieter riverside character over the high-density Tanjong Pagar corridor. Yields will be modest but stable, and the real upside comes from long-term capital preservation rather than short-term price appreciation. Buyers with a 10-15 year holding horizon and low leverage will find this a defensible allocation within a broader portfolio.

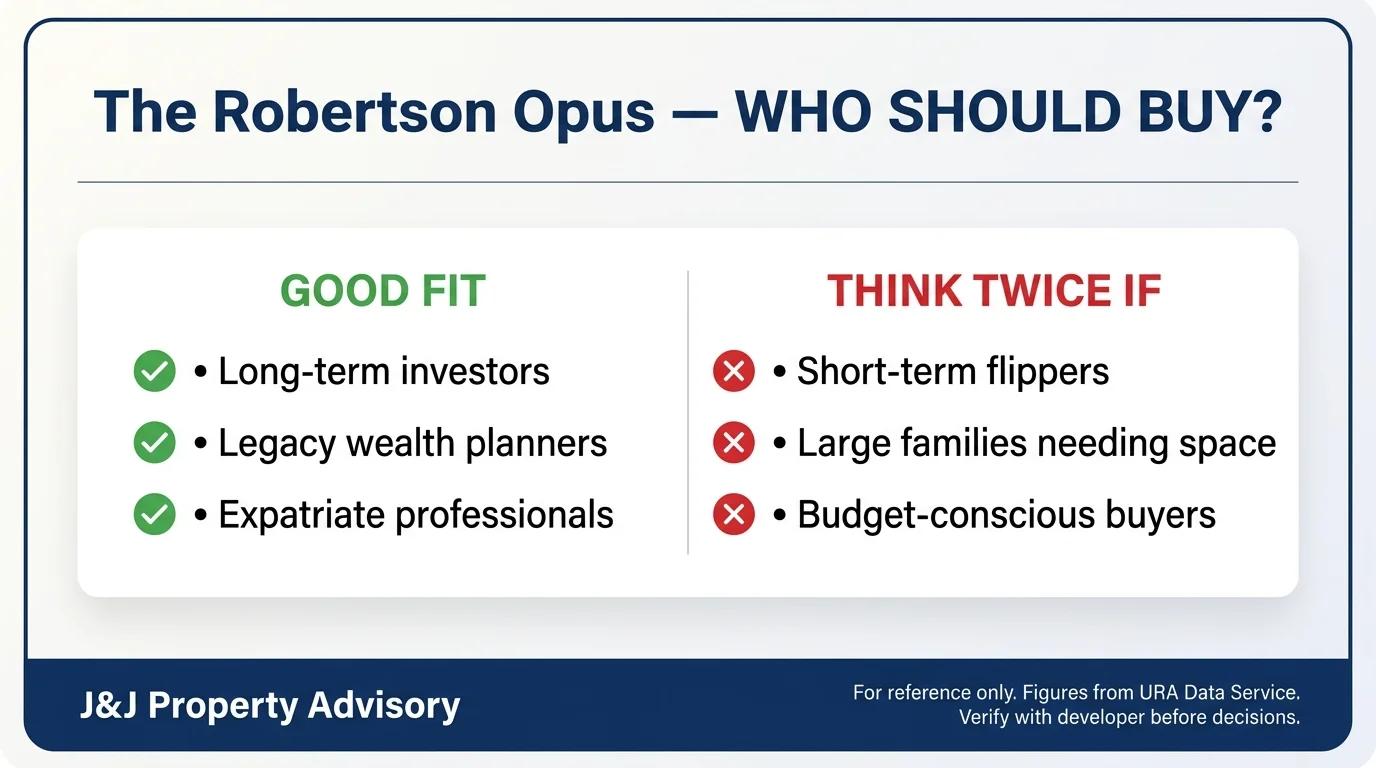

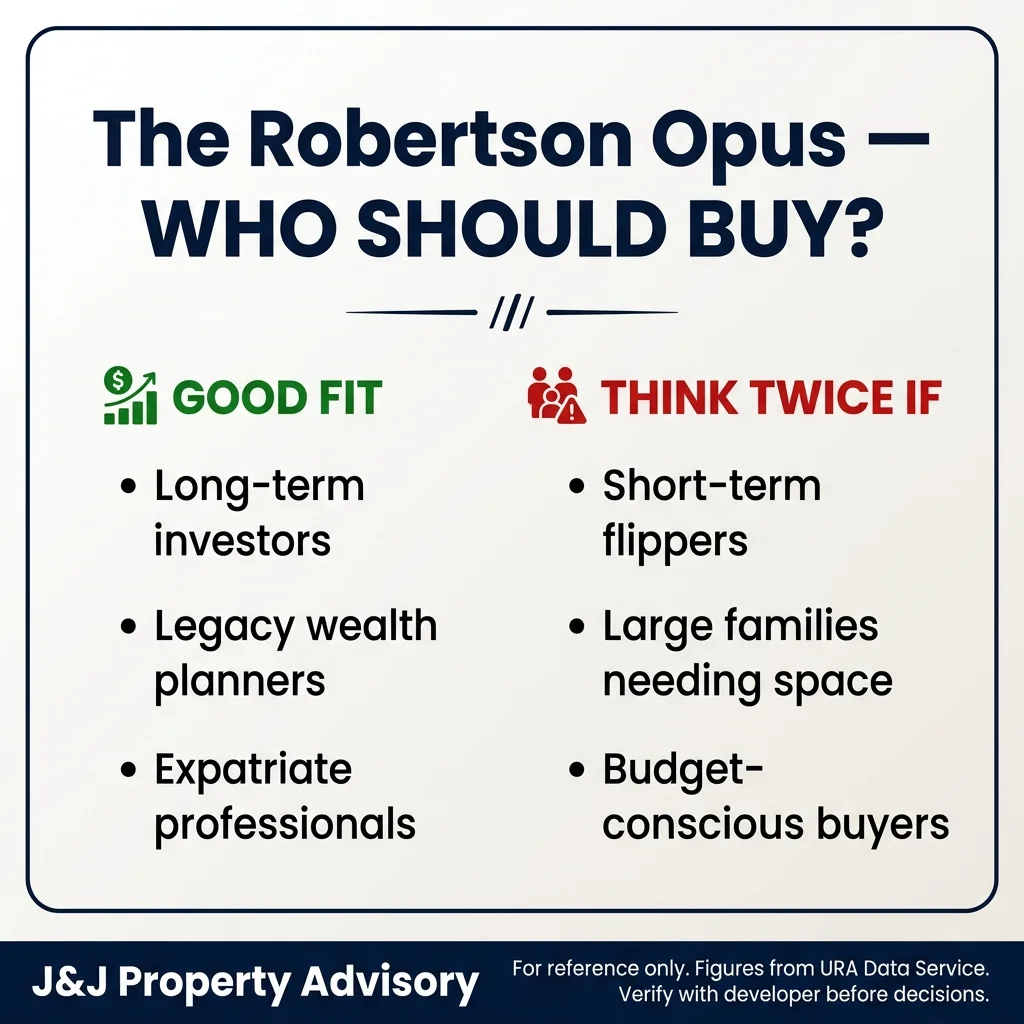

Who Is This For

Good fit:

- Buyers prioritising tenure security and willing to pay a 6-7% premium over 99-year leasehold projects for multi-generational wealth preservation.

- Expatriate professionals or returning Singaporeans who value Robertson Quay’s lifestyle character and require strong MRT connectivity to the CBD within 10-15 minutes.

- Families with one child targeting River Valley Primary School’s approximately 640m catchment, with realistic expectations around MOE balloting outcomes.

- Investors holding a diversified Core Central Region portfolio and seeking a low-volatility, long-tenure asset that provides rental stability rather than speculative upside.

- Empty-nesters or retirees downsizing from landed property who want a walkable, amenity-rich neighbourhood with strong public transport redundancy.

- Dual-income households with S$800K-1M in combined cash and CPF, targeting a 3-bedroom unit for a 10-15 year own-stay hold with minimal lease decay concerns.

Not ideal for:

- Families with two or more children requiring 1,100+ sqft layouts, as the 990-1023 sqft 3-bedroom units may feel constrained within 5-7 years as children age.

- Investors prioritising gross rental yields above 4%, as Core Central Region properties at this quantum typically deliver 2.5-3.5% yields in the current market.

- Buyers seeking short-term capital appreciation or planning to sell within 5-7 years, as the Q2 2030 TOP and 4-year SSD lock-in period extend the minimum holding horizon to mid-2034.

- Households sensitive to urban noise, particularly those with young children, given the approximately 710m proximity to Clarke Quay nightlife and weekend riverfront activity.

- First-time buyers with limited cash reserves below S$400K, as the S$1.388M studio quantum still requires S$350K in upfront capital and financing capacity for a 75% LTV loan.

- Drivers prioritising effortless expressway access, as River Valley Road congestion during peak hours introduces friction for daily commutes despite strong MRT redundancy.

Review Date: March 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This review is based on publicly available data and official URA transaction records. It is not financial advice. Verify all details with the developer before making purchase decisions.