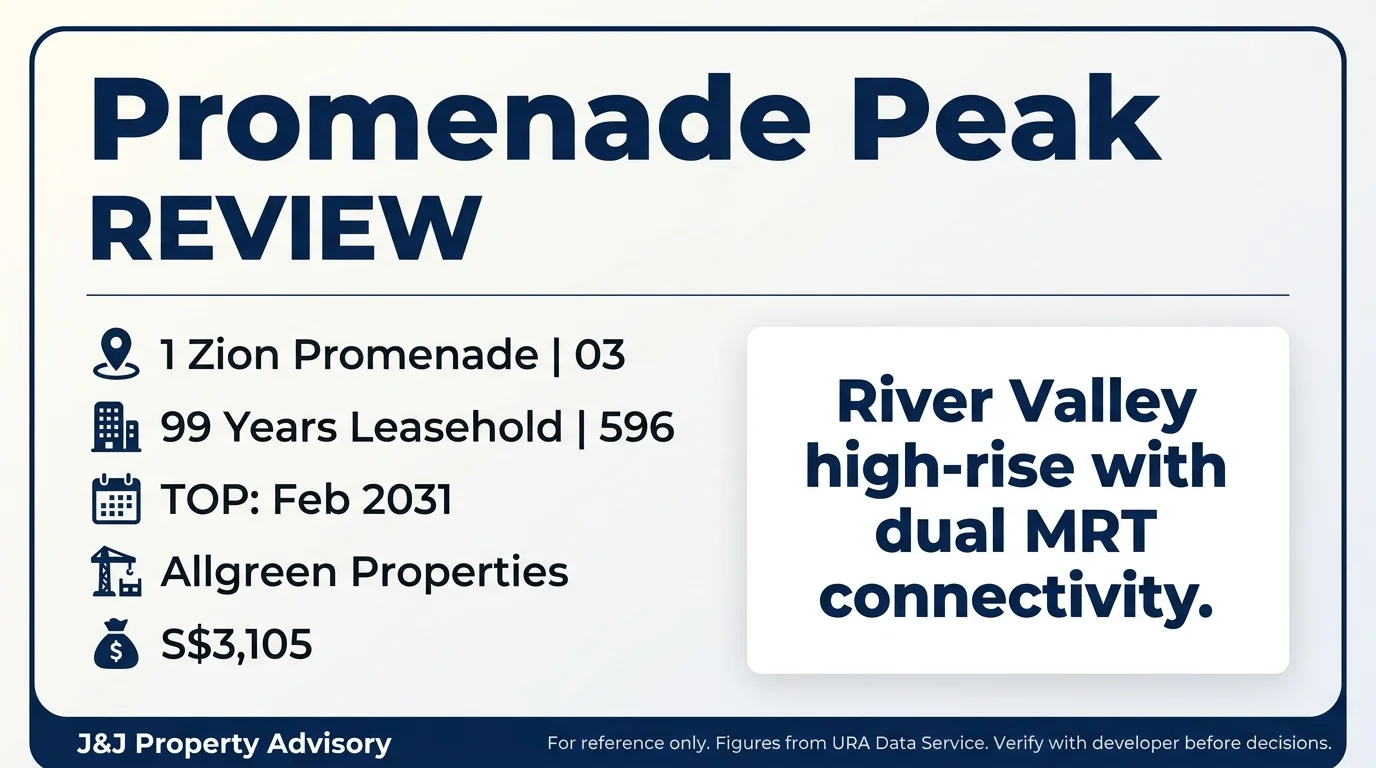

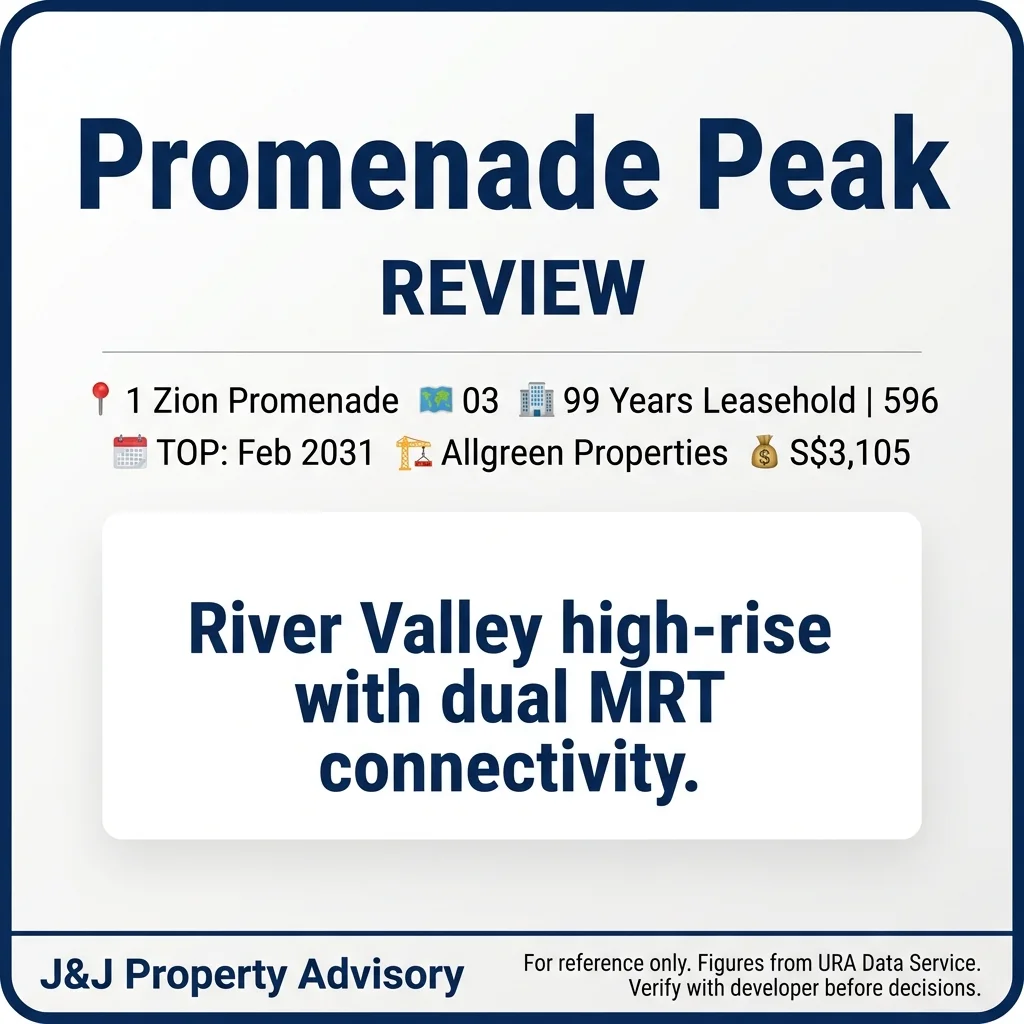

Project Snapshot

| Attribute | Details |

| Site Area | 99,952.5 sqft / 9,285.9 sqm |

| Developer | Allgreen Properties |

| Tenure | 99 Years Leasehold |

| Total Units | 596 |

| Units Sold | 388 (65.1% take-up) |

| Median PSF | S$3,105 |

| Land Cost PSF PPR | S$1,304 |

| Architect | DCA Architects |

Promenade Peak occupies a significant site in the River Valley precinct, positioned between the established Great World commercial node and the heritage Tiong Bahru neighbourhood. The development’s height and scale make it a visible landmark, with unobstructed sightlines to Marina Bay and the CBD. The land cost of S$1,304 PSF PPR reflects the premium attached to dual-MRT proximity on the Thomson-East Coast Line, which opened relatively recently and continues to drive residential demand in this corridor.

Location & Connectivity

1. Great World MRT (TE15) at approximately 180m

This is the primary transport node for residents, placing the development within a two-minute walk from a station on the Thomson-East Coast Line. TE15 connects directly to Orchard (TE14) in four minutes and Marina Bay (TE20) in approximately 12 minutes, making this a genuinely accessible location for CBD commuters. The station also integrates with Great World City shopping mall, providing covered access to dining, retail, and grocery options.

2. Havelock MRT (TE16) at approximately 310m

The second TEL station serves as a redundancy option and extends connectivity further south towards HarbourFront and Cantonment. While most residents will default to Great World station, the dual-station setup reduces crowding risk and offers alternative routing during peak hours or service disruptions. This level of MRT redundancy is uncommon in non-CBD locations and adds measurable convenience for daily commuting.

3. Tiong Bahru MRT (EW17) at approximately 890m

The East-West Line station extends cross-island connectivity, though the 890m distance makes this a secondary option for most residents. Access to EW17 is useful for commutes to Jurong East, Buona Vista, and western destinations without requiring a transfer at Orchard or Outram Park. The walk is manageable but less practical than the TEL stations for daily use.

4. River Valley Primary School at approximately 430m and Alexandra Primary School at approximately 990m

River Valley Primary is within a seven-minute walk, making it accessible for families prioritising proximity without requiring MOE’s 1km priority registration advantage. Alexandra Primary sits just under 1km, which places it within Phase 2B eligibility range but does not guarantee placement in competitive years. Neither school operates a GEP programme, which limits appeal for families specifically targeting gifted education pathways.

5. Great World City at approximately 250m, Valley Point at approximately 700m, Tiong Bahru Plaza at approximately 890m

Great World City anchors daily convenience, offering Cold Storage supermarket, food court options, and mid-range retail. Valley Point provides alternative dining and Cold Storage access, while Tiong Bahru Plaza serves the HDB heartland with more budget-oriented F&B and services. The cluster provides sufficient variety for everyday needs without requiring a car or extended travel.

6. Expressway access via River Valley Road and Clemenceau Avenue

The Central Expressway (CTE) is accessible within five minutes via River Valley Road, connecting to the Pan-Island Expressway (PIE) and Seletar Expressway (SLE) for cross-island travel. The Ayer Rajah Expressway (AYE) is reachable via Clemenceau Avenue and Havelock Road, though peak-hour congestion near the CBD fringe is common. Drivers benefit from proximity to arterial routes, but MRT dependency is higher here than in outer suburbs.

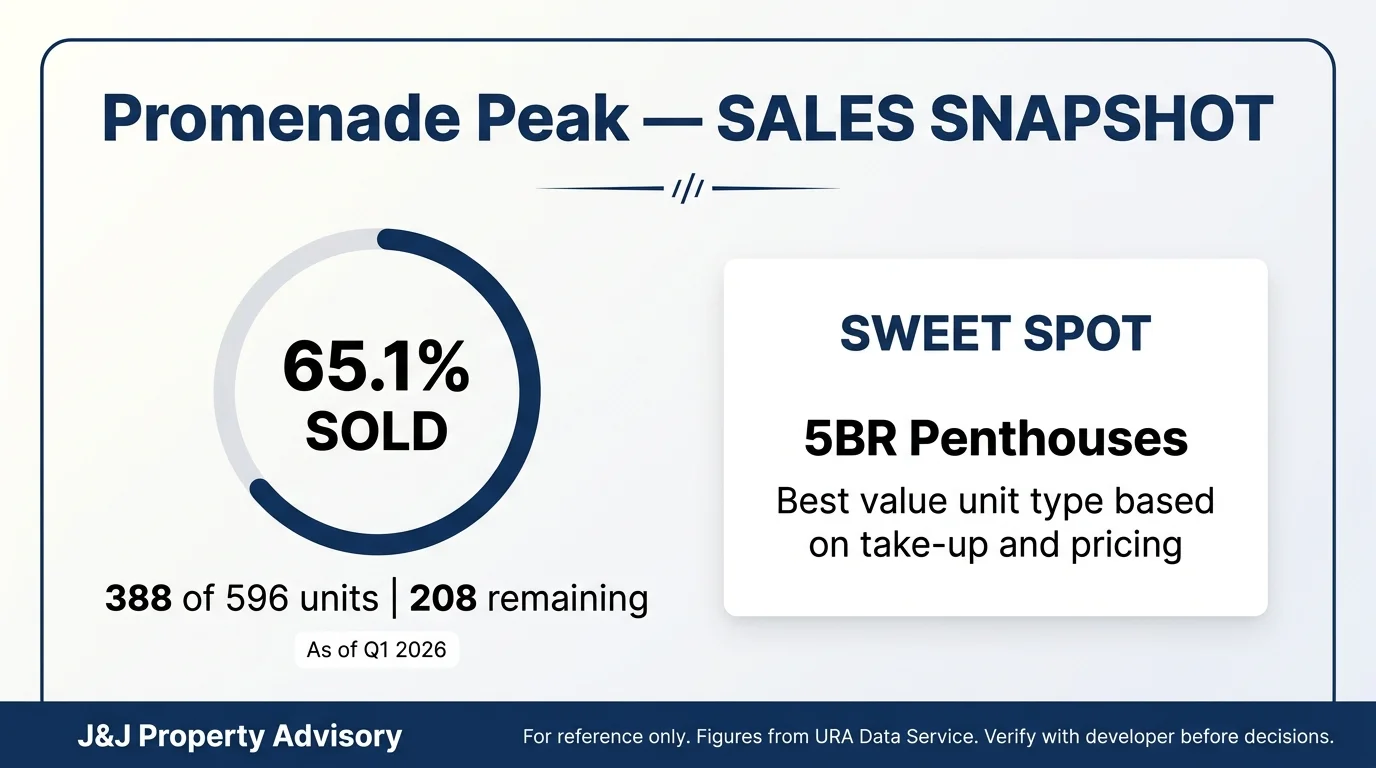

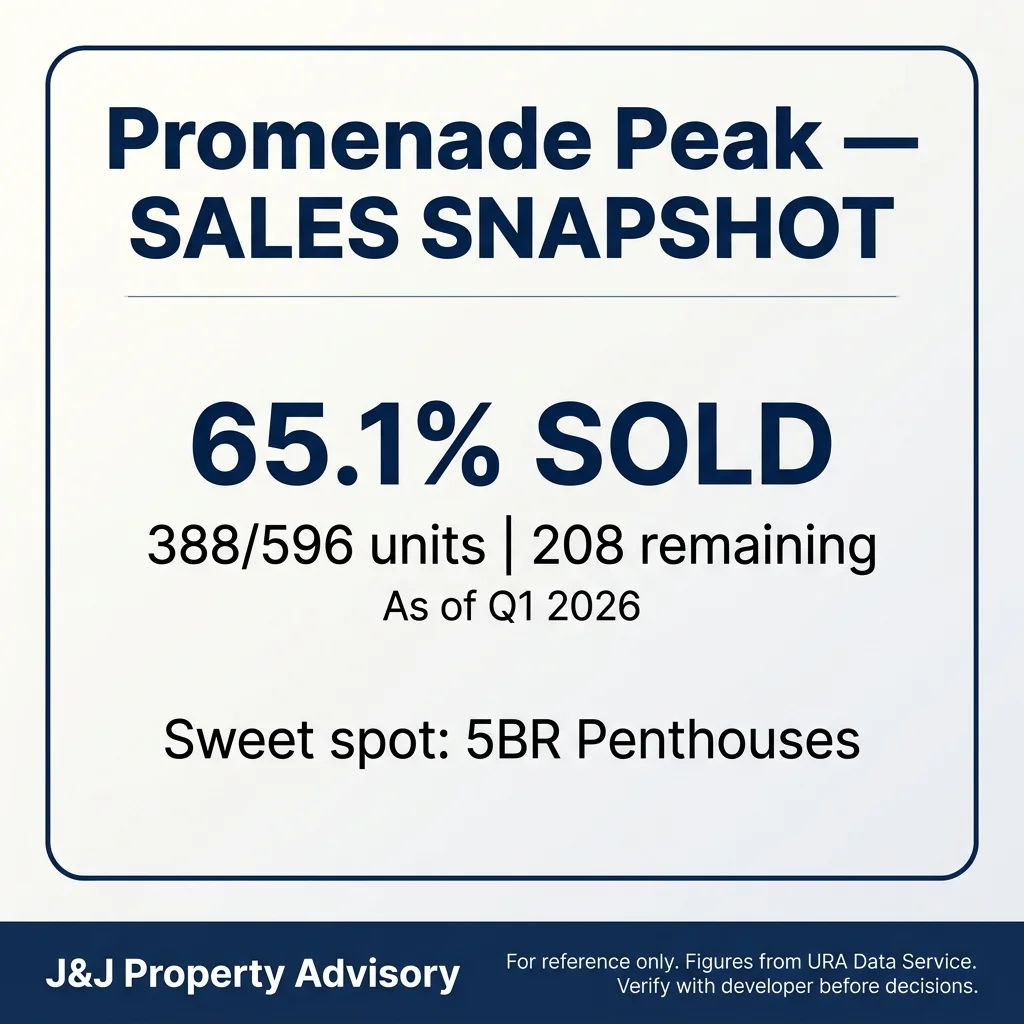

Sales Performance

| Metric | Figure |

| Units Sold | 388 / 596 (65.1%) |

| Median PSF | S$3,105 |

| PSF Range | S$2,927 – S$3,124 |

| Avg Monthly Sales | 23.5 units/month |

| District 03 Median PSF | S$2,727 |

| Premium to District | +13.9% |

Promenade Peak achieved a 65.1% take-up rate as of Q1 2026, selling 388 out of 596 launched units since its August 2025 launch. This translates to approximately 23.5 units per month across three quarters, which reflects steady absorption rather than a rapid sellout. The median transacted PSF of S$3,105 sits 13.9% above the District 03 median of S$2,727, positioning the project at the upper end of the district’s pricing spectrum alongside other recent TEL-adjacent launches.

The PSF range of S$2,927 to S$3,124 shows relatively tight clustering, indicating consistent pricing discipline from the developer without significant discounting pressure. The 208 remaining units suggest inventory for selective buyers, though the pace indicates the project is not struggling. Compared to the district median, Promenade Peak commands a clear premium, justified by its MRT proximity and newness but requiring buyers to accept leasehold depreciation risk over freehold alternatives.

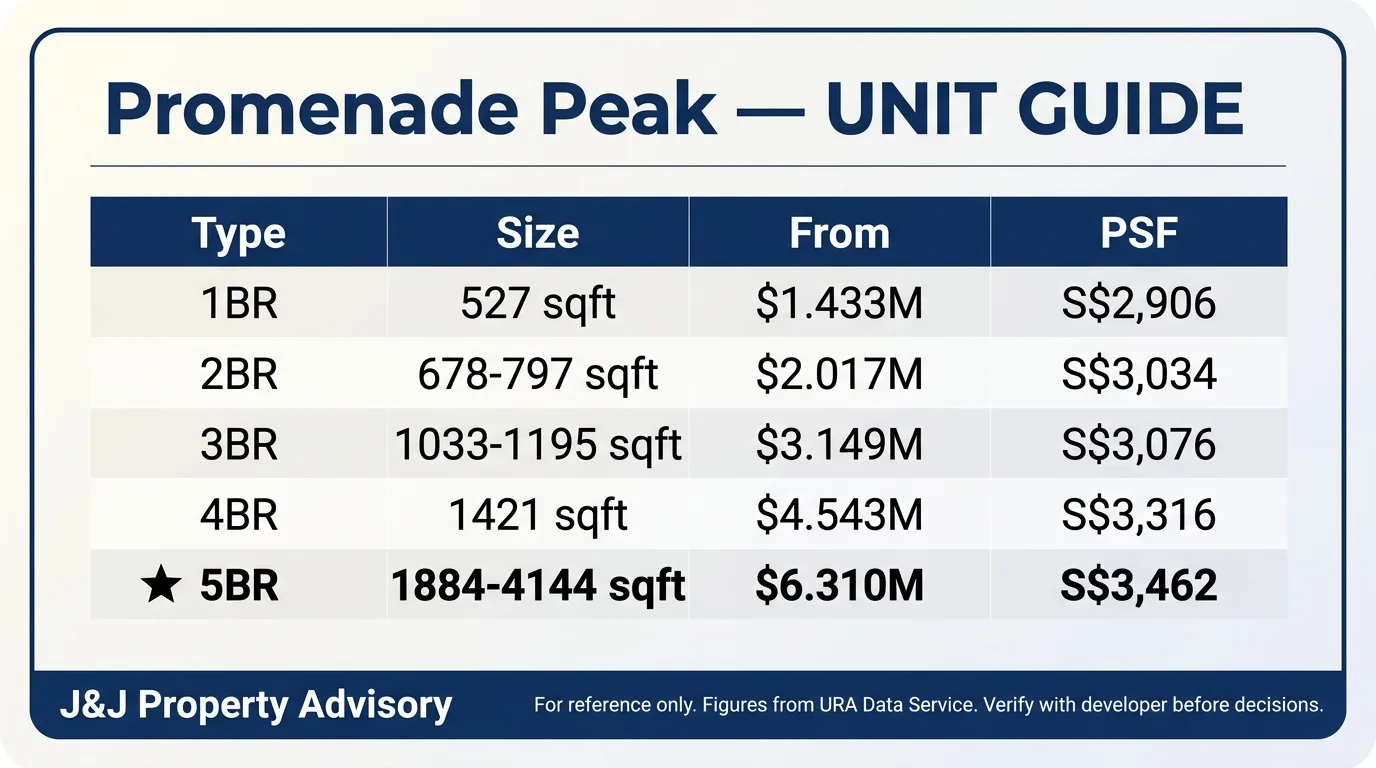

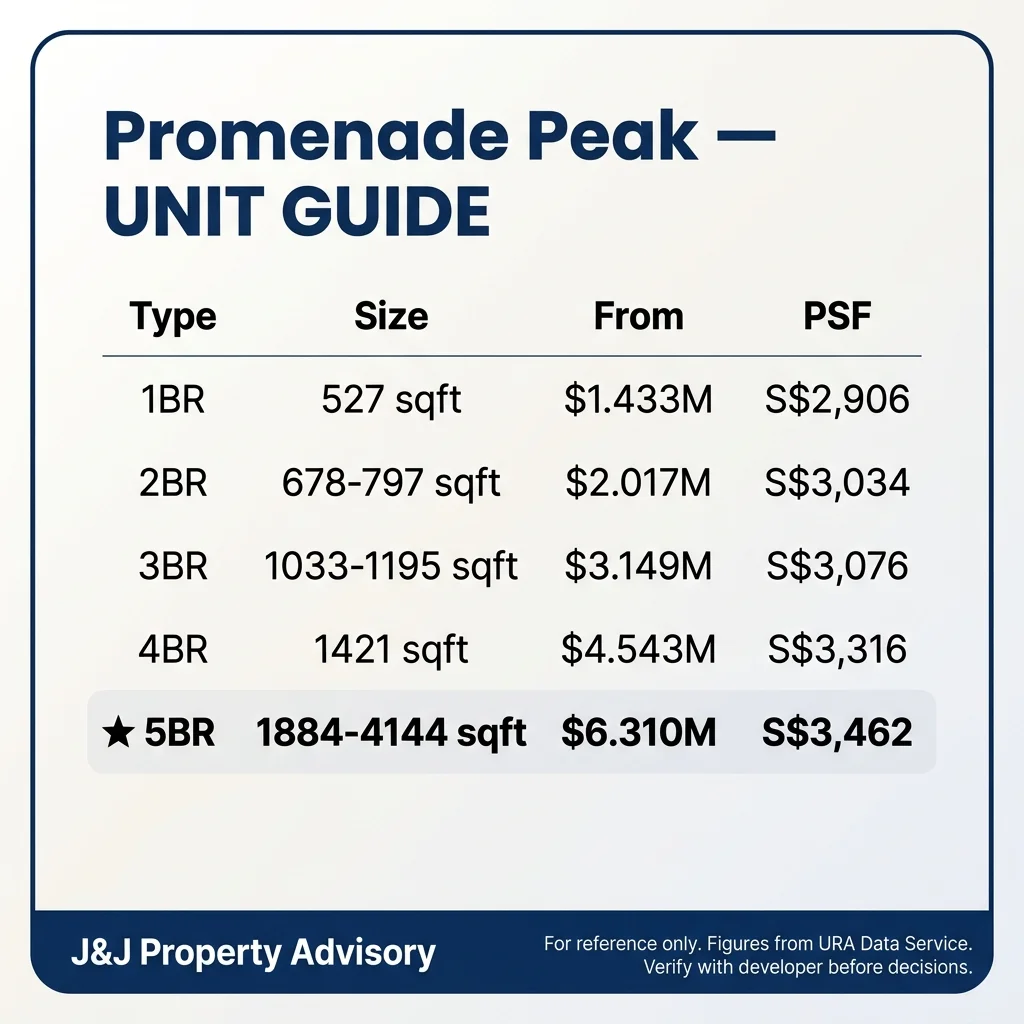

Unit Mix & Pricing

| Type | Size Range | Quantum From | PSF From | Units |

| 1BR | 527 sqft | S$1.433M | S$2,906 | 40 |

| 2BR | 678–797 sqft | S$2.017M | S$3,034 | 87 |

| 3BR | 1,033–1,195 sqft | S$3.149M | S$3,076 | 13 |

| 4BR | 1,421 sqft | S$4.543M | S$3,316 | 20 |

| 5BR | 1,884–4,144 sqft | S$6.310M | S$3,462 | 15 |

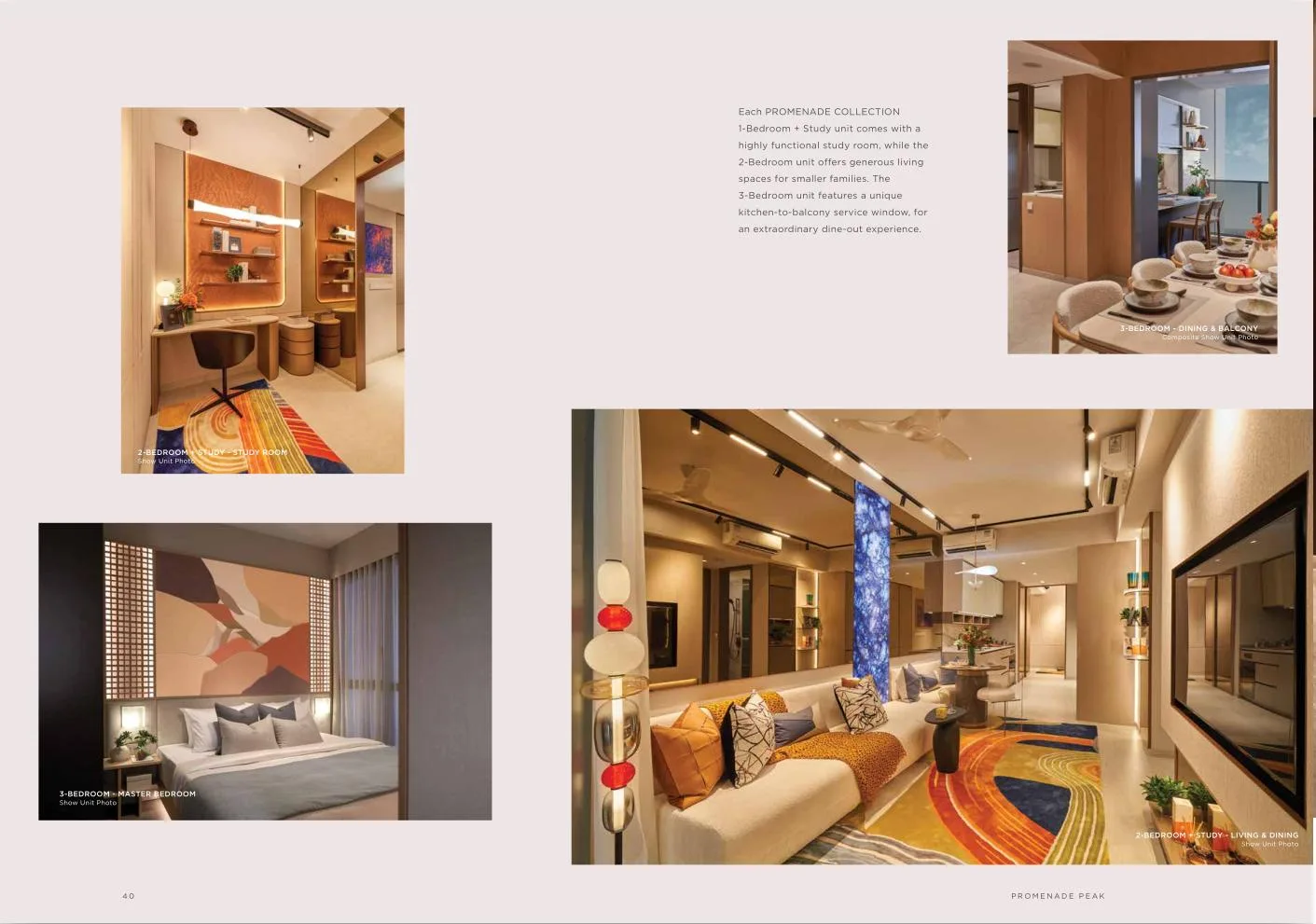

The unit mix skews heavily toward compact types, with only 13 three-bedroom units and 20 four-bedroom units out of 596 total. This reflects the developer’s bet on investor-landlord demand and DINK/expat couples rather than large family owner-occupiers. The 1BR quantum of S$1.433M positions it within reach of first-time buyers with substantial CPF and cash, though the leasehold tenure limits long-term holding appeal compared to older, cheaper resale alternatives.

The PSF premium increases sharply with bedroom count, rising from S$2,906 for 1BR to S$3,462 for 5BR penthouses. This gradient suggests the developer priced larger units aggressively to capture lifestyle buyers willing to pay for space and views. The 5BR range extends to 4,144 sqft, which is unusually large for a high-rise and targets ultra-high-net-worth buyers seeking landed-style space without the maintenance burden.

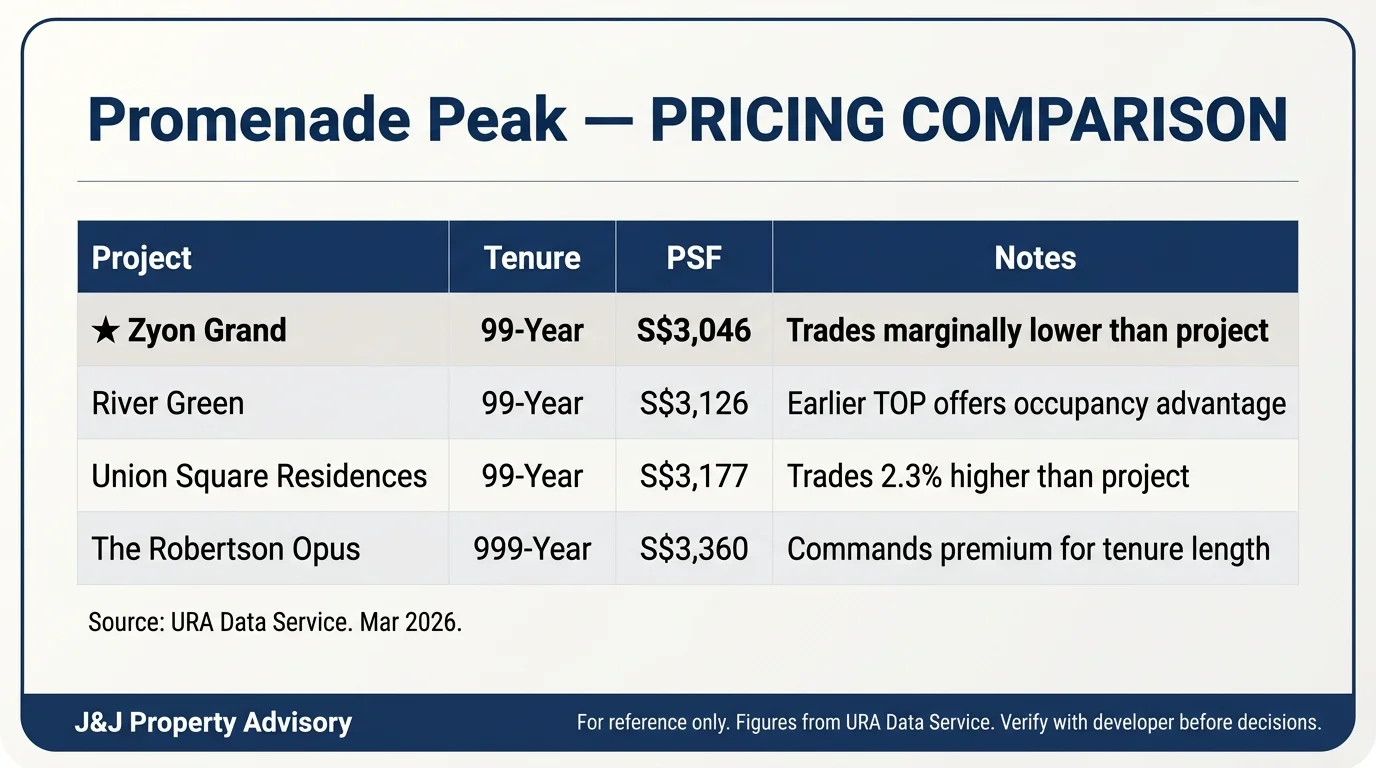

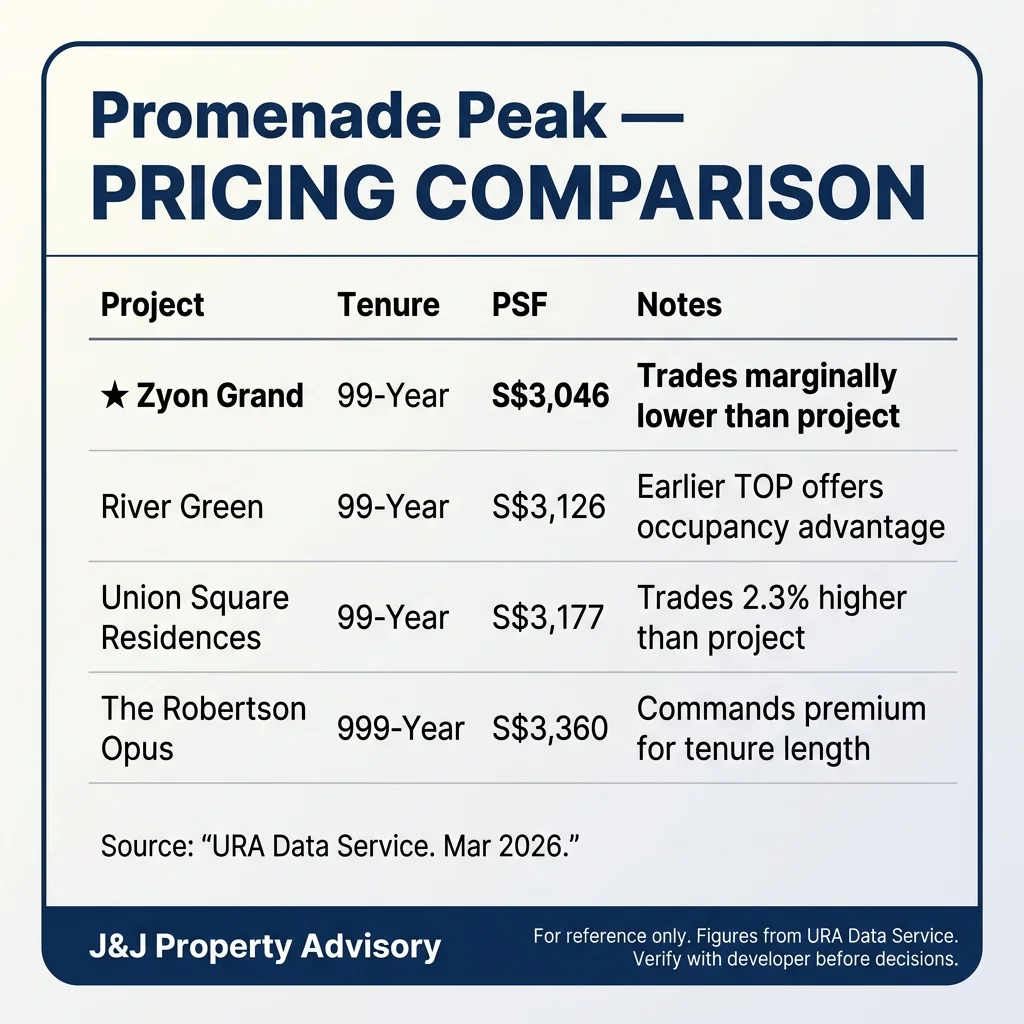

Comparables

| Project | Median PSF | Transactions | Tenure | Expected TOP |

| Promenade Peak | S$3,105 | 388 | 99-Year Leasehold | Feb 2031 |

| Zyon Grand | S$3,046 | 618 | 99-Year Leasehold | Sep 2032 |

| River Green | S$3,126 | 483 | 99-Year Leasehold | Q1 2029 |

| Union Square Residences | S$3,177 | 138 | 99-Year Leasehold | Q1 2029 |

| The Robertson Opus | S$3,360 | 200 | 999-Year Leasehold | Q2 2030 |

Promenade Peak trades in line with recent leasehold comparables, sitting marginally above Zyon Grand and marginally below River Green. The tight PSF clustering among these four projects reflects the market’s current pricing consensus for new TEL-adjacent developments in District 03. The Robertson Opus commands an 8.2% premium over Promenade Peak, attributable entirely to its 999-year tenure, which functionally behaves as freehold for resale and estate planning purposes.

River Green’s earlier TOP (Q1 2029 versus Feb 2031) offers a two-year occupancy advantage, which may appeal to buyers prioritising faster rental income or own-stay timelines. Union Square Residences shares the same Q1 2029 TOP and trades 2.3% higher than Promenade Peak, though its smaller transaction sample (138 versus 388) suggests less liquidity and potentially more selective buyer targeting. For buyers comparing within this peer group, the key differentiators are tenure length, TOP timing, and specific location trade-offs rather than meaningful pricing gaps.

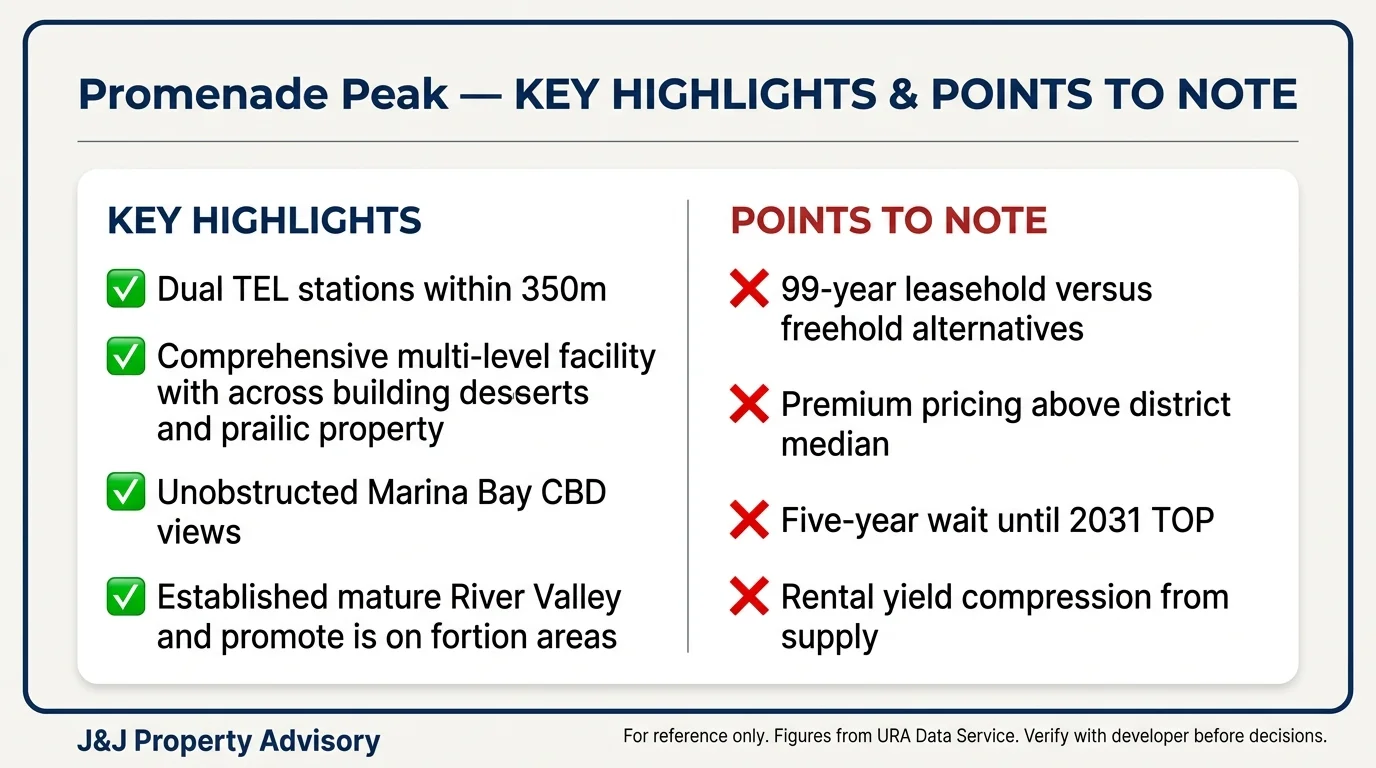

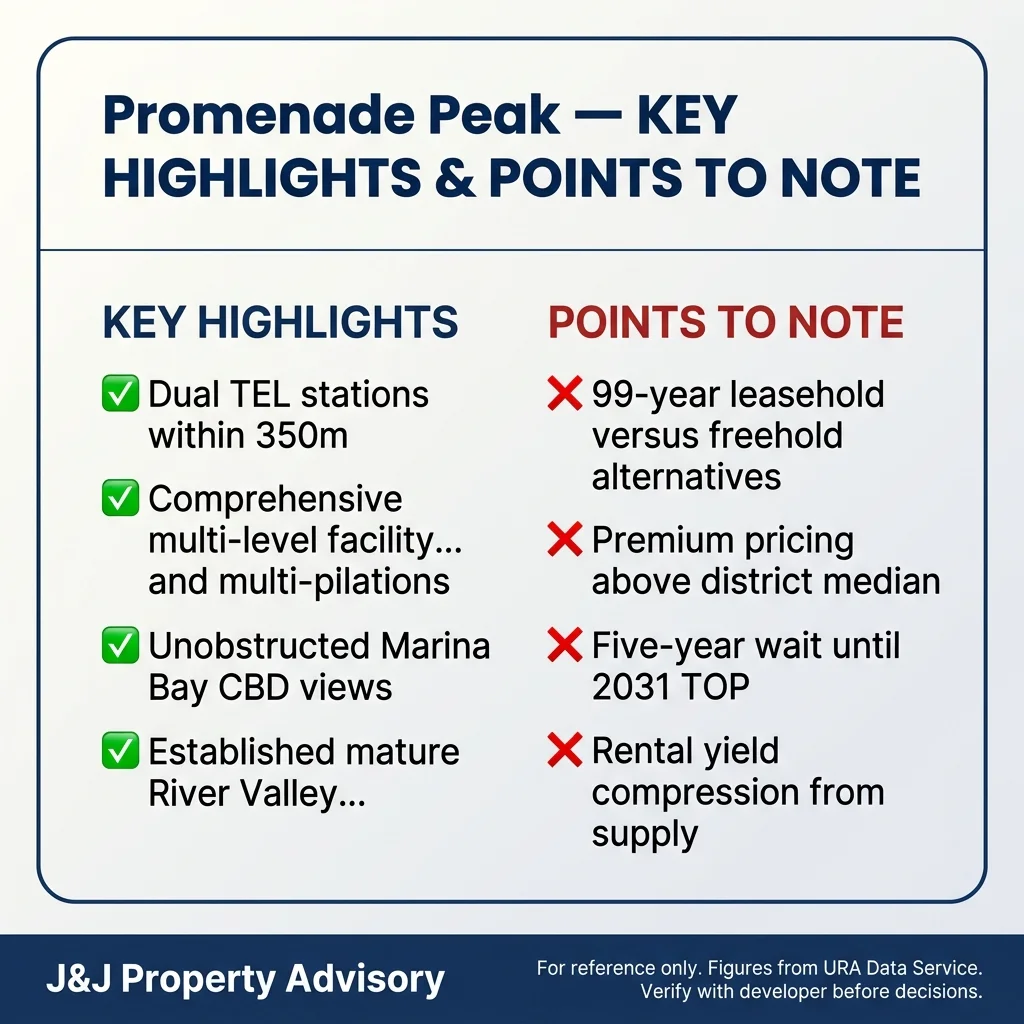

Key Strengths

Dual TEL station access within 200-350m

Great World (TE15) at approximately 180m and Havelock (TE16) at approximately 310m provide exceptional redundancy and route flexibility. This setup rivals Orchard-Somerset dual-station configurations and eliminates single-point-of-failure risk during MRT disruptions. For CBD commuters, the sub-10-minute travel time to Shenton Way or Raffles Place via one or two stops is a tangible daily time saving compared to bus-dependent or car-reliant alternatives.

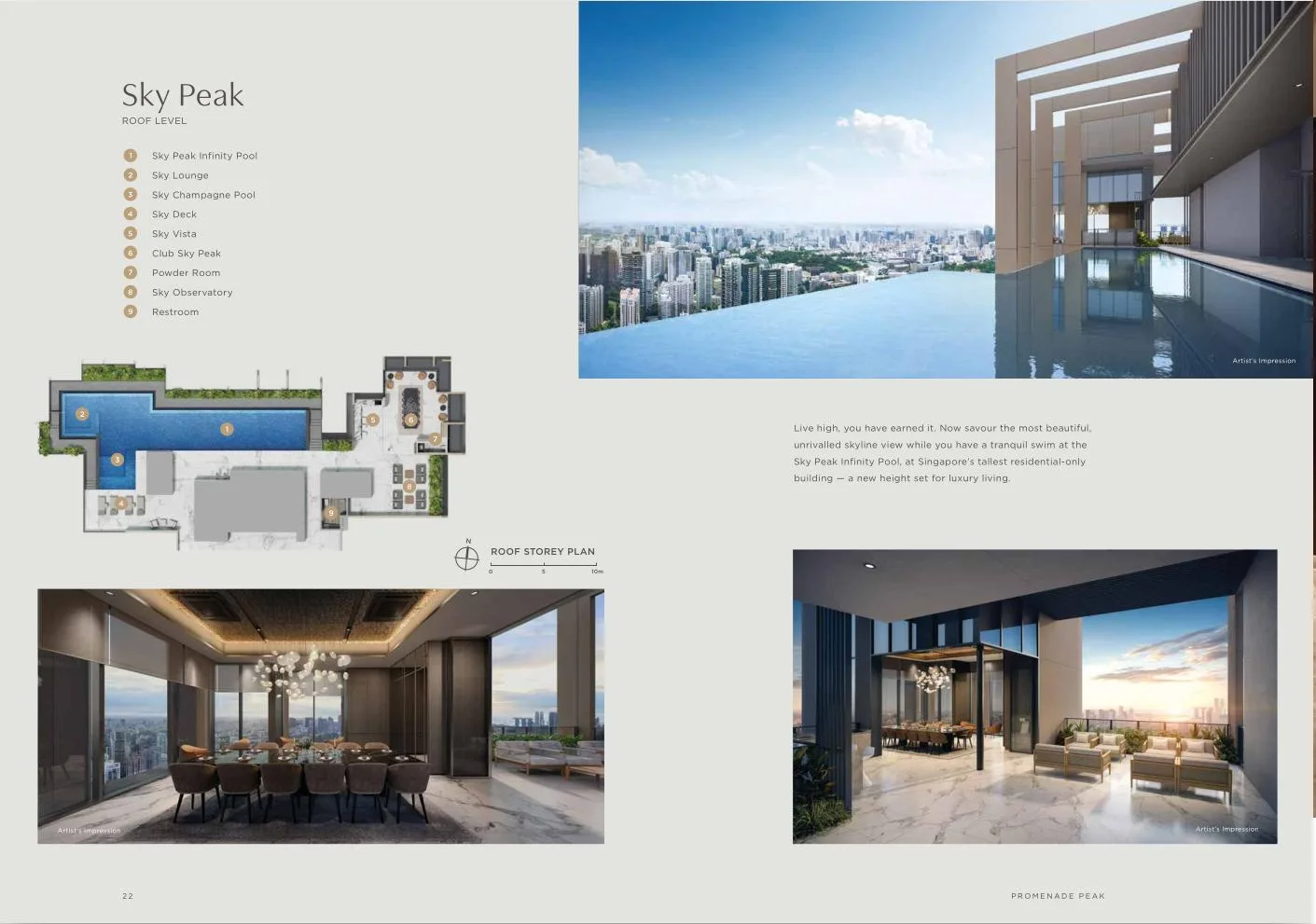

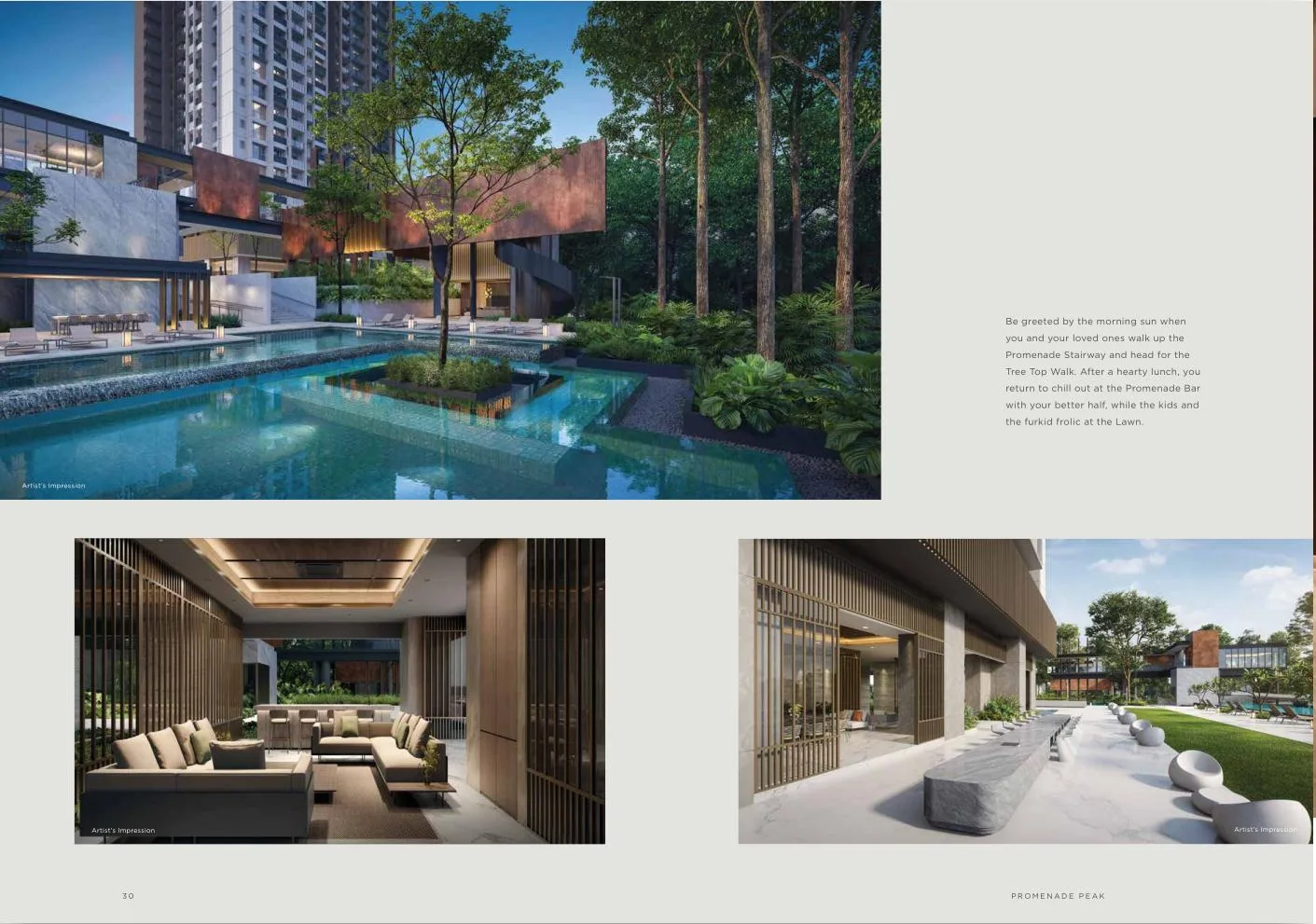

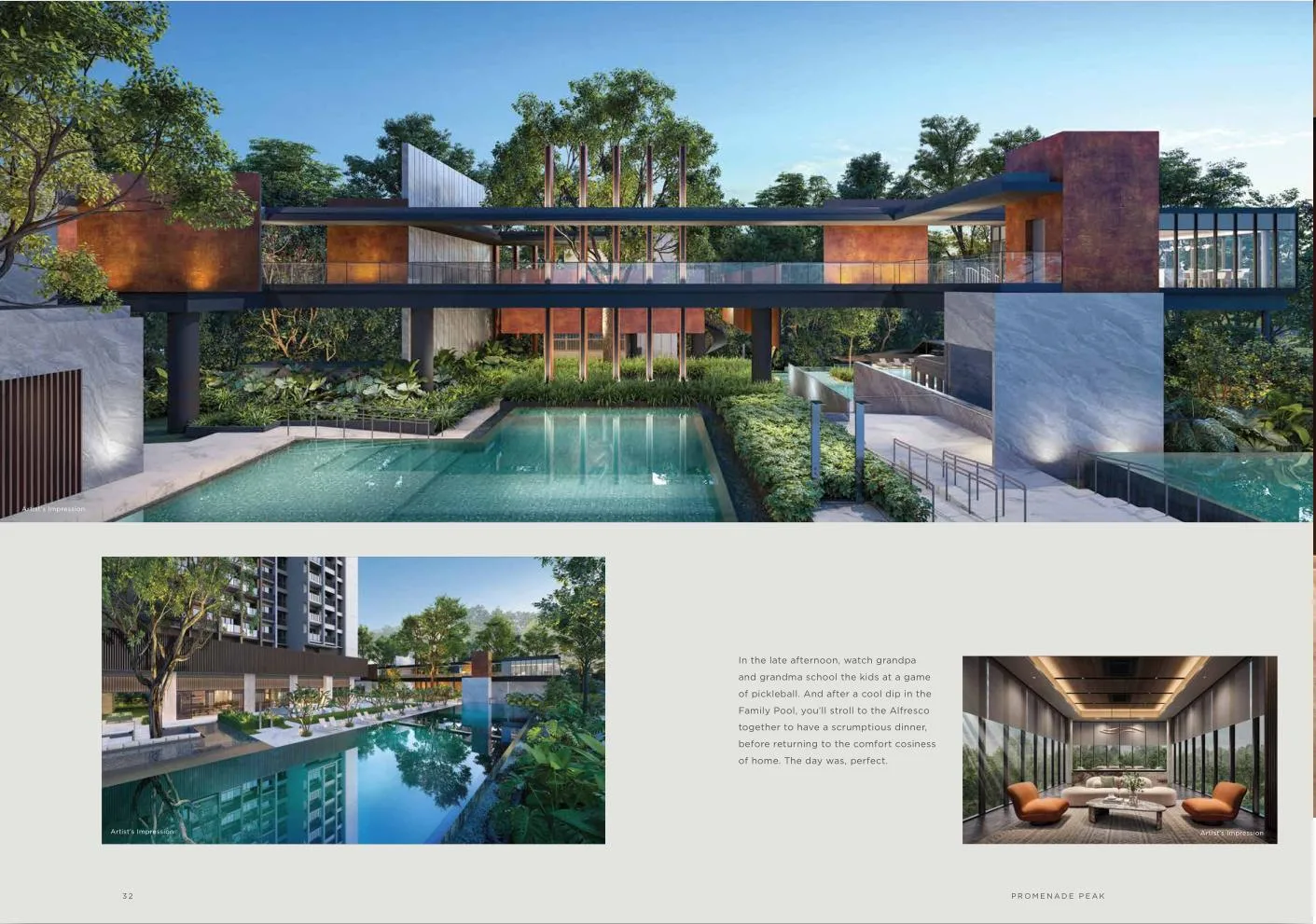

Comprehensive facility spread across multiple dedicated levels

The development allocates separate floors for ground-level recreation, mid-level co-working and social spaces, a dedicated wellness floor, and a rooftop sky lounge. This vertical segregation reduces crowding at individual facility zones and provides functional variety that matches larger 800-unit developments. The inclusion of hydrotherapy facilities and smart home integration reflects above-average capital expenditure on amenities, which should translate to lower depreciation in facility quality over the first decade post-TOP.

High-floor units with unobstructed Marina Bay and CBD views

The development’s height ensures upper-tier units face minimal future obstruction risk from surrounding low-rise heritage shophouses and conservation areas. Buyers in stacks facing southeast capture Marina Bay Sands, the Flyer, and the financial district skyline, which historically commands a 10-15% resale premium in comparable projects. The views are not replicable in lower-density developments and represent a permanent locational advantage.

Established neighbourhood with mature infrastructure

River Valley and Tiong Bahru are fully built-out precincts with stable traffic patterns, complete utility networks, and predictable noise profiles. Unlike emerging growth corridors with ongoing MRT construction or future highway extensions, this location offers certainty on what the living environment will look and feel like post-TOP. For risk-averse buyers, this eliminates speculative assumptions about future neighbourhood development.

Allgreen’s 53-project track record and Kuok Group backing

Allgreen has delivered approximately 11,000 residential units across 53 projects since the 1980s, with zero major defect scandals or unfinished projects in its history. The Kuok Group’s financial depth provides confidence in on-time TOP delivery and adequate defect rectification budgets. While track record does not guarantee resale performance, it does reduce execution risk for buyers holding through to completion.

Points to Watch

99-year leasehold versus freehold alternatives in the same district

The Robertson Opus’s 999-year tenure trades 8.2% higher than Promenade Peak, quantifying the market’s current discount for leasehold holdings. Over a 20-year hold period, leasehold depreciation accelerates as the remaining tenure drops below 80 years, which historically triggers sharper PSF declines in resale transactions. Buyers planning multi-decade holds should model the effective annual depreciation cost, which compounds more aggressively in the final third of the lease.

Premium pricing 13.9% above District 03 median

The S$3,105 median PSF requires buyers to accept a material premium over the district average of S$2,727, which includes older but freehold stock in the same vicinity. If the next market downturn compresses pricing, newer leasehold projects typically retract faster than established freehold alternatives due to overleveraged investor-landlords liquidating at a loss. The premium is defensible for own-stay buyers prioritising newness and facilities, but represents heightened volatility risk for short-term flippers.

February 2031 TOP with five-year wait from launch

Buyers purchasing in 2026 face a five-year wait before occupancy, during which interest rate changes, economic cycles, and oversupply risk can materially shift resale pricing. The TEL corridor has multiple competing launches scheduled between now and 2030, which may saturate demand and compress rental yields upon TOP. Buyers financing with significant cash components face opportunity cost risk if alternative investments outperform over the holding period.

Limited larger units with only 13 three-bedroom and 20 four-bedroom flats

The scarcity of family-sized units reduces appeal for buyers seeking long-term own-stay in a growing household. The 87 two-bedroom units will compete with resale alternatives when current owners upsize, creating potential liquidity friction in the secondary market. Families targeting this development should secure larger units early, as future resale availability will be constrained by the small absolute unit count.

River Valley Primary School outside 1km priority registration range

The approximately 430m distance to River Valley Primary does not confer Phase 2A(2) 1km priority, leaving buyers reliant on Phase 2B or 2C balloting in competitive years. Alexandra Primary sits just under 1km at approximately 990m, which falls within Phase 2B but offers no guarantee of placement. Families prioritising guaranteed school access should verify exact measured distances from their specific unit block and consider backup options in neighbouring districts.

Rental yield compression risk from 596-unit supply hitting market simultaneously

When the project TOPs in February 2031, investor-landlords across 596 units will list rental inventory within a narrow timeframe, creating temporary oversupply in the River Valley rental submarket. This phenomenon historically depresses first-year rental yields by 5-10% compared to steady-state levels as landlords compete for tenants. Buyers banking on immediate positive cash flow post-TOP should model conservative rental assumptions and factor in potential void periods during the initial leasing phase.

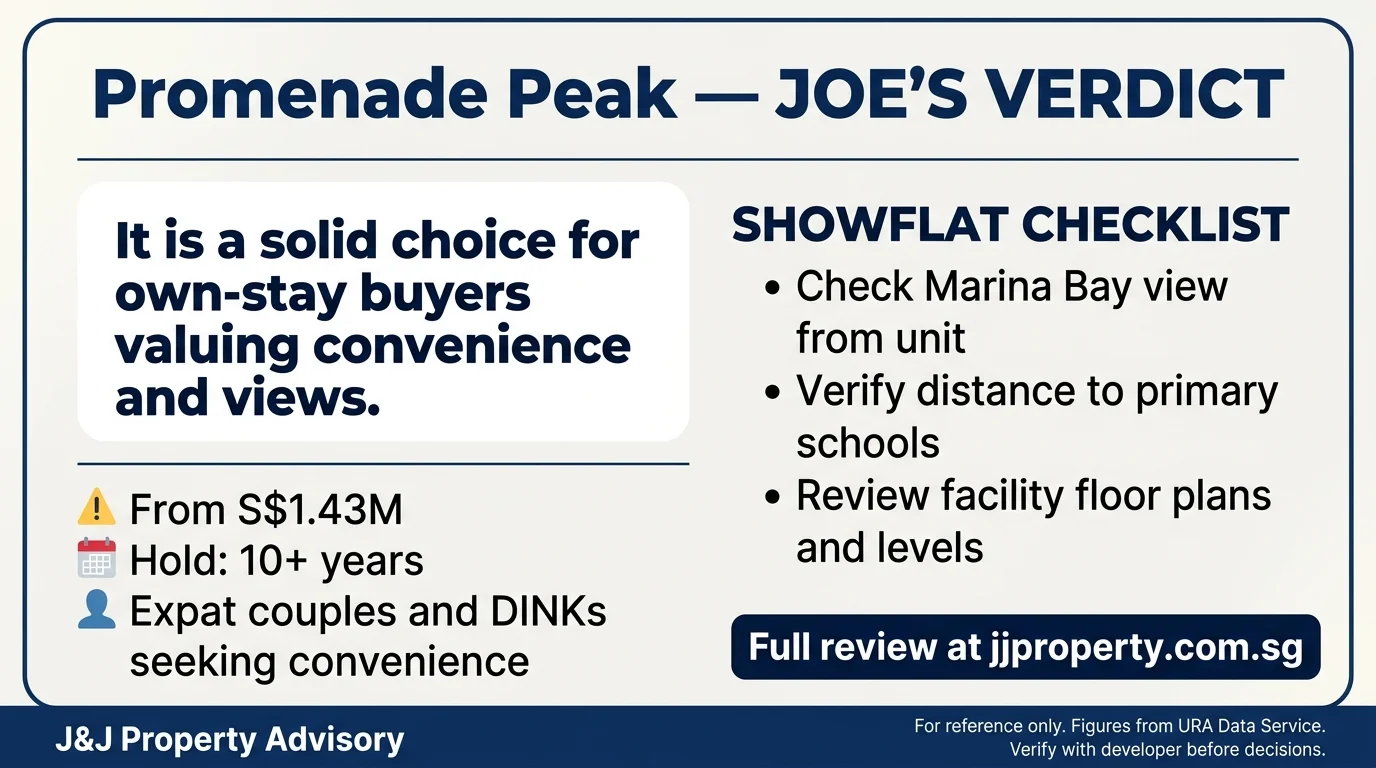

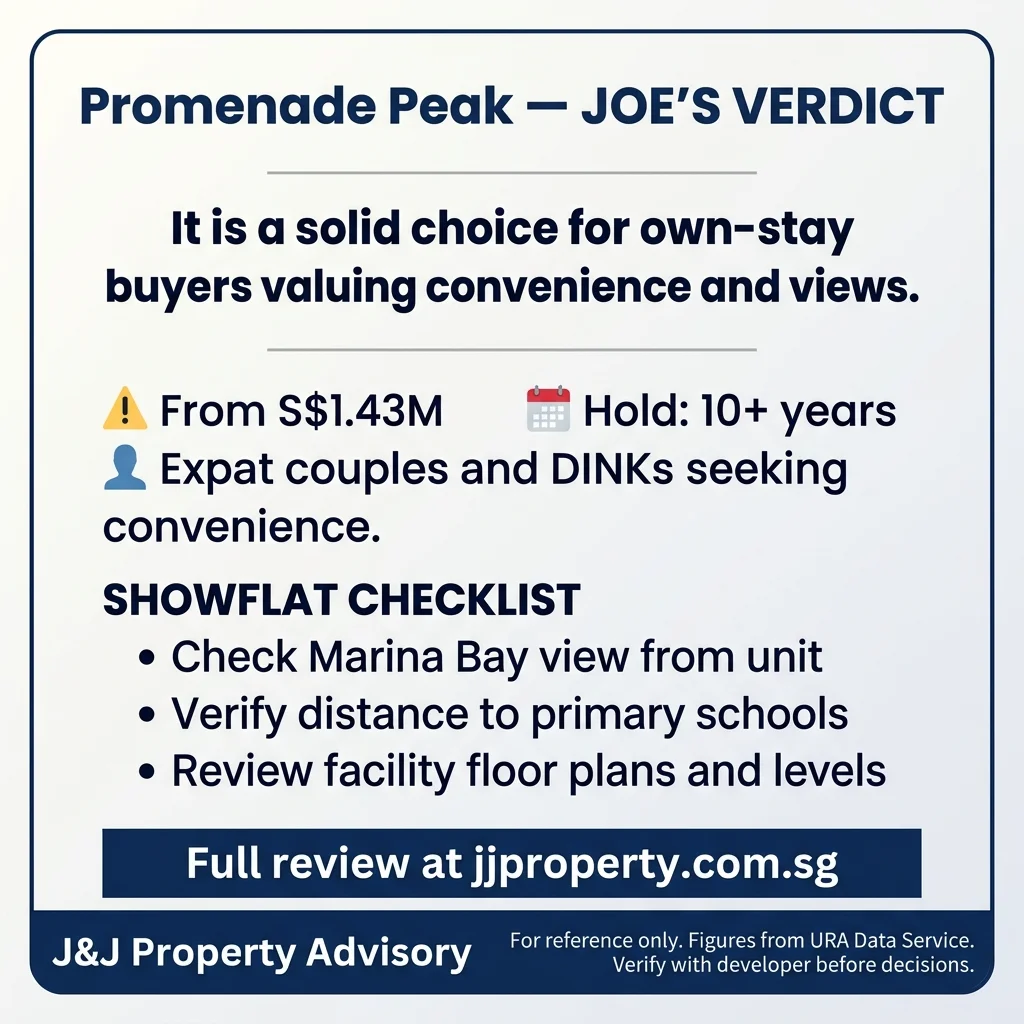

Bottom Line

Promenade Peak delivers on the fundamentals that matter for River Valley own-stay buyers: sub-200m MRT access, established neighbourhood infrastructure, and unobstructed high-floor views in a location that will not see further dramatic transformation. The 65.1% take-up rate and S$3,105 median PSF reflect steady market acceptance rather than speculative frenzy, which is appropriate given the leasehold tenure and premium pricing. For buyers who value immediate lifestyle benefits and can afford the 13.9% premium over district median, the project offers a defensible proposition, particularly for units facing Marina Bay with clear sightlines.

The case weakens for buyers sensitive to long-term capital appreciation or seeking school proximity advantages. The 99-year leasehold tenure will depreciate measurably faster than freehold comparables over a 15-20 year hold, and the lack of 1km school priority eliminates a key resale driver for family buyers. The five-year wait to TOP also introduces execution risk and opportunity cost, particularly if competing launches between now and 2031 compress pricing in the TEL corridor. Buyers should approach this as a lifestyle purchase rather than a capital growth vehicle, and model conservative resale assumptions accordingly.

For Own-Stay Buyers

If you prioritise Great World MRT access, unobstructed views, and a mature neighbourhood with predictable infrastructure, Promenade Peak offers a turnkey solution with minimal speculative risk on future development. The comprehensive facilities justify the premium for buyers who will actively use co-working spaces, wellness amenities, and rooftop social zones. Focus on higher-floor units facing southeast to maximise view retention and select larger bedroom counts early given the limited supply of 3BR and 4BR units. Accept the leasehold depreciation as the cost of locking in current pricing and location, and plan to hold through at least one full market cycle to recoup transaction costs.

For Investment Buyers

The rental yield case is weaker due to simultaneous TOP supply risk, premium entry pricing, and leasehold depreciation headwinds. The 1BR and 2BR units will attract tenant demand from Great World MRT proximity, but expect first-year rental competition and potential void periods as 596 units hit the market together. Model gross yields conservatively at 2.8-3.2% in the first two years post-TOP, rising to 3.5-3.8% once the initial glut clears. The investment thesis depends on TEL ridership growth and sustained CBD employment, both of which face uncertainty in a hybrid-work economy. Buyers seeking safer yield plays should compare against older freehold resale stock in the same district trading at lower PSF entry points with established rental track records.

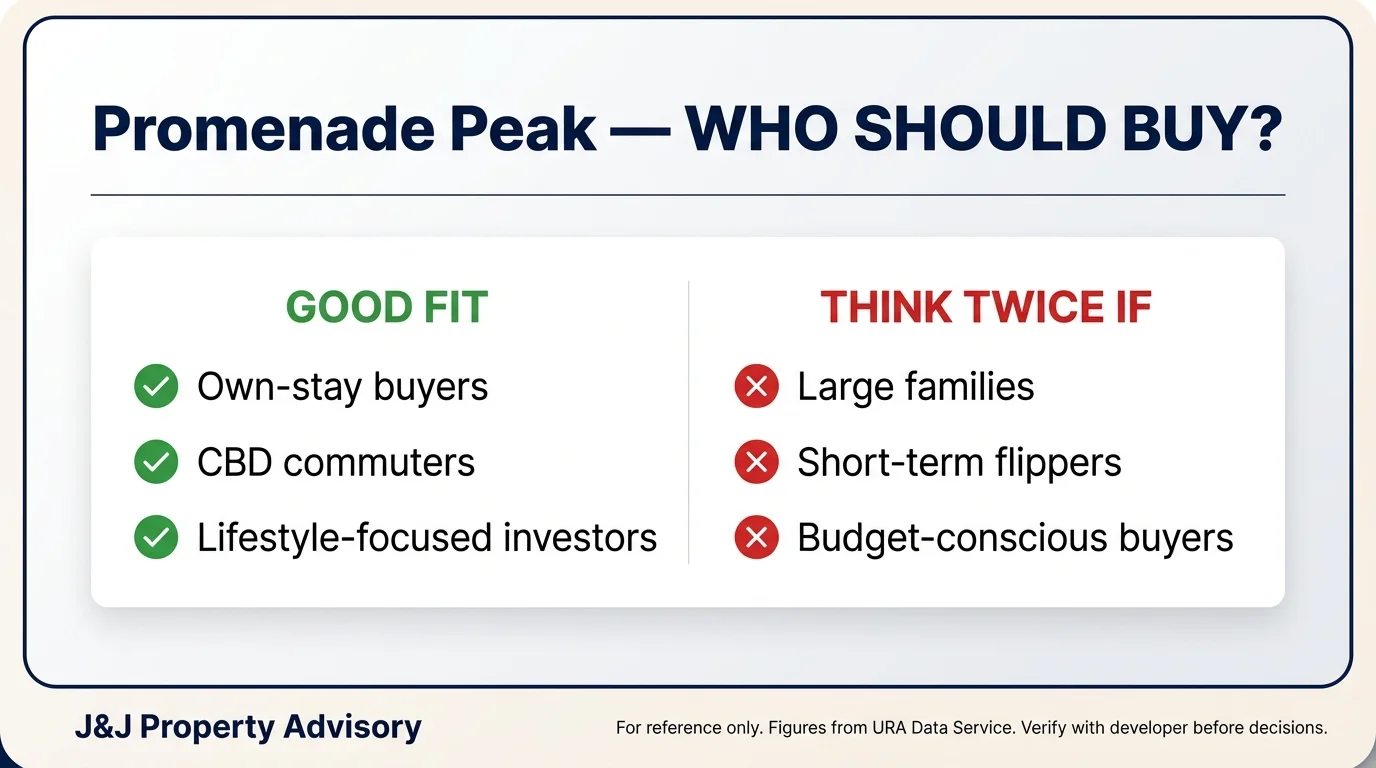

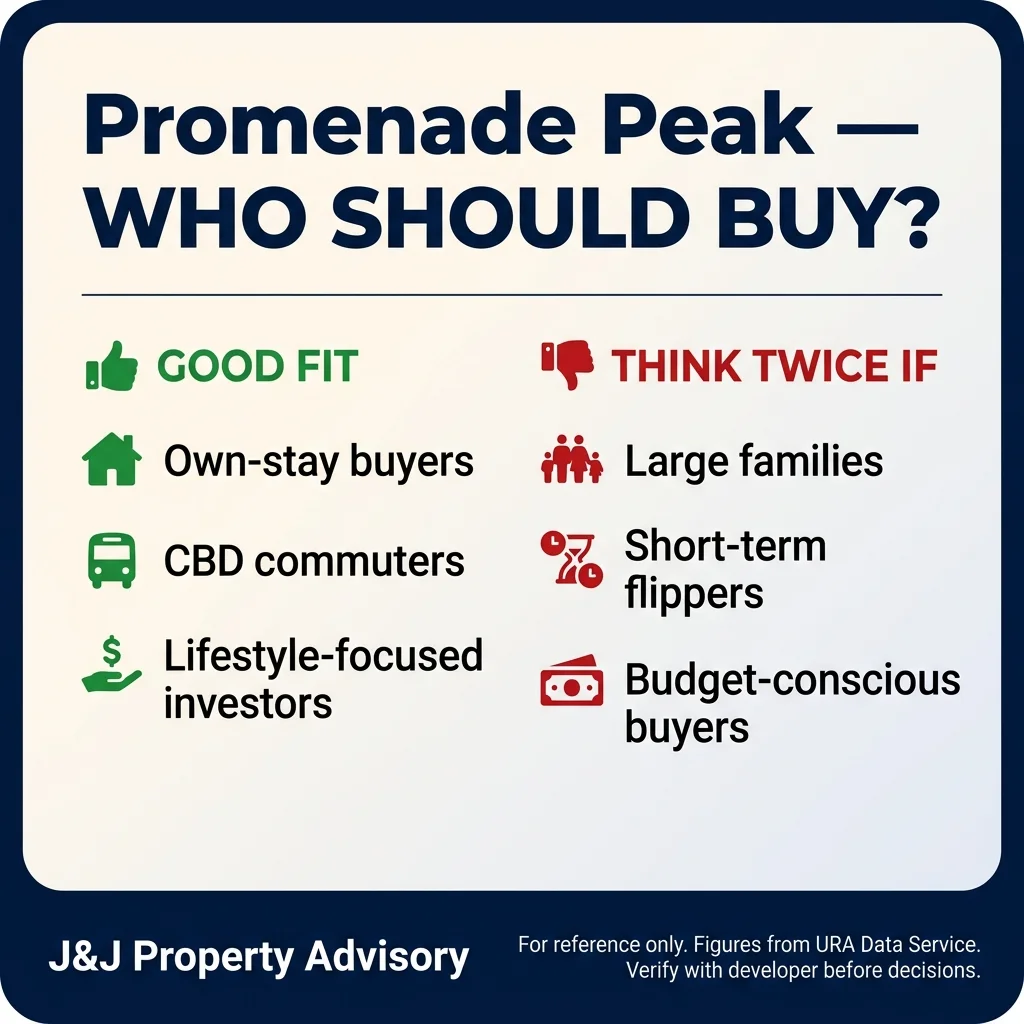

Who Is This For

Good fit:

- CBD professionals commuting to Shenton Way or Raffles Place via TEL, prioritising sub-10-minute train access over car dependency. The dual-station setup reduces commute variability and eliminates parking costs.

- DINK couples or small families comfortable with 2BR layouts in the 678-797 sqft range, targeting own-stay rather than future upsizing. The S$2.017M entry quantum is accessible with combined CPF and 20-25% cash equity.

- Expat tenants or relocating professionals seeking short-term (1-3 year) leases near Great World City, Orchard, and the CBD. The development’s newness and facilities will command premium rents from corporate relocations.

- Buyers prioritising immediate lifestyle amenities (co-working, hydrotherapy, sky lounge) over long-term capital appreciation. The facility investment justifies the premium for active users who will extract daily utility value.

- High-floor view buyers willing to pay for unobstructed Marina Bay and CBD skyline sightlines that will not be replicated in low-rise heritage zones. Units on floors 30+ facing southeast capture permanent view advantages.

- Buyers who prefer established, mature neighbourhoods with predictable infrastructure over emerging growth corridors with speculative upside. River Valley’s built-out character eliminates execution risk on future amenities.

Not ideal for:

- Families requiring guaranteed 1km school priority for River Valley Primary or Alexandra Primary. Both schools fall outside or at the edge of 1km eligibility, forcing reliance on Phase 2B/2C balloting.

- Buyers targeting long-term (20+ year) holds prioritising freehold tenure and minimal lease decay. The 99-year leasehold will depreciate measurably faster than 999-year or freehold alternatives in resale transactions.

- Investors seeking immediate positive cash flow post-TOP without void period risk. The 596-unit simultaneous supply will compress first-year rental yields and increase tenant competition.

- Value-conscious buyers unwilling to pay 13.9% above District 03 median PSF for newness and facilities. Older resale freehold stock offers better entry pricing for buyers prioritising affordability.

- Families needing 3BR or larger units with multiple layout options. Only 13 three-bedroom and 20 four-bedroom units limit selection and future resale liquidity for upsizers.

- Buyers requiring TOP within 1-2 years for immediate occupancy or rental income. The February 2031 completion involves a five-year wait with attendant market cycle and interest rate risk.

Review Date: March 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This review is based on publicly available data and official URA transaction records. It is not financial advice. Verify all details with the developer before making purchase decisions.