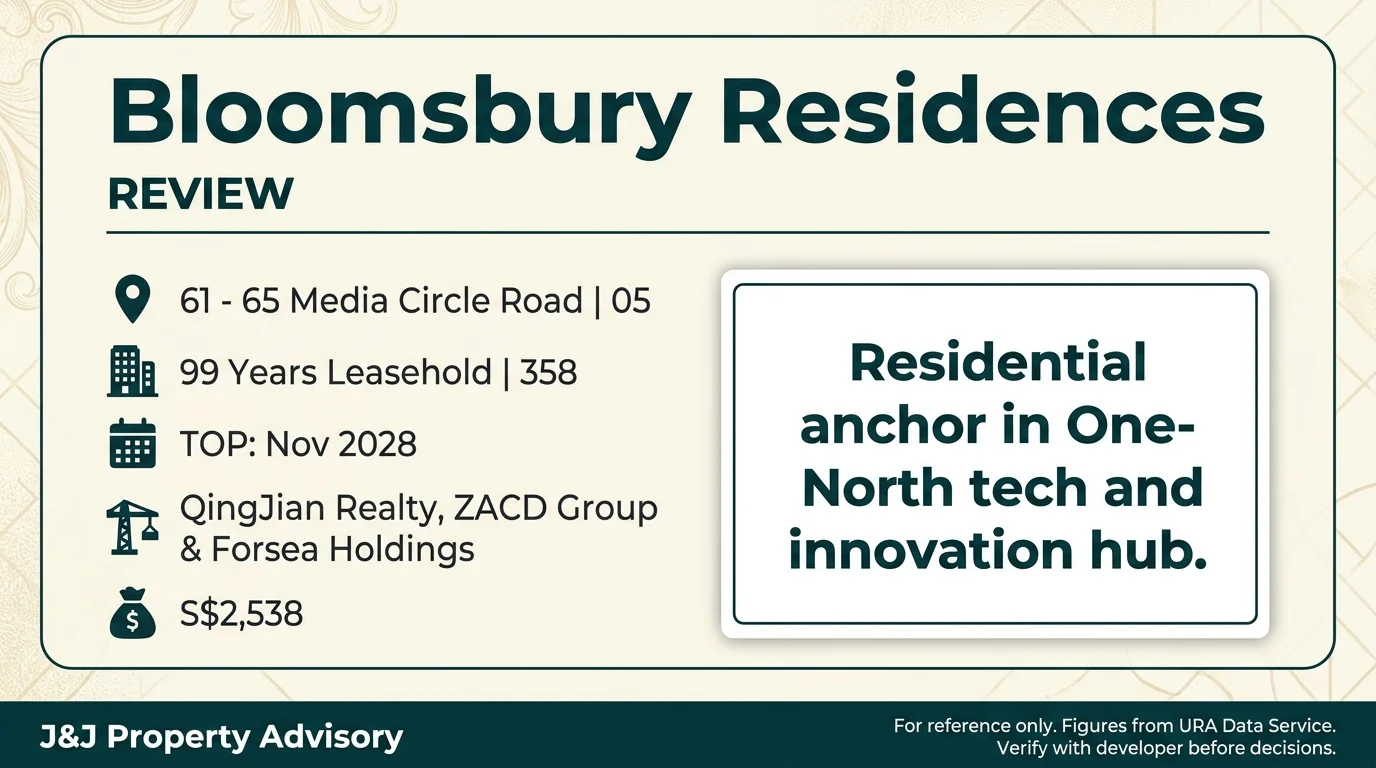

Launched Analysis

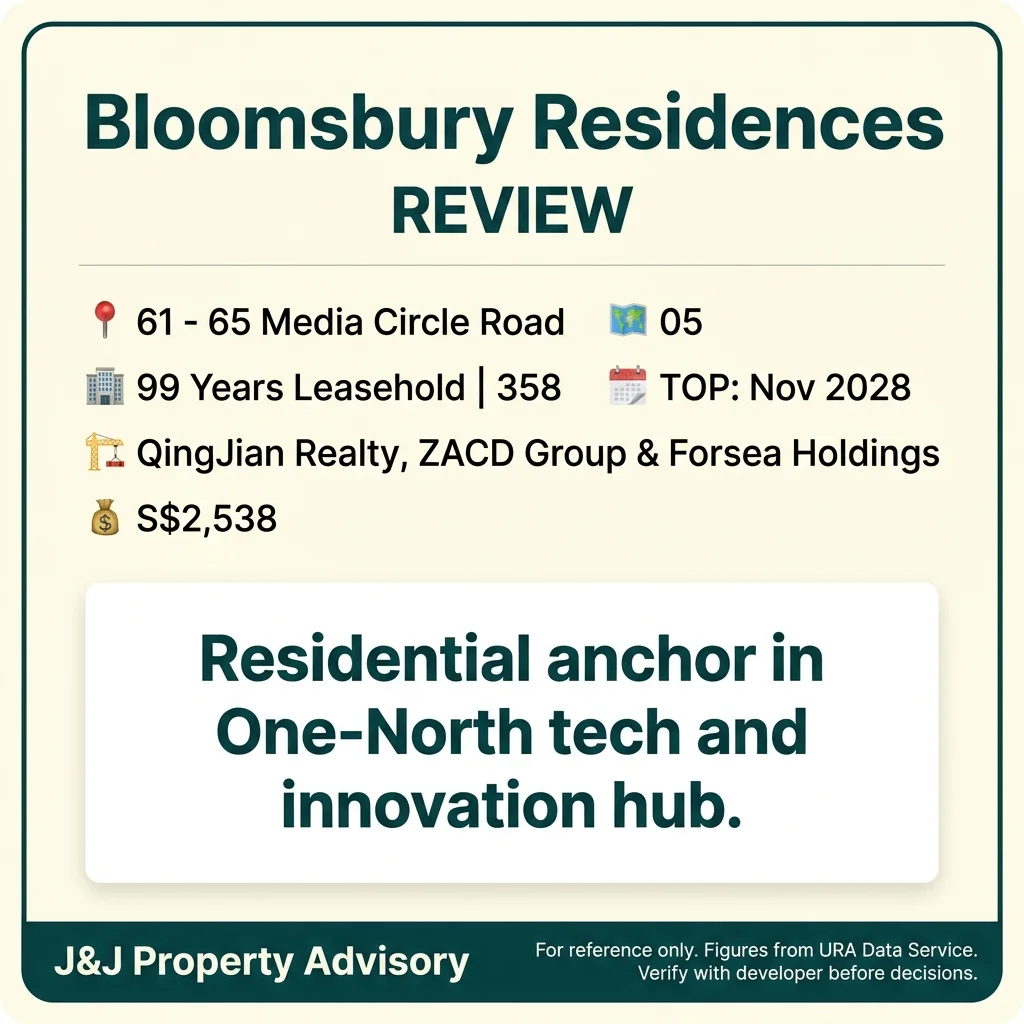

Project Snapshot

| Attribute | Details |

| Site Area | 114,442.9 sqft / 10,632.1 sqm |

| Developer | QingJian Realty, ZACD Group & Forsea Holdings |

| Tenure | 99 Years Leasehold |

| Total Units | 358 |

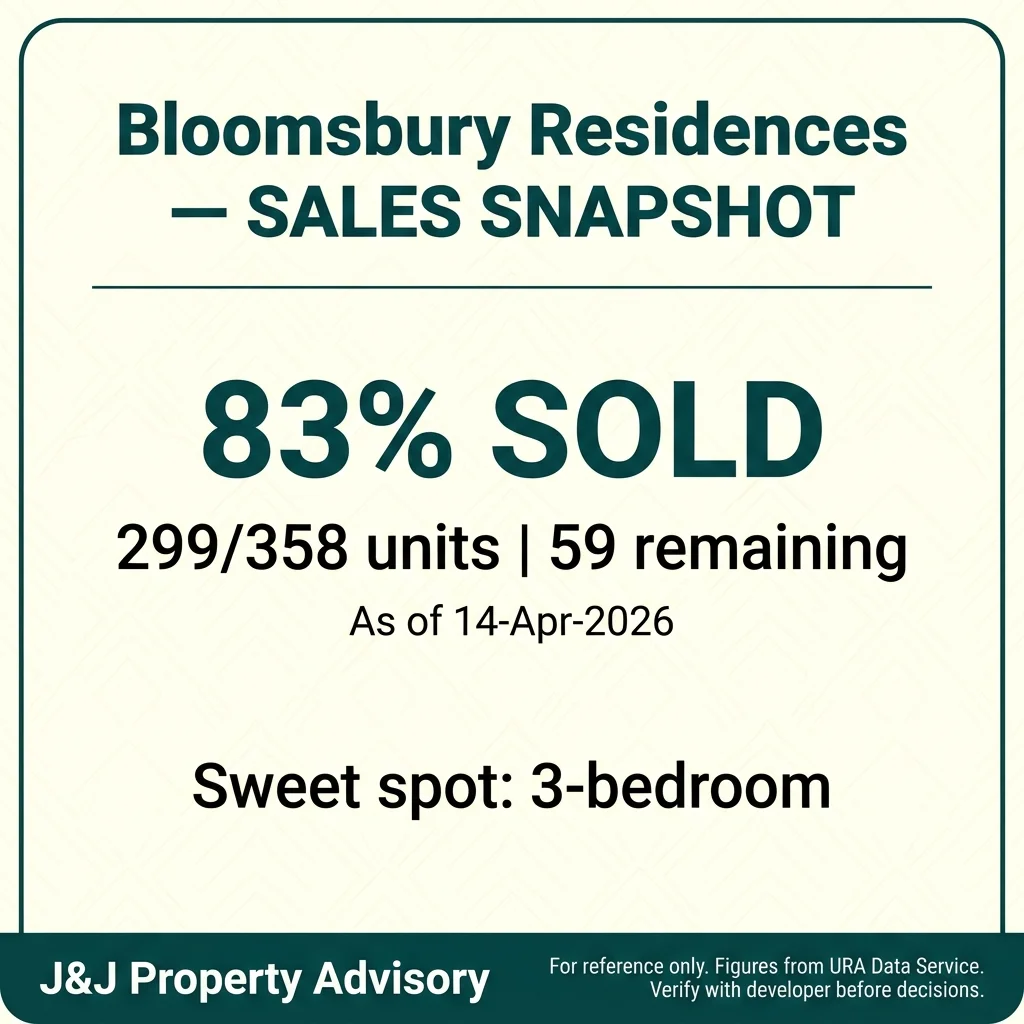

| Units Sold | 299 / 358 (83%) |

| Units Remaining | 59 |

| Expected TOP | Nov 2028 |

| Land Cost PSF PPR | S$1,191 PSF PPR (S$395M total, Jan 2024) |

| Architect | ADDP Architects |

Bloomsbury Residences occupies a rare residential site within the Mediapolis sub-precinct of One-North, a government-designated innovation cluster housing research institutes, media companies, and tech startups. This is the first major condominium launch in a precinct previously dominated by commercial and mixed-use developments. The site’s location along Media Circle Road positions it as a residential anchor for the broader One-North ecosystem, targeting professionals seeking minimal commute friction to Fusionopolis, Biopolis, and nearby industrial parks.

Location & Connectivity

1. MRT Access Requires Commitment

Commonwealth Station (EW20) sits approximately 960m away, One-North Station (CC23) at approximately 1.03km, and Kent Ridge Station (CC24) at approximately 1.19km. None qualify as immediate doorstep convenience. The walk to Commonwealth involves navigating Commonwealth Avenue West, while One-North requires crossing the Ayer Rajah Expressway via pedestrian bridges. Shuttle bus networks serve the One-North precinct, but buyers banking on MRT proximity should calibrate expectations accordingly.

2. One-North Employment Ecosystem

The project sits within the heart of the One-North innovation district, home to over 500 companies including multinational research labs, biomedical firms, and media production houses. Fusionopolis and Biopolis are within a 1.5km radius. For professionals employed within this cluster, commute times can drop to single-digit minutes. This proximity premium is the site’s core value proposition, but it only activates for a specific employment demographic.

3. Expressway Access is Strong

Ayer Rajah Expressway (AYE) entrance points are accessible within 2km, providing direct routes to the CBD, West Coast, and Jurong industrial zones. Commonwealth Avenue West connects northward to the PIE network. This dual-expressway setup supports car-dependent households, though peak-hour congestion on Commonwealth Avenue remains a persistent friction point.

4. Primary School Options Within Walking Range

New Town Primary School sits approximately 790m away, placing it within the 1km Phase 2B priority band for PSLE registration. Fairfield Methodist School (Primary) at approximately 1.3km and Queenstown Primary School at approximately 1.42km fall into the 1-2km Phase 2C zone. Families targeting Fairfield should note its mixed-gender enrolment and historical ballot patterns, which have tightened in recent years.

5. Retail Landscape is Functional, Not Lifestyle-Oriented

Geneo at approximately 1.09km, Queensway Shopping Centre at approximately 1.17km, and Anchorpoint Shopping Centre at approximately 1.3km provide essential services and dining options. Alexandra Central (approximately 1.36km) and Rochester Mall (approximately 1.44km) add to the mix. None of these qualify as destination malls. Households seeking lifestyle retail or entertainment options will travel to Vivocity (4km) or Orchard Road (6km). The project includes an integrated pet-friendly retail zone, though scale and tenant mix remain to be seen.

6. Green Spaces and Nature Access

The broader One-North precinct incorporates linear parks, cycling paths, and green corridors designed to soften the tech-campus aesthetic. Southern Ridges trails and Kent Ridge Park are accessible within 2-3km for weekend activity. The precinct’s walkability is engineered for function rather than leisure, with pedestrian infrastructure connecting office clusters rather than retail or F&B nodes.

Sales Performance

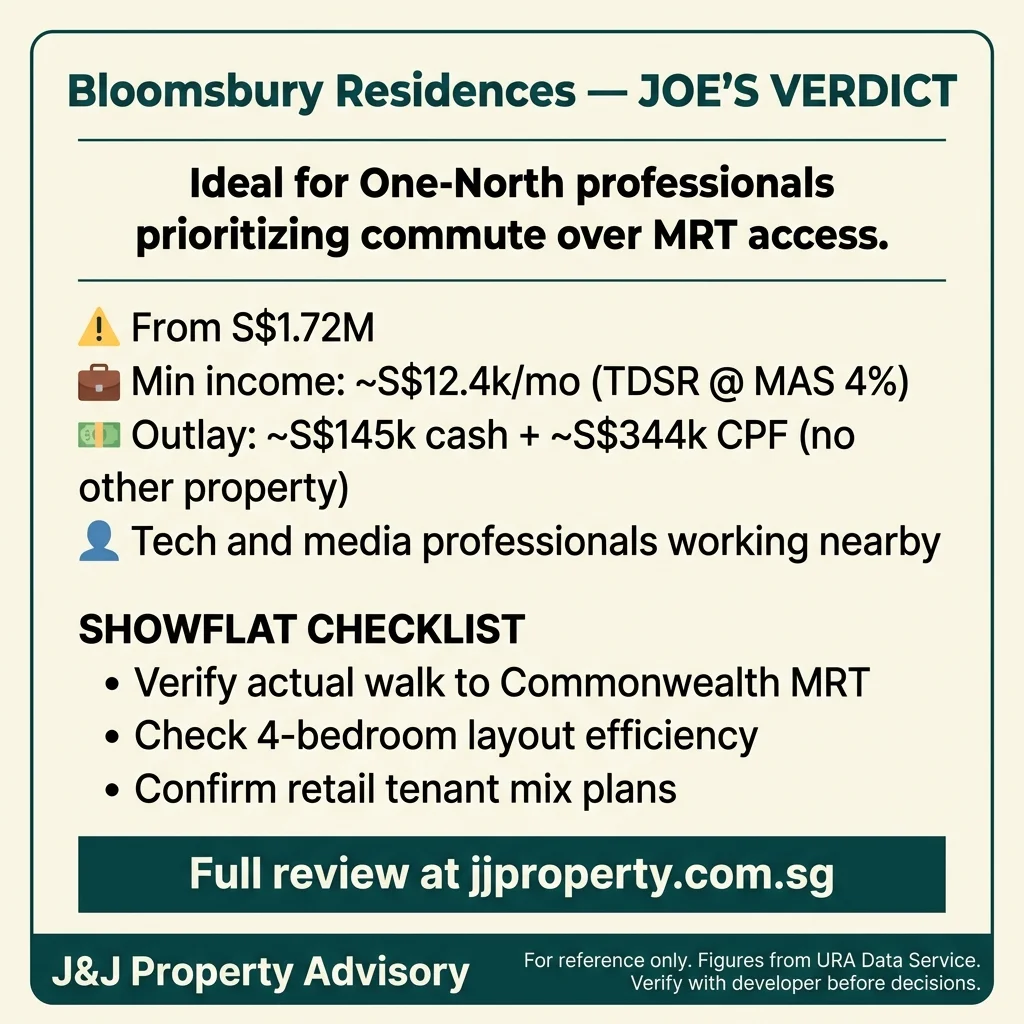

Bloomsbury Residences moved 299 units out of 358 within 12 months of launch, translating to an 83% take-up rate. URA data records 215 units sold through Q4 2025, reflecting an average velocity of 21.5 units per month. The live sales tracker shows 59 remaining units as of April 2026, indicating sustained absorption despite the project’s peripheral MRT positioning.

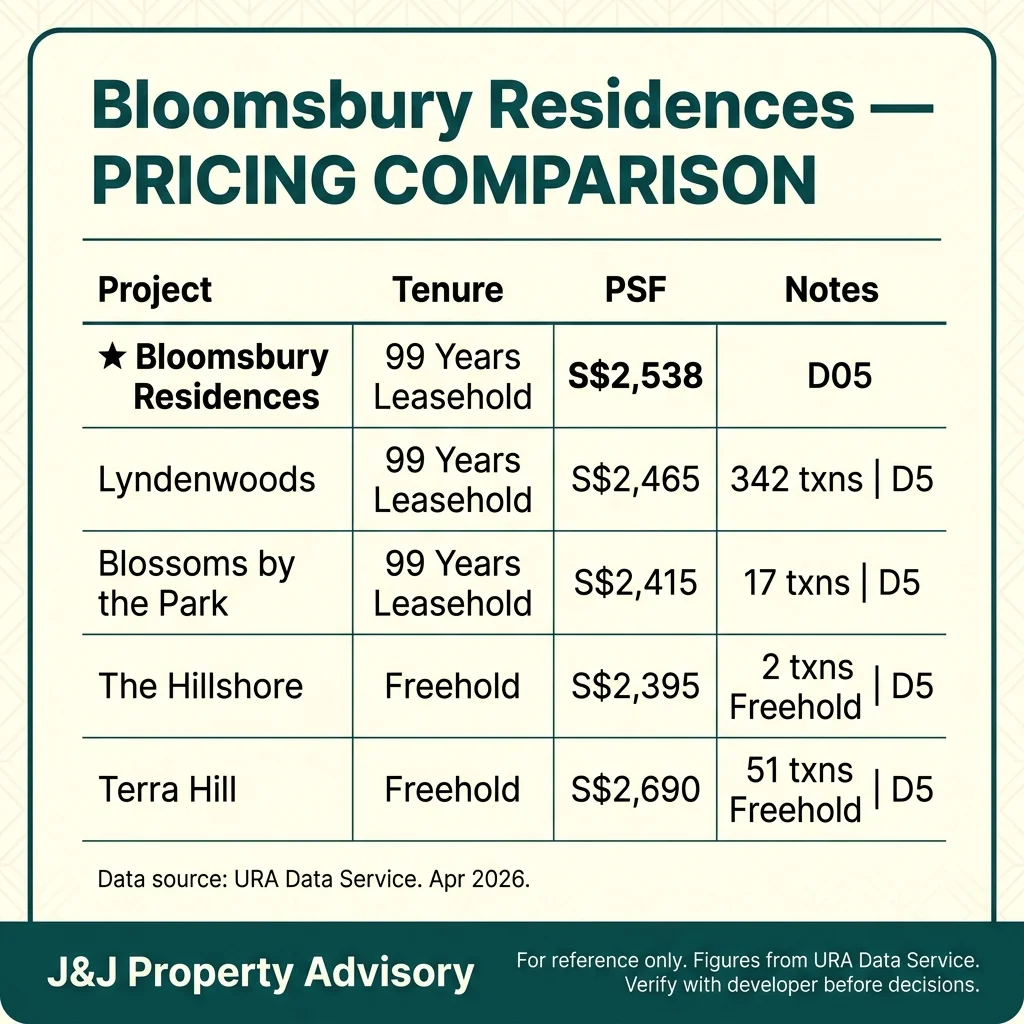

The URA transacted median sits at S$2,538 PSF across 190 caveats lodged over the past 12 months, with a range of S$2,379 to S$2,716 PSF. This positions the project above the District 5 median of S$2,172 PSF (1,947 transactions) but below the S$2,690 median for Terra Hill and in line with Lyndenwoods at S$2,465 PSF. Developer asking prices for remaining units start from S$2,558 PSF for 3-bedroom units, S$2,664 PSF for 2-bedroom units, and S$2,680 PSF for 4-bedroom units. The gap between transacted median and current asking price reflects the typical new launch pricing curve, where earlier units moved at lower entry points.

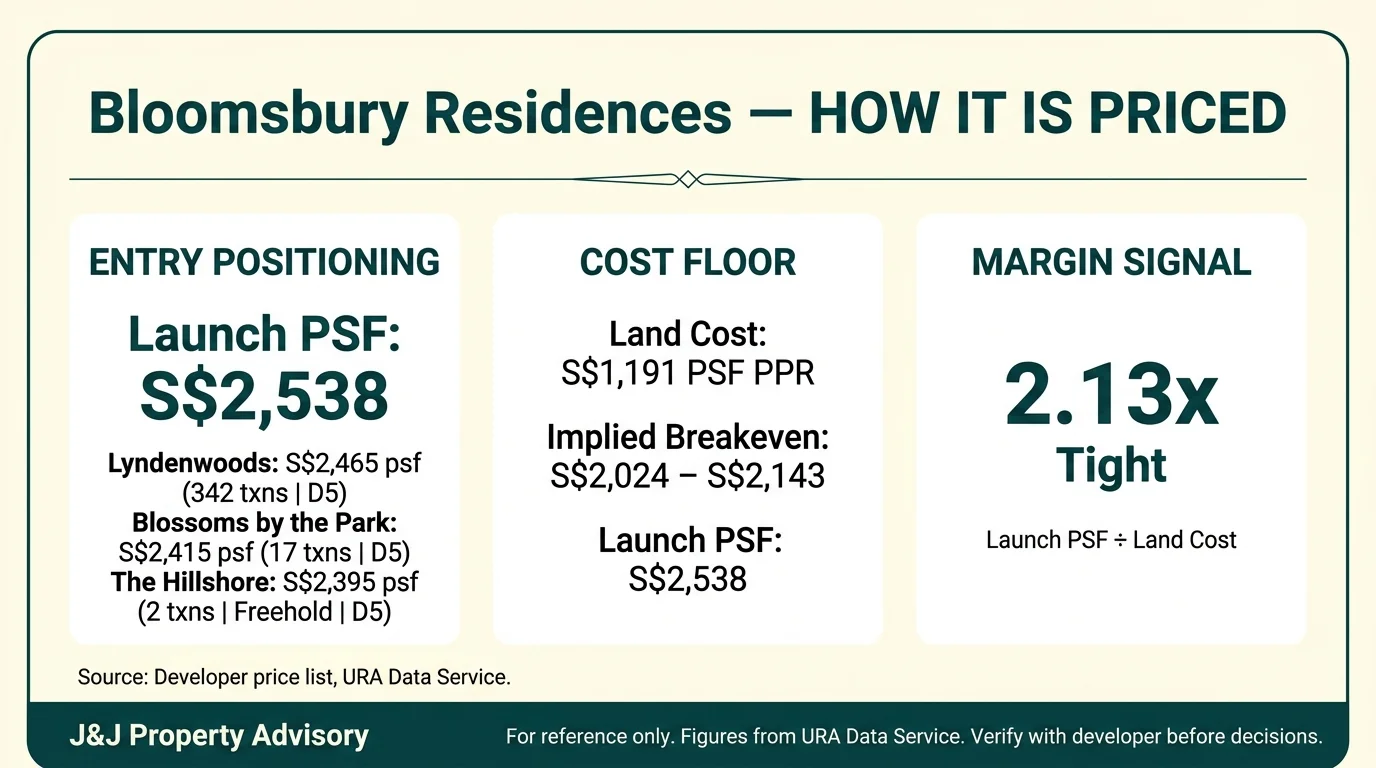

The land cost of S$1,191 PSF PPR (S$395M total, Jan 2024) against a launch PSF from S$2,558 yields a 2.15x multiple, tighter than the market norm of approximately 2.27x. This suggests limited margin for future price escalation unless broader district appreciation compensates.

HDB Upgrader Catchment

| Flat Type | Median Price | Typical Equity | Transactions |

| 3 Room | S$420k | S$200k – S$350k | 1,132 |

| 4 Room | S$930k | S$350k – S$500k | 946 |

| 5 Room | S$1.05M | S$500k – S$700k | 292 |

| Executive | S$1.11M | S$600k – S$900k | 34 |

Clementi and Queenstown form the primary HDB resale catchment for Bloomsbury upgraders. Over the past 24 months these estates recorded 2,450 resale transactions:

Queenstown’s 4-room median (S$969k, 529 txns) sits S$169k above Clementi’s (S$800k, 417 txns), reflecting a more central position. Upgraders typically exit with S$200k–S$350k equity, supporting entry at Bloomsbury’s S$1.72M 2-bedroom tier. 3-bedroom quantums from S$2.31M stretch most single-flat upgrader budgets without additional capital injection.

Unit Mix & Pricing

| Type | Size Range (sqft) | Quantum From | PSF From | Total Units | Remaining |

| 2BR | 568 – 687 | S$1.72M | S$2,664 | 76 (35%) | 11 (14% unsold) |

| 3BR | 900 – 1,095 | S$2.31M | S$2,558 | 73 (34%) | 7 (10% unsold) |

| 4BR | 1,175 – 1,418 | S$3.14M | S$2,680 | 68 (31%) | 35 (51% unsold) |

Note: The 2BR/3BR/4BR breakdown above accounts for 217 residential units from the published factsheet. The project’s total 358 unit count includes additional smaller-format residences (studios/1BR and flexible SOHO layouts) which the developer has not publicly itemised in the factsheet. Percentages reflect share of the 217 published units.

The distribution skews toward 2-bedroom units at 35% of total inventory, reflecting demand from single professionals and dual-income couples without children. The 3-bedroom segment absorbed fastest, with only 10% remaining unsold. The 4-bedroom category shows 51% unsold inventory, a common pattern in projects targeting tech professionals who favour efficiency over space. Quantum entry points at S$1.72M for 2-bedroom units and S$2.31M for 3-bedroom units align with upgrader budgets, though 4-bedroom quantums starting at S$3.14M face tougher competition from freehold alternatives in the district.

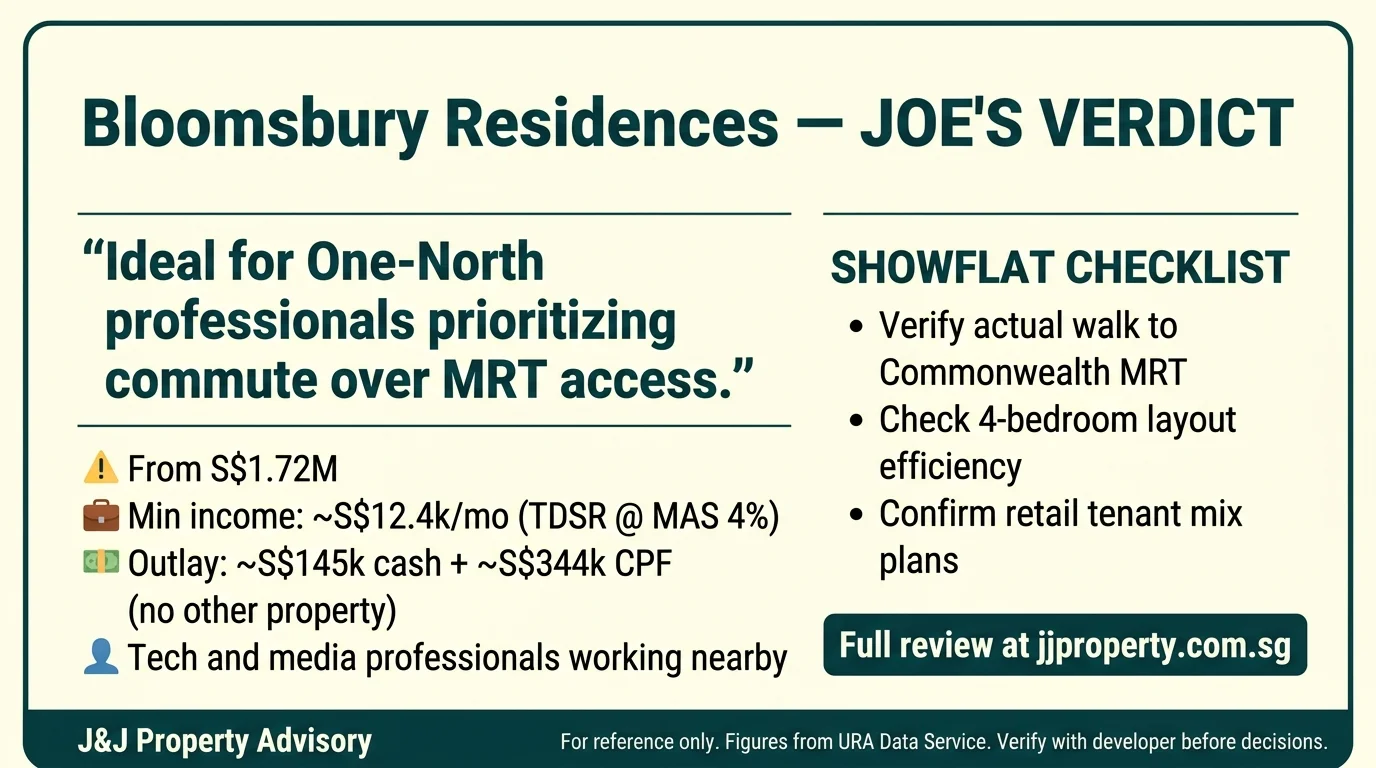

At the S$1.72M 2BR entry, outlay is roughly S$145k cash (5% minimum plus BSD and legals) and S$344k from CPF OA — assuming no other residential property held. ABSD adds 20% (2nd SC purchase) or 30% (3rd and beyond); sell-first or decoupling resets the count to zero.

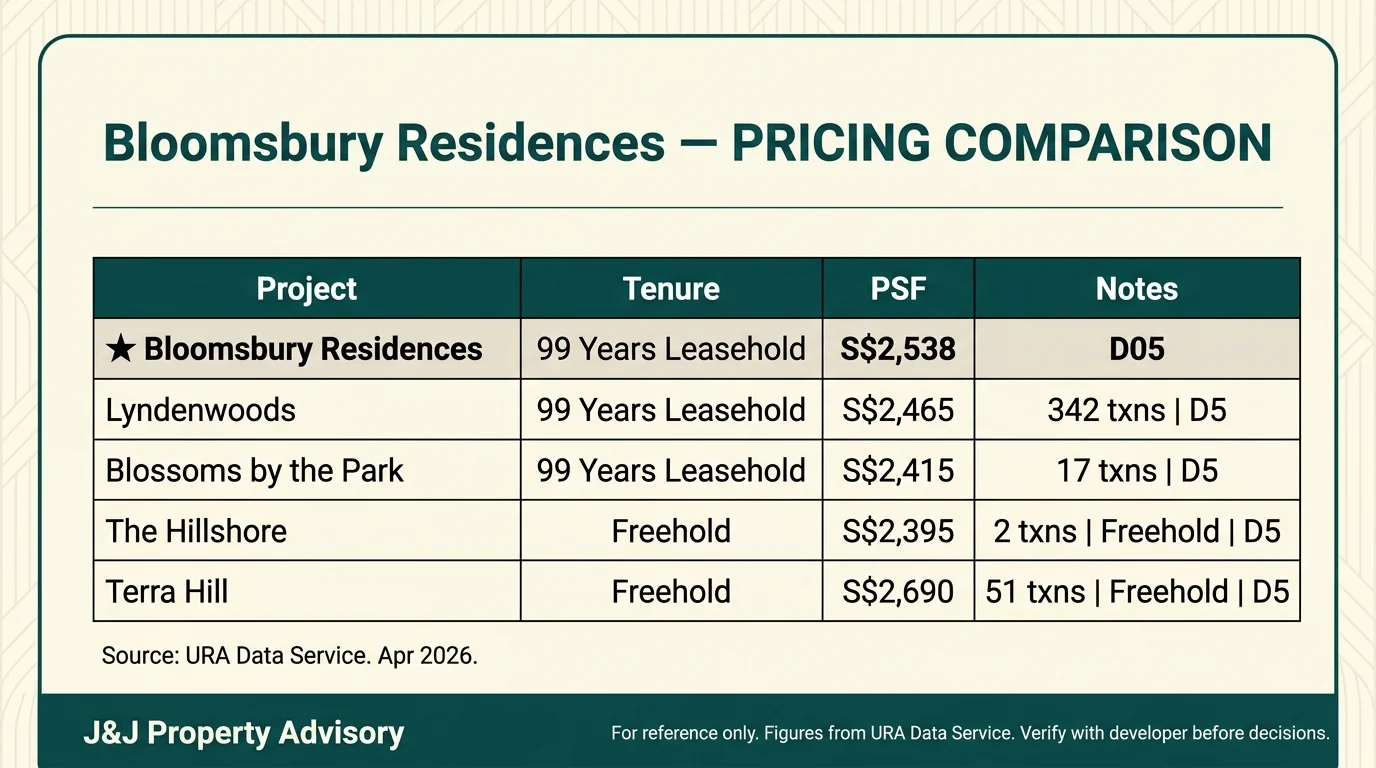

Comparables

| Project | Median PSF | PSF Range | Transactions | Tenure | Expected TOP |

| Bloomsbury Residences | S$2,538 | S$2,379 – S$2,716 | 190 | 99-Year Leasehold | Nov 2028 |

| Lyndenwoods | S$2,465 | S$2,192 – S$2,700 | 342 | 99-Year Leasehold | Jun 2029 |

| Blossoms by the Park | S$2,415 | S$2,248 – S$2,489 | 17 | 99-Year Leasehold | Dec 2027 |

| The Hillshore | S$2,395 | S$2,381 – S$2,409 | 2 | Freehold | Q2 2027 |

| Terra Hill | S$2,690 | S$2,234 – S$2,857 | 51 | Freehold | Q1 2028 |

Bloomsbury’s S$2,538 median places it S$73 above Lyndenwoods and S$123 above Blossoms by the Park, both 99-year leasehold projects with similar 2027-2029 TOP timelines. The S$152 discount to Terra Hill’s S$2,690 median reflects the freehold tenure gap. The Hillshore, despite freehold status, shows a lower S$2,395 median, though only two transactions limit comparability. Bloomsbury’s pricing occupies the middle band of District 5 leasehold offerings, trading at a premium to location equivalents without proximity to major MRT interchanges but capturing the One-North employment ecosystem value.

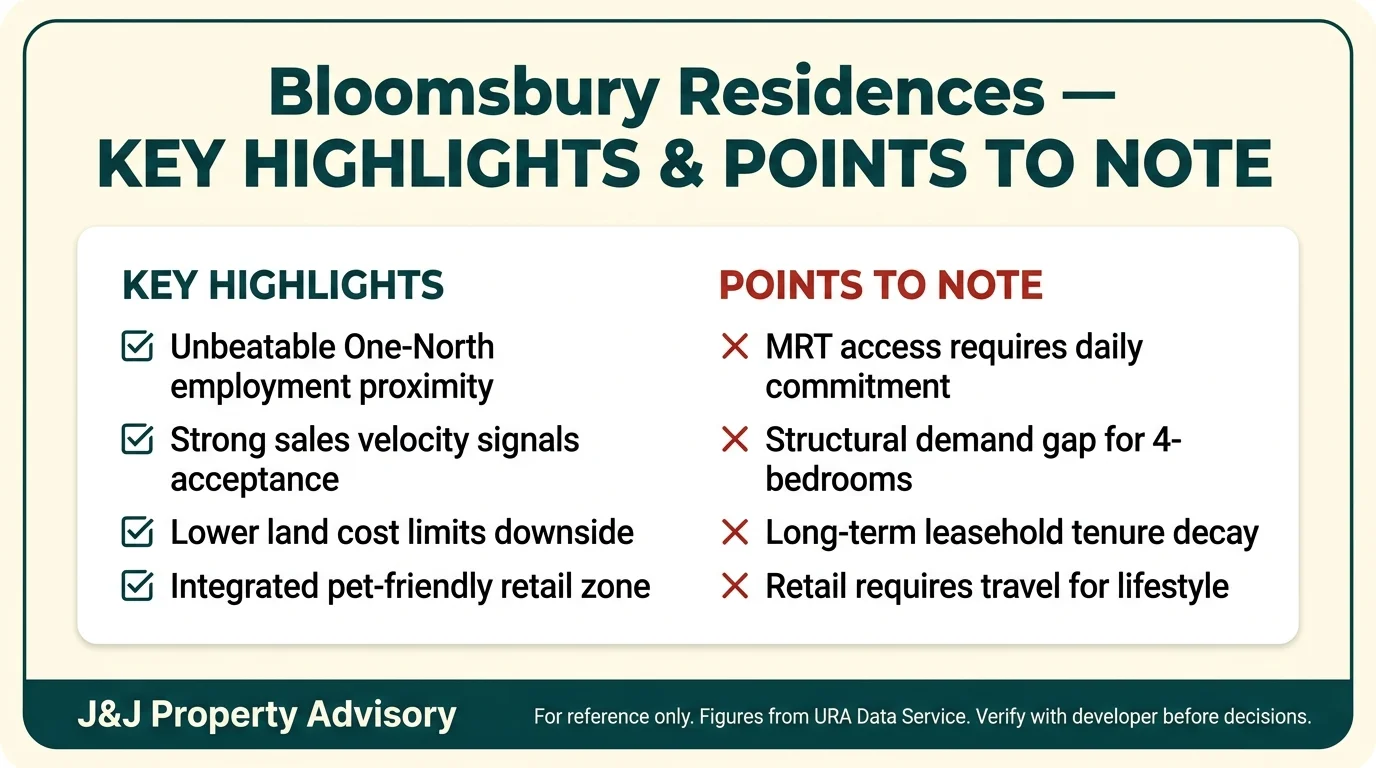

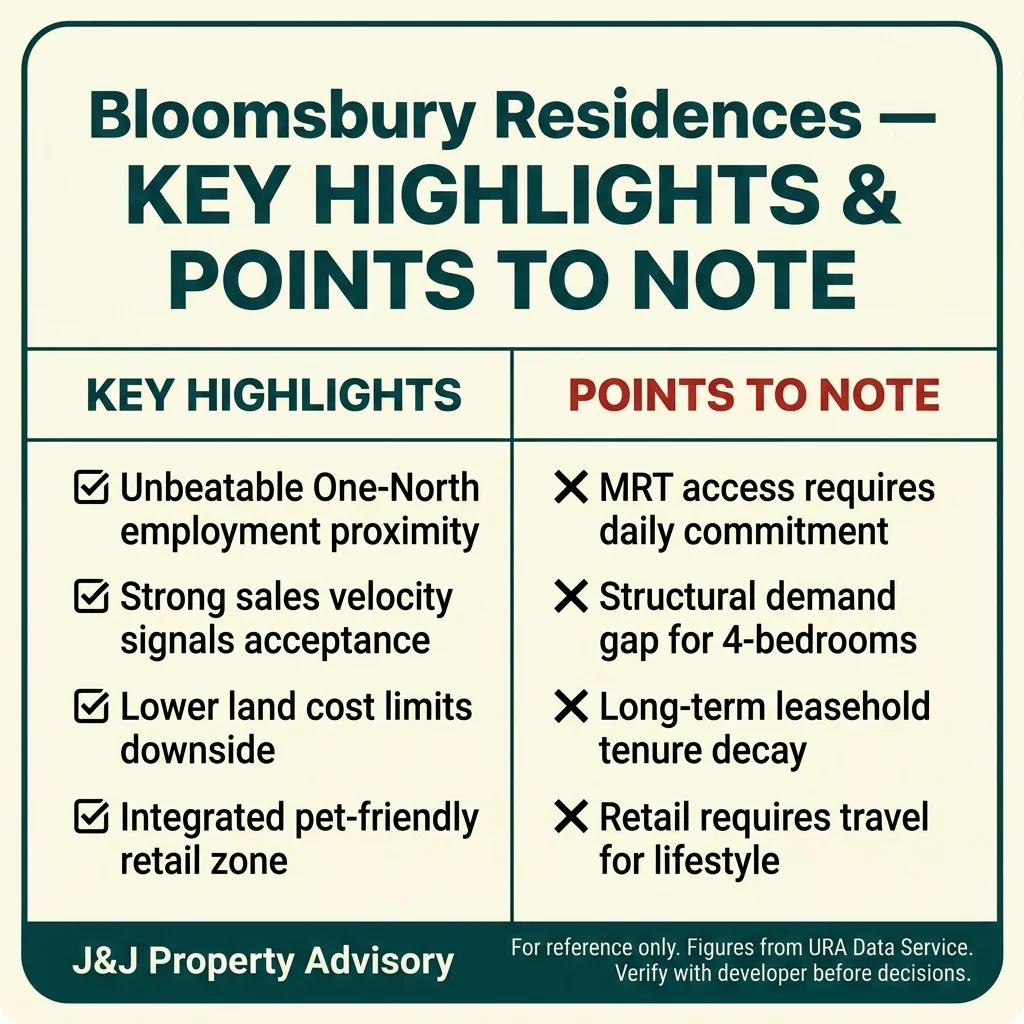

Key Strengths

One-North Employment Proximity is Material

For tech, biomedical, and media professionals employed within Fusionopolis, Biopolis, or Mediapolis, commute times compress to under 10 minutes. This proximity premium reduces transport friction and supports work-life integration, particularly for households with dual incomes in the same employment cluster. The value proposition collapses if neither household member works within One-North, making this a highly specific advantage.

Strong Sales Velocity Signals Market Acceptance

Moving 83% of inventory within 12 months, with an average velocity of 21.5 units per month, reflects sustained buyer confidence despite the project’s MRT positioning. The 3-bedroom segment cleared 90% of stock, indicating demand from upgraders and small families who prioritise unit efficiency and quantum affordability over traditional lifestyle features. This absorption pattern de-risks resale liquidity concerns for early buyers.

Land Cost Multiple Limits Downside Risk

The 2.15x land cost multiple sits below the market norm of 2.27x, suggesting tighter developer margins and reduced risk of post-launch price compression. While this limits upside speculation, it provides a buffer against broader market corrections. Buyers entering at current asking prices (S$2,558 to S$2,680 PSF) are closer to developer cost base than typical new launches.

Integrated Retail Component Adds Convenience Layer

The pet-friendly retail zone integrated as a public thoroughfare introduces ground-floor activation that reduces reliance on external amenities for daily essentials. While scale and tenant mix remain unconfirmed, the concept addresses the precinct’s historical retail gap. Households with pets gain additional utility, though this feature alone does not compensate for the broader retail sparsity in the area.

School Proximity for New Town Primary

New Town Primary School at approximately 790m falls within the 1km Phase 2B priority band, offering a clear path to balloting advantage for families with primary-age children. This proximity carries weight for upgraders timing entry around MOE registration cycles, though the school’s enrolment patterns and popularity relative to other District 5 options require separate verification.

Points to Watch

MRT Distance is a Daily Friction Point

At 960m to Commonwealth Station and 1.03km to One-North Station, residents face a 12-15 minute walk under optimal conditions. Rain, heat, and stroller logistics extend this further. The precinct shuttle bus network provides partial mitigation, but schedule dependency introduces variability. Households reliant on daily MRT commutes to CBD or East Coast will experience this as a persistent inconvenience rather than a minor trade-off.

4-Bedroom Inventory Overhang Signals Demand Mismatch

With 51% of 4-bedroom units unsold versus 14% for 2-bedroom and 10% for 3-bedroom units, the data reveals a structural demand gap. Families seeking larger units within this quantum range (from S$3.14M) can access freehold alternatives in adjacent districts or larger landed options in Districts 21 and 23. This inventory pattern may compress 4-bedroom resale pricing relative to smaller unit types.

99-Year Leasehold Tenure Introduces Long-Term Decay

At TOP in 2028, the lease will stand at approximately 95 years remaining. While this poses minimal impact over the first 10-15 years, the decay curve accelerates beyond the 60-year mark, compressing resale valuations and mortgage eligibility. Buyers planning 20-30 year hold periods should model the tenure gap against freehold comparables, particularly given the S$152 PSF discount to Terra Hill’s freehold premium.

Retail and Lifestyle Amenities Require External Travel

The project’s immediate retail catchment consists of functional shopping centres (Queensway, Anchorpoint) serving basic needs rather than lifestyle or entertainment demand. Families seeking weekend dining, cinema, or retail therapy will drive 15-20 minutes to Vivocity or Orchard Road. This geographic isolation suits professionals with minimal leisure time but frustrates households with children seeking varied social infrastructure.

Rental Yield Faces New Launch Compression

District 5 gross yields typically range 3.0-4.0%, but new launch pricing premiums reduce initial yields to an estimated 2.6-3.4% range. At S$2,558 PSF entry points, a 900 sqft 3-bedroom unit (S$2.3M) would require monthly rents of approximately S$5,000 to hit 3.0% gross yield. Current One-North rental benchmarks for comparable units sit closer to S$4,500-S$4,800, compressing achievable yields further. Investors should model rental escalation timelines before committing.

Tight Developer Margin Limits Future Price Appreciation

The 2.15x land cost multiple, while reducing downside risk, also caps speculative upside. Developer margins leave little room for aggressive price increases on remaining units, and resale buyers will inherit this compressed margin structure. Capital appreciation will depend heavily on broader district movements rather than project-specific scarcity dynamics. This favours own-stay buyers over short-term flippers.

Bottom Line

Bloomsbury Residences delivers a clear value proposition for a narrow buyer segment: tech and media professionals employed within the One-North ecosystem who prioritise commute efficiency over traditional condominium lifestyle features. The 83% take-up rate within 12 months validates market acceptance, and the S$2,538 transacted median positions the project within District 5 leasehold norms without excessive premium. The MRT distance at 960m to Commonwealth Station is a tangible daily friction that cannot be engineered away, and the 51% unsold inventory in the 4-bedroom segment signals a structural demand mismatch for larger family units.

The tight land cost multiple of 2.15x reduces downside risk but also limits capital appreciation potential. Buyers entering at current asking prices (S$2,558 to S$2,680 PSF) are paying close to developer cost base, which provides a buffer against broader market corrections but offers minimal speculative upside. The 99-year leasehold tenure introduces long-term decay considerations, though these remain immaterial for hold periods under 15 years. The retail and lifestyle infrastructure gap requires external travel, making this better suited to time-starved professionals than families seeking varied social amenities.

For Own-Stay Buyers

If you work within Fusionopolis, Biopolis, or Mediapolis and value commute compression above MRT convenience, the project delivers tangible daily utility. The 3-bedroom segment at S$2.31M entry points offers the strongest value-to-function ratio, with 90% absorption validating market acceptance. Families targeting New Town Primary (790m, Phase 2B range) gain balloting advantage, though larger 4-bedroom units face stiff competition from freehold alternatives at similar quantums. Run the numbers on your actual daily commute pattern before committing—if neither household member works in One-North, the location premium evaporates.

For Investment Buyers

Rental demand from One-North expatriate professionals provides a stable tenant base, but yields compress to an estimated 2.6-3.4% range due to new launch pricing premiums. The 2-bedroom segment (35% of inventory, 14% unsold) offers the most liquid resale profile, targeting the same professional demographic that drove initial absorption. The 4-bedroom overhang (51% unsold) introduces resale pricing risk for larger units. Tight developer margins limit capital appreciation upside, making this a yield-focused play rather than a speculative flip. Model rental escalation timelines carefully—current One-North benchmarks sit S$200-S$500 below the monthly rents required to achieve 3.0% gross yields at entry pricing.

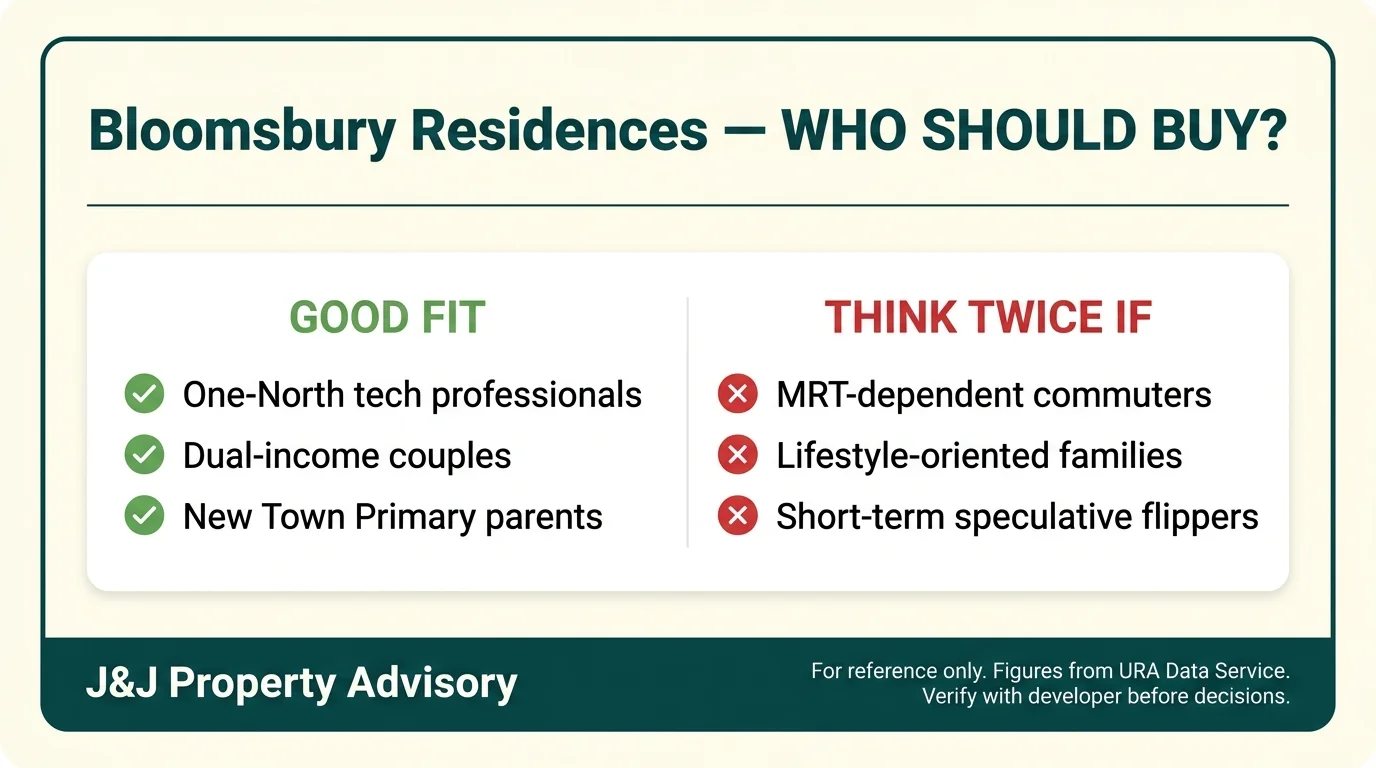

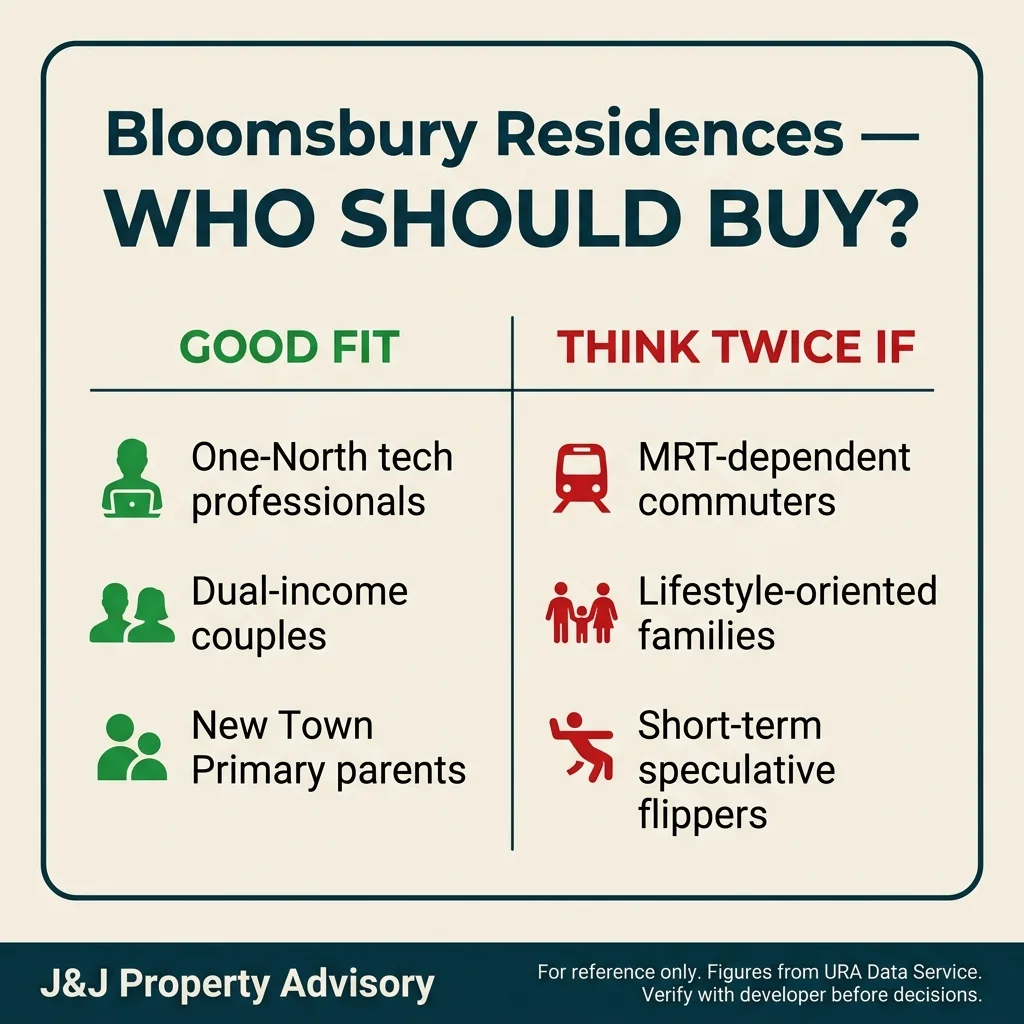

Who Is This For

Good fit:

- Tech, biomedical, or media professionals employed within Fusionopolis, Biopolis, or Mediapolis seeking sub-10 minute commutes

- Dual-income couples without children prioritising unit efficiency and quantum affordability (2-bedroom units from S$1.72M)

- Upgraders targeting New Town Primary School within the 1km Phase 2B priority band (approximately 790m)

- Car-dependent households valuing expressway access (AYE within 2km) over MRT proximity

- Investors targeting stable rental demand from One-North expatriate professionals, accepting 2.6-3.4% gross yields

- Own-stay buyers comfortable with functional retail infrastructure and willing to travel 15-20 minutes for lifestyle amenities

Not ideal for:

- Households reliant on daily MRT commutes to CBD or East Coast (960m to Commonwealth, 1.03km to One-North)

- Families seeking destination retail, entertainment, or varied social infrastructure within immediate walking radius

- Investors chasing high capital appreciation potential—tight 2.15x land cost multiple limits speculative upside

- Buyers prioritising freehold tenure or long-term hold periods beyond 20-30 years (99-year leasehold decay accelerates post-60 years)

- Families requiring 4-bedroom units—51% unsold inventory signals structural demand mismatch and resale pricing compression risk

- Professionals employed outside the One-North cluster—location premium collapses without employment proximity benefit

Review Date: April 2026

Agent: Joe Chow | CEA Reg No.: R072635C

Agency: SRI Pte Ltd | Licence: L3010738A

Contact: +65 8098 0916

This review is based on publicly available data and official URA transaction records. It is not financial advice. Verify all details with the developer before making purchase decisions.